Advertisement

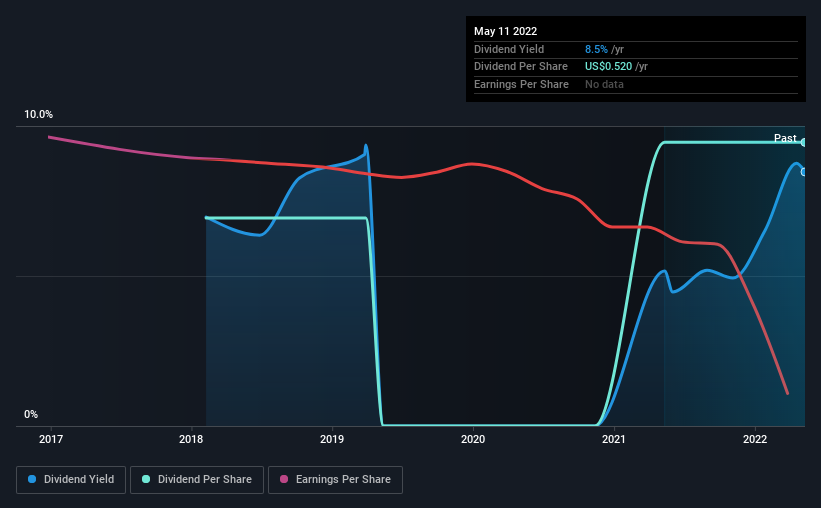

FAT Brands Inc. (NASDAQ:FAT) has announced that it will pay a dividend of US$0.13 per share on the 1st of June. This makes the dividend yield 11%, which will augment investor returns quite nicely.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. FAT Brands' stock price has reduced by 45% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

View our latest analysis for FAT Brands

FAT Brands' Distributions May Be Difficult To Sustain

If the payments aren't sustainable, a high yield for a few years won't matter that much. Even though FAT Brands is not generating a profit, it is still paying a dividend. The company is also yet to generate cash flow, so the dividend sustainability is definitely questionable.

Looking forward, earnings per share is forecast to rise by 20.3% over the next year. This is the right direction to be moving, but it is not enough to achieve profitability. Unless this happens fairly soon, the dividend could start to come under pressure.

FAT Brands' Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. The first annual payment during the last 4 years was US$0.38 in 2018, and the most recent fiscal year payment was US$0.52. This means that it has been growing its distributions at 8.1% per annum over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. FAT Brands might have put its house in order since then, but we remain cautious.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. FAT Brands' earnings per share has shrunk at 79% a year over the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this becomes a long term trend.

The company has also been raising capital by issuing stock equal to 11% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

We're Not Big Fans Of FAT Brands' Dividend

In summary, while it is good to see that the dividend hasn't been cut, we think that at current levels the payment isn't particularly sustainable. The company isn't making enough to be paying as much as it is, and the other factors don't look particularly promising either. Overall, the dividend is not reliable enough to make this a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, FAT Brands has 5 warning signs (and 2 which make us uncomfortable) we think you should know about. Is FAT Brands not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:FAT

FAT Brands

A multi-brand restaurant franchising company, acquires, develops, markets, and manages quick service, fast casual, casual dining, and polished casual dining restaurant concepts in the United States and internationally.

Undervalued moderate.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor