Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:TXRH

Will Reduced Brazilian Beef Tariffs Reshape Texas Roadhouse's (TXRH) Margin Story?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, Jim Cramer highlighted the past reduction of tariffs on Brazilian beef, emphasizing the potential positive impact on Texas Roadhouse's cost structure and profitability.

- An interesting aspect is Texas Roadhouse's decision to maintain strong sales by not raising menu prices, leaving its margins highly sensitive to shifts in commodity costs like beef.

- We'll explore how expected margin improvements from lower beef import tariffs could influence Texas Roadhouse's investment narrative going forward.

Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

Texas Roadhouse Investment Narrative Recap

To be a shareholder in Texas Roadhouse, one must believe in the company's ability to consistently grow guest traffic, expand its brand footprint, and protect margins despite volatile input costs. The recent reduction of Brazilian beef tariffs has the potential to ease food cost pressures, addressing a key short term catalyst tied to margin recovery. At the same time, elevated labor inflation and heavy reliance on in-person dining remain the most important risks that could still offset any cost savings if broader inflation persists.

The latest quarterly earnings announcement, released in early November, is especially relevant in assessing the impact of lower beef costs. While Q3 revenue climbed year-on-year to US$1,436.34 million, net income held steady, reflecting that input inflation had still been weighing on profitability. Future quarters could see margin benefits if the cost reprieve from tariffs proves material, complementing the company’s ongoing efforts to drive growth with disciplined expense management.

However, despite the encouraging outlook on beef costs, investors should pay close attention in case wage pressures intensify...

Read the full narrative on Texas Roadhouse (it's free!)

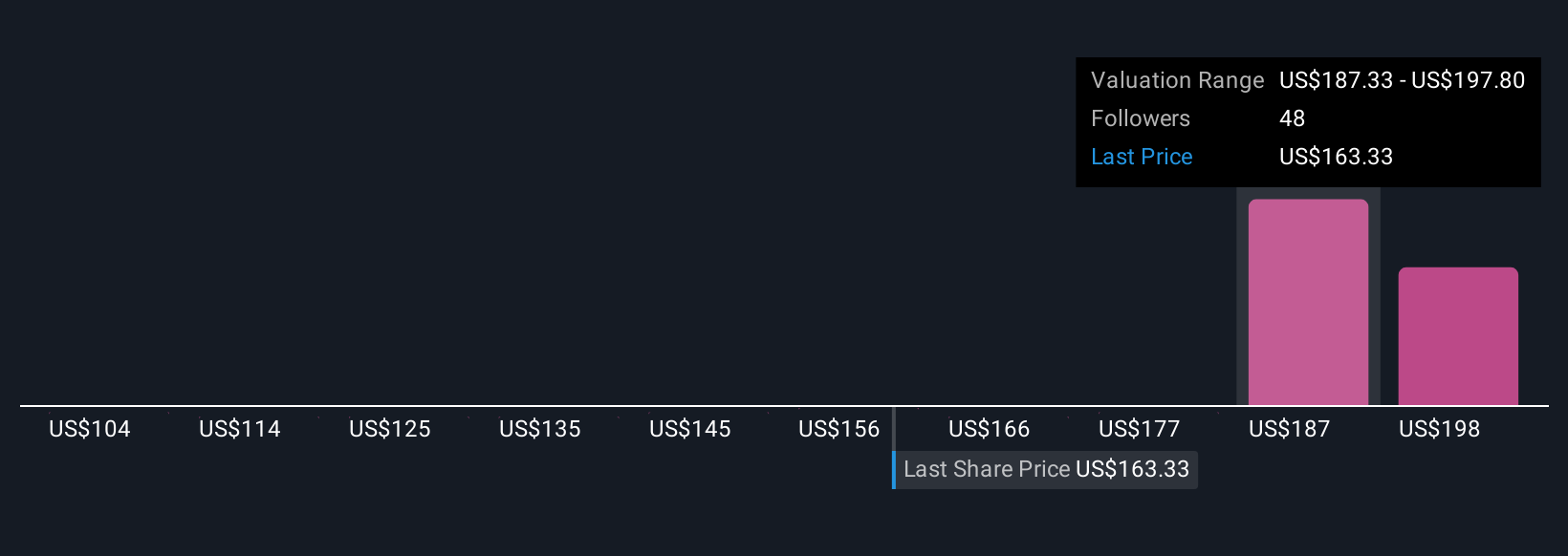

Texas Roadhouse's narrative projects $7.4 billion in revenue and $594.2 million in earnings by 2028. This requires 9.1% yearly revenue growth and a $156 million earnings increase from $438.0 million currently.

Uncover how Texas Roadhouse's forecasts yield a $189.08 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offered six fair value estimates for Texas Roadhouse ranging from US$149.17 to US$227.56 per share. While community views are spread, the recent beef tariff cut ties directly to gross margin sensitivity which could influence future profitability in either direction.

Explore 6 other fair value estimates on Texas Roadhouse - why the stock might be worth as much as 30% more than the current price!

Build Your Own Texas Roadhouse Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Texas Roadhouse research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Texas Roadhouse research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Texas Roadhouse's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 35 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Texas Roadhouse might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TXRH

Texas Roadhouse

Operates casual dining restaurants in the United States and internationally.

Adequate balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative