- United States

- /

- Hospitality

- /

- NYSE:CHH

Investors in Choice Hotels International (NYSE:CHH) have seen notable returns of 50% over the past five years

When you buy and hold a stock for the long term, you definitely want it to provide a positive return. But more than that, you probably want to see it rise more than the market average. But Choice Hotels International, Inc. (NYSE:CHH) has fallen short of that second goal, with a share price rise of 45% over five years, which is below the market return. On a brighter note, more newer shareholders are probably rather content with the 25% share price gain over twelve months.

Now it's worth having a look at the company's fundamentals too, because that will help us determine if the long term shareholder return has matched the performance of the underlying business.

See our latest analysis for Choice Hotels International

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

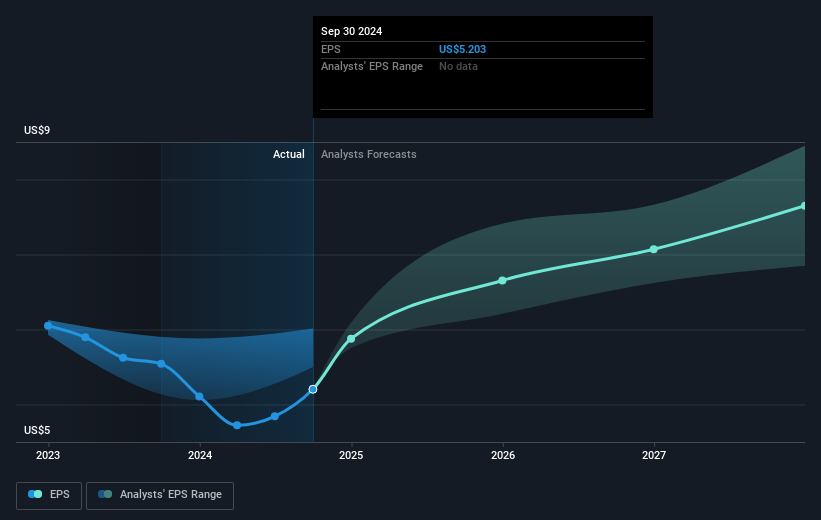

During five years of share price growth, Choice Hotels International achieved compound earnings per share (EPS) growth of 7.3% per year. This EPS growth is remarkably close to the 8% average annual increase in the share price. This indicates that investor sentiment towards the company has not changed a great deal. In fact, the share price seems to largely reflect the EPS growth.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

Before buying or selling a stock, we always recommend a close examination of historic growth trends, available here.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. We note that for Choice Hotels International the TSR over the last 5 years was 50%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

A Different Perspective

Choice Hotels International's TSR for the year was broadly in line with the market average, at 26%. That gain looks pretty satisfying, and it is even better than the five-year TSR of 8% per year. Even if the share price growth slows down from here, there's a good chance that this is business worth watching in the long term. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Choice Hotels International (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

Of course Choice Hotels International may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CHH

Choice Hotels International

Operates as a hotel franchisor in the United States and internationally.

Moderate growth potential second-rate dividend payer.

Similar Companies

Market Insights

Community Narratives