Advertisement

- United States

- /

- Hospitality

- /

- NasdaqCM:DENN

Earnings Beat: Denny's Corporation Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

Last week, you might have seen that Denny's Corporation (NASDAQ:DENN) released its annual result to the market. The early response was not positive, with shares down 7.0% to US$20.00 in the past week. It looks like a credible result overall - although revenues of US$541m were in line with what analysts predicted, Denny's surprised by delivering a statutory profit of US$1.90 per share, a notable 15% above expectations. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether analysts have changed their earnings models, following these results.

See our latest analysis for Denny's

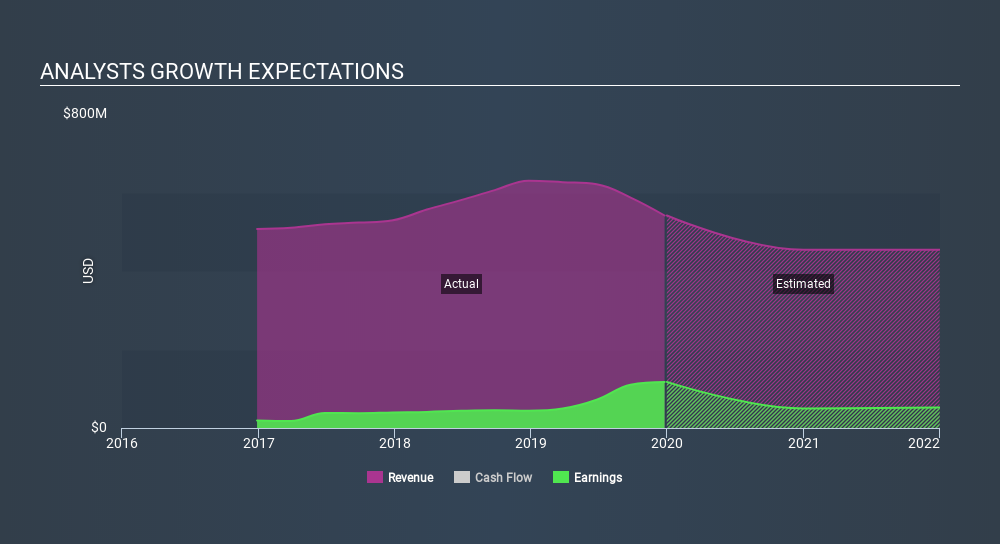

After the latest results, the consensus from Denny's's six analysts is for revenues of US$453.9m in 2020, which would reflect an uncomfortable 16% decline in sales compared to the last year of performance. Statutory earnings per share are expected to crater 55% to US$0.87 in the same period. Before this earnings report, analysts had been forecasting revenues of US$424.0m and earnings per share (EPS) of US$0.85 in 2020. So there seems to have been a moderate uplift in analyst sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

Although analysts have upgraded their earnings estimates, there was no change to the consensus price target of US$24.70, suggesting that the forecast performance does not have a long term impact on the company's valuation There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Denny's analyst has a price target of US$27.00 per share, while the most pessimistic values it at US$21.00. Still, with such a tight range of estimates, it suggests analysts have a pretty good idea of what they think the company is worth.

Another way to assess these estimates is by comparing them to past performance, and seeing whether analysts are more or less bullish relative to other companies in the market. We would highlight that sales are expected to reverse, with the forecast 16% revenue decline a notable change from historical growth of 5.4% over the last five years. Compare this with our data, which suggests that other companies in the same market are, in aggregate, expected to see their revenue grow 7.5% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Denny's to grow slower than the wider market.

The Bottom Line

The biggest takeaway for us from these new estimates is that the consensus upgraded its earnings per share estimates, showing a clear improvement in sentiment around Denny's's earnings potential next year. Fortunately, analysts also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Denny's going out to 2021, and you can see them free on our platform here..

You can also view our analysis of Denny's's balance sheet, and whether we think Denny's is carrying too much debt, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqCM:DENN

Denny's

Through its subsidiaries, owns and operates franchised full-service restaurant chains under the Denny's and Keke’s Breakfast Cafe brand names in the United States and internationally.

Good value low.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor