Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:BKNG

Analysts Just Made A Captivating Upgrade To Their Booking Holdings Inc. (NASDAQ:BKNG) Forecasts

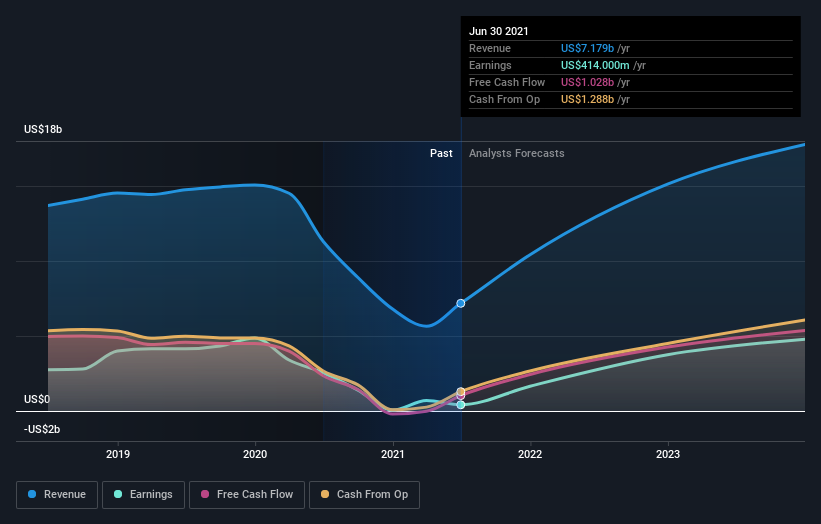

Booking Holdings Inc. (NASDAQ:BKNG) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

Following the upgrade, the current consensus from Booking Holdings' 29 analysts is for revenues of US$10b in 2021 which - if met - would reflect a substantial 45% increase on its sales over the past 12 months. Statutory earnings per share are presumed to soar 299% to US$40.32. Prior to this update, the analysts had been forecasting revenues of US$9.3b and earnings per share (EPS) of US$30.32 in 2021. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for Booking Holdings

Despite these upgrades, the analysts have not made any major changes to their price target of US$2,561, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Booking Holdings, with the most bullish analyst valuing it at US$3,100 and the most bearish at US$1,890 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. One thing stands out from these estimates, which is that Booking Holdings is forecast to grow faster in the future than it has in the past, with revenues expected to display 111% annualised growth until the end of 2021. If achieved, this would be a much better result than the 3.9% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 20% annually. Not only are Booking Holdings' revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Some investors might be disappointed to see that the price target is unchanged, but we feel that improving fundamentals are usually a positive - assuming these forecasts are met! So Booking Holdings could be a good candidate for more research.

Analysts are clearly in love with Booking Holdings at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as its declining profit margins. For more information, you can click through to our platform to learn more about this and the 2 other risks we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade Booking Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Booking Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:BKNG

Booking Holdings

Provides online and traditional travel and restaurant reservations and related services in the United States, the Netherlands, and internationally.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor