- United States

- /

- Hospitality

- /

- NasdaqGS:DASH

DoorDash (NasdaqGS:DASH) Reports Robust Earnings Growth in Q1 2025

Reviewed by Simply Wall St

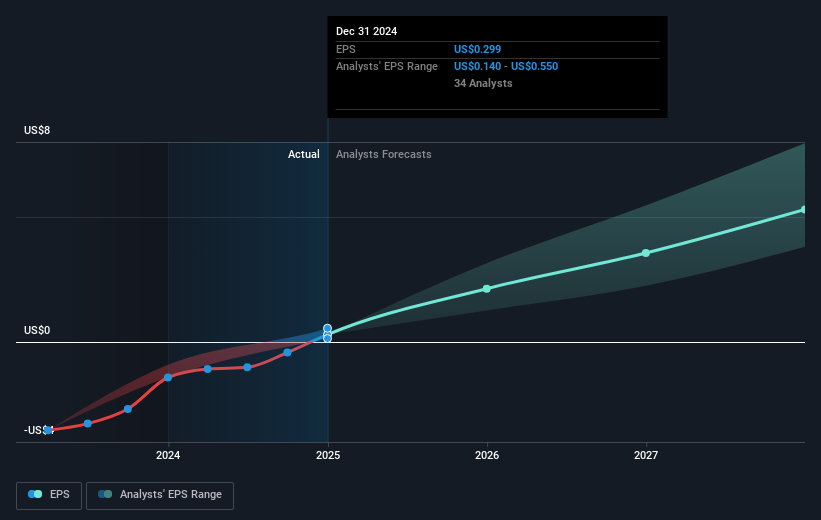

DoorDash (NasdaqGS:DASH) recently reported a significant improvement in its earnings, highlighting a robust sales growth and a return to profitability for the first quarter of 2025. Despite these positive financial results, the announced buyback remained stalled, showing zero progress. Coupled with proposed governance amendments, these events collectively offered investor insight into the company's operational and strategic directions. DoorDash's 11% price increase over the last week aligns with broader market trends, which saw gains as trade tensions eased and key economic data remained positive. The company's developments added weight to the optimistic sentiment reflected in numerous market indices' advances.

Be aware that DoorDash is showing 1 risk in our investment analysis.

The recent positive earnings report for DoorDash, coupled with significant sales growth and a turnaround to profitability, is likely to bolster investor confidence and align well with the company's international expansion efforts and technological advancements. However, the stalled buyback program and governance amendments may raise questions about DoorDash's capital allocation efficiency, potentially influencing future revenue and earnings projections as the company balances expansion with shareholder returns.

Over the longer term, DoorDash's shares have delivered a remarkable total return of 209.35% over three years. In contrast, over the past year, DoorDash outperformed both the US market, which returned 10.6%, and the broader US Hospitality industry, which returned 13.2%. These returns reflect the company's successful growth initiatives and market positioning.

In the context of its current share price of US$190.11, the analyst consensus price target of US$218.70 suggests a potential upside of 13.1%. This indicates that investors may see further growth opportunities if DoorDash successfully leverages its acquisitions of Deliveroo and SevenRooms. Such strategic moves could expand revenue streams and enhance earnings. However, analysts remain divided, which points to potential uncertainties in achieving these targets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade DoorDash, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DASH

DoorDash

Operates a commerce platform that connects merchants, consumers, and independent contractors in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Community Narratives