Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:MCRI

Monarch Casino & Resort (MCRI): Checking Valuation After Strong Year-to-Date Gains and Recent Momentum Cooldown

Simply Wall St

Reviewed by Simply Wall St

Monarch Casino & Resort (MCRI) has quietly outperformed many peers this year, with the stock up about 23% year to date and roughly 12% over the past year, despite recent pullbacks.

See our latest analysis for Monarch Casino & Resort.

That recent dip in the 90 day share price return contrasts with a strong year to date share price gain and a solid one year total shareholder return. This suggests momentum has cooled slightly rather than reversed.

If Monarch’s steady performance has you thinking about where else consistent compounding might be hiding, now is a good time to explore fast growing stocks with high insider ownership.

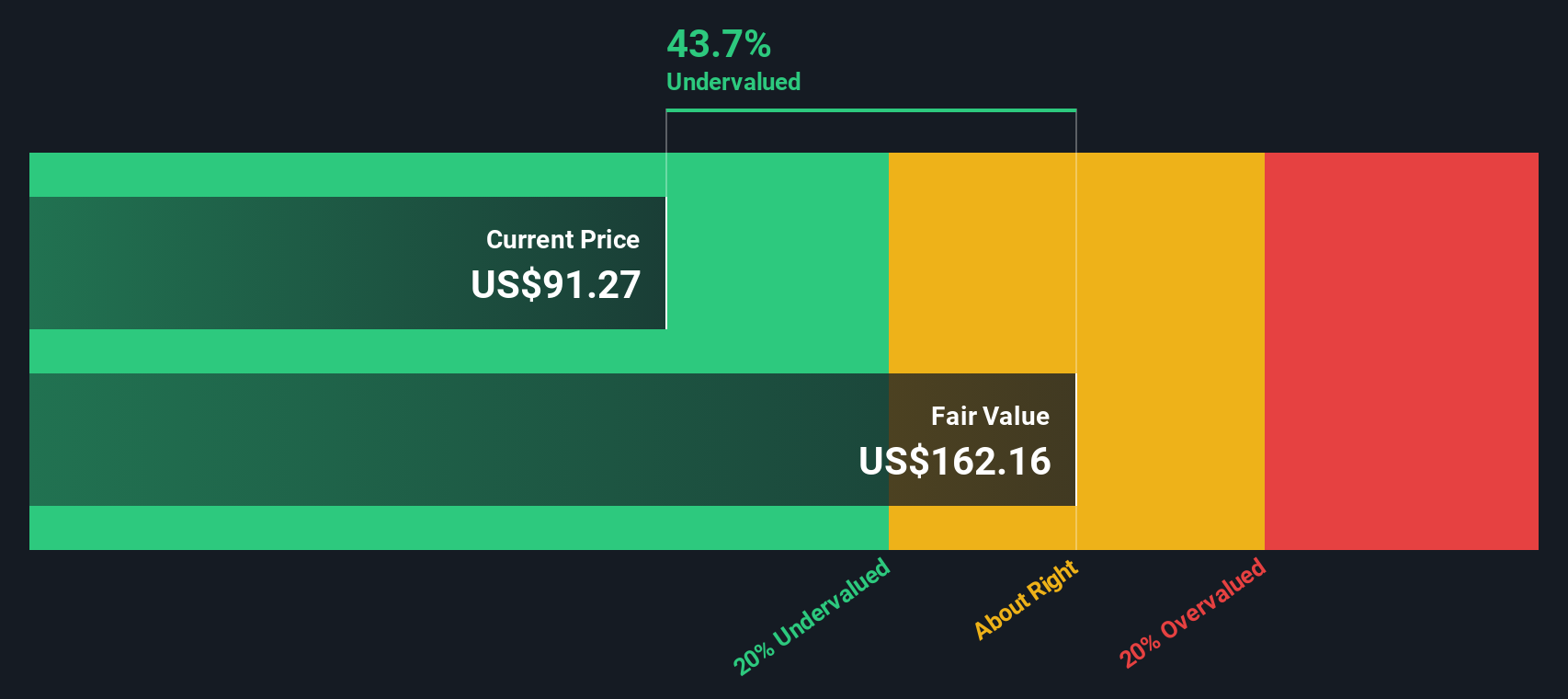

With shares still trading at a notable discount to analyst targets despite steady revenue and profit growth, the key question now is whether Monarch Casino & Resort remains undervalued or if the market is already pricing in its future expansion?

Price to Earnings of 21.2x: Is it justified?

On a price to earnings basis, Monarch Casino & Resort trades at 21.2 times earnings, with the latest close at $96 and the stock screens as good value versus several benchmarks.

The price to earnings ratio compares what investors pay for each dollar of the company’s current earnings, a key lens for mature, profitable hospitality operators like Monarch.

Here, the market is paying 21.2x earnings, a touch below the peer average of 25.6x and fractionally under the broader US hospitality industry average of 21.3x. This suggests investors are not assigning a speculative premium given the reported five year earnings growth of 14% per year and forecasts for profits to continue growing around the high single digits.

Set against Simply Wall St’s estimated fair price to earnings ratio of 16.2x, however, the current 21.2x looks demanding. This implies the market could eventually gravitate toward a lower multiple if growth underwhelms or sector sentiment cools.

Explore the SWS fair ratio for Monarch Casino & Resort

Result: Price-to-Earnings of 21.2x (ABOUT RIGHT)

However, persistent multiple compression, if earnings growth slows or regional gaming demand softens, could quickly erode today’s apparent valuation support.

Find out about the key risks to this Monarch Casino & Resort narrative.

Another View, Using Our DCF Model

While the current price to earnings ratio looks roughly in line with peers, our DCF model presents a different perspective. It suggests Monarch Casino & Resort is trading at about a 40.8% discount to its estimated fair value of around $162 per share, which indicates the market may be underestimating its long term cash generation potential.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Monarch Casino & Resort for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 909 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Monarch Casino & Resort Narrative

And if you would rather follow your own process than rely on this view, you can quickly build a personalised thesis in just a few minutes: Do it your way.

A great starting point for your Monarch Casino & Resort research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction ideas?

Before you move on, put your research edge to work by hunting for the next standout opportunity with Simply Wall St’s powerful, data driven stock screeners.

- Capture potential multi baggers early by targeting quality growth at compelling prices through these 909 undervalued stocks based on cash flows.

- Capitalize on the AI wave by focusing on businesses harnessing intelligent automation and data advantage using these 26 AI penny stocks.

- Secure growing income streams by narrowing in on resilient companies offering attractive yields via these 14 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MCRI

Monarch Casino & Resort

Through its subsidiaries, owns and operates hotels and casinos.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

14 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative