- United States

- /

- Hospitality

- /

- NYSE:CAVA

Is CAVA Group’s (CAVA) Lofty Valuation Outrunning Its Strong Store Economics And Expansion Story?

Reviewed by Sasha Jovanovic

- In recent weeks, analysts have highlighted CAVA Group’s strong growth potential, solid store-level economics, and successful expansion into new regions, reinforcing confidence in its fundamentals despite cost and competitive pressures.

- At the same time, some valuation analyses now suggest CAVA’s shares may be priced well above their estimated intrinsic value, putting a spotlight on the gap between enthusiasm for the brand and more cautious cash flow assumptions.

- With analysts praising CAVA’s new market expansion and store economics, we’ll now explore how this shapes the company’s broader investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

CAVA Group Investment Narrative Recap

To own CAVA Group today, you need to believe its fast casual Mediterranean concept can keep attracting new guests and supporting profitable unit growth, even as competition and input costs rise. The recent analyst enthusiasm around store economics and new market openings supports that thesis, but the highlighted valuation concerns and 1 year share price decline make sentiment, rather than operations, the key short term catalyst. The biggest risk that stands out right now is aggressive expansion potentially outpacing sustainable demand.

Against this backdrop, CAVA’s updated 2025 guidance and Q3 results are especially relevant. Management still expects 68 to 70 net new restaurant openings this year and solid restaurant level margins, even after trimming same store sales growth expectations to 3.0% to 4.0%. That combination of continued unit expansion and slightly softer comparable sales underlines how much of the current story rests on CAVA successfully scaling its footprint without diluting returns over time.

Yet investors should also be aware that rapid restaurant expansion could start to strain unit economics and market saturation risks...

Read the full narrative on CAVA Group (it's free!)

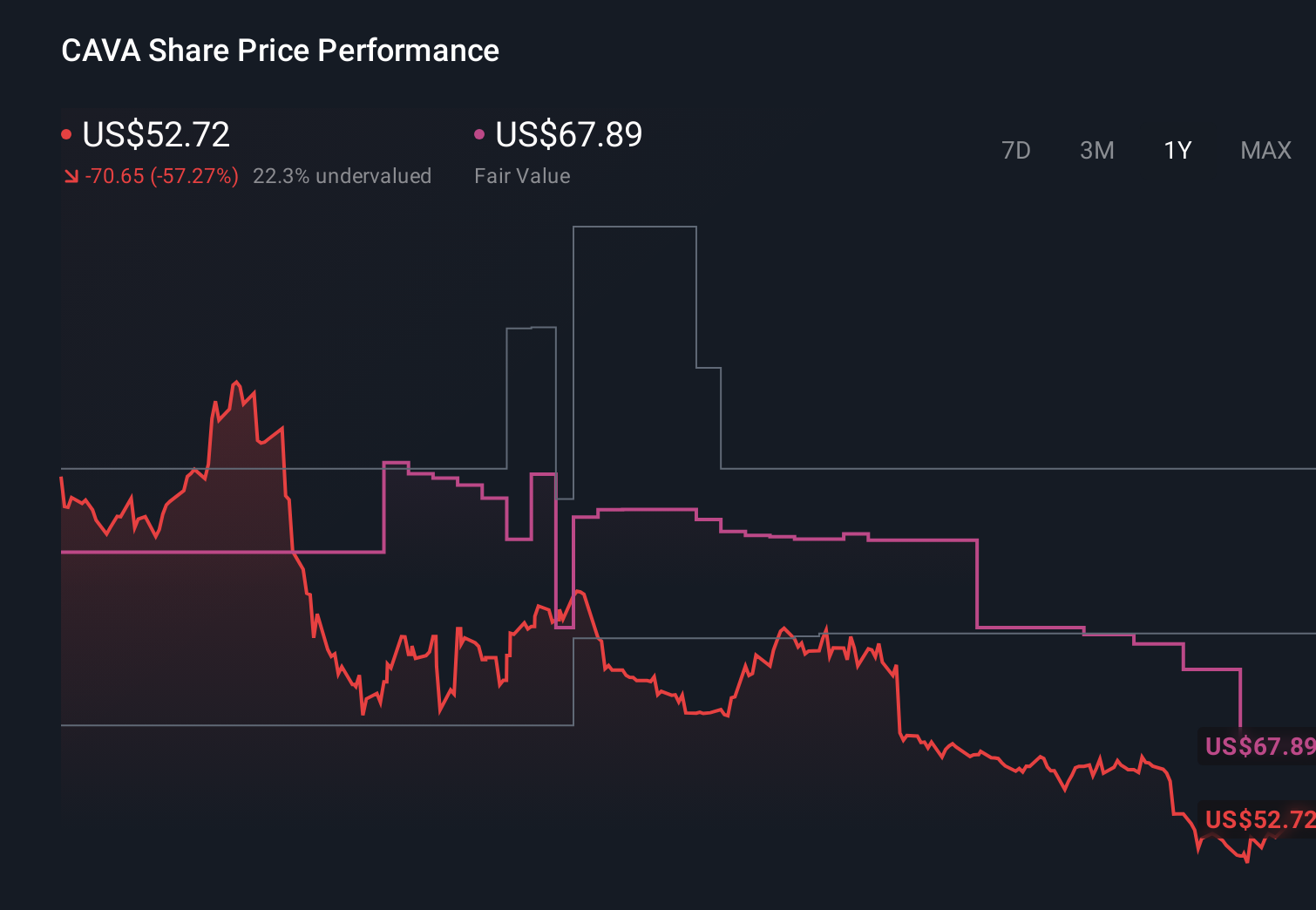

CAVA Group's narrative projects $1.9 billion revenue and $126.2 million earnings by 2028. This requires 20.4% yearly revenue growth and a $14.5 million earnings decrease from $140.7 million today.

Uncover how CAVA Group's forecasts yield a $67.89 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Eleven fair value estimates from the Simply Wall St Community span roughly US$37.88 to US$110 per share, showing just how far apart individual expectations can be. When you set that against concerns about CAVA’s rapid expansion and the potential for market saturation, it underlines why many readers may want to compare several viewpoints before deciding how this growth story fits into their portfolio.

Explore 11 other fair value estimates on CAVA Group - why the stock might be worth 33% less than the current price!

Build Your Own CAVA Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CAVA

CAVA Group

Owns and operates a chain of restaurants under the CAVA brand in the United States.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion