Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:WMT

Walmart (WMT): Examining the Retail Giant’s Valuation After a Flat Trading Session

Simply Wall St

Reviewed by Kshitija Bhandaru

The latest trading session for Walmart (WMT) closed with little movement, leaving investors to assess what is next for the retail giant. Despite flat returns over the past week, Walmart’s long-term performance remains a point of interest.

See our latest analysis for Walmart.

Walmart’s share price has edged up more than 13% year-to-date, underscoring gradual but steady momentum after a year marked by resilient consumer demand and efficiency pushes. Even more telling, shareholders have seen a robust 28% total return over the past twelve months, which helps reinforce Walmart’s reputation for delivering value in both the short and long run.

If you’re looking to broaden your investing horizons beyond retail, now is a great time to discover fast growing stocks with high insider ownership

With Walmart continuing to deliver strong returns and modest growth, the question remains: is the current share price reflecting the company’s true potential, or could there still be room for savvy investors to benefit?

Most Popular Narrative: 9% Undervalued

With analysts setting Walmart’s fair value at $112 and the market closing at $101.84, sentiment sees untapped potential still priced in.

Expansion of high-margin business streams such as Walmart Connect (advertising, up 31-46% globally), marketplace, and Walmart+ memberships (global advertising up 46%, membership income up 15%) is diversifying Walmart's income base beyond retail. This is gradually transforming the company's profit mix and resulting in structurally higher net margins and earnings over time.

Curious what’s fueling that bold valuation forecast? It’s not just retail strength. The narrative hints at critical margin shifts and future income streams that could transform Walmart’s financial trajectory. One assumption underpins everything. Uncover the big story details that are moving the market’s view.

Result: Fair Value of $112 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent international losses and rising delivery costs could slow Walmart's margin gains and present challenges to upbeat forecasts if left unresolved.

Find out about the key risks to this Walmart narrative.

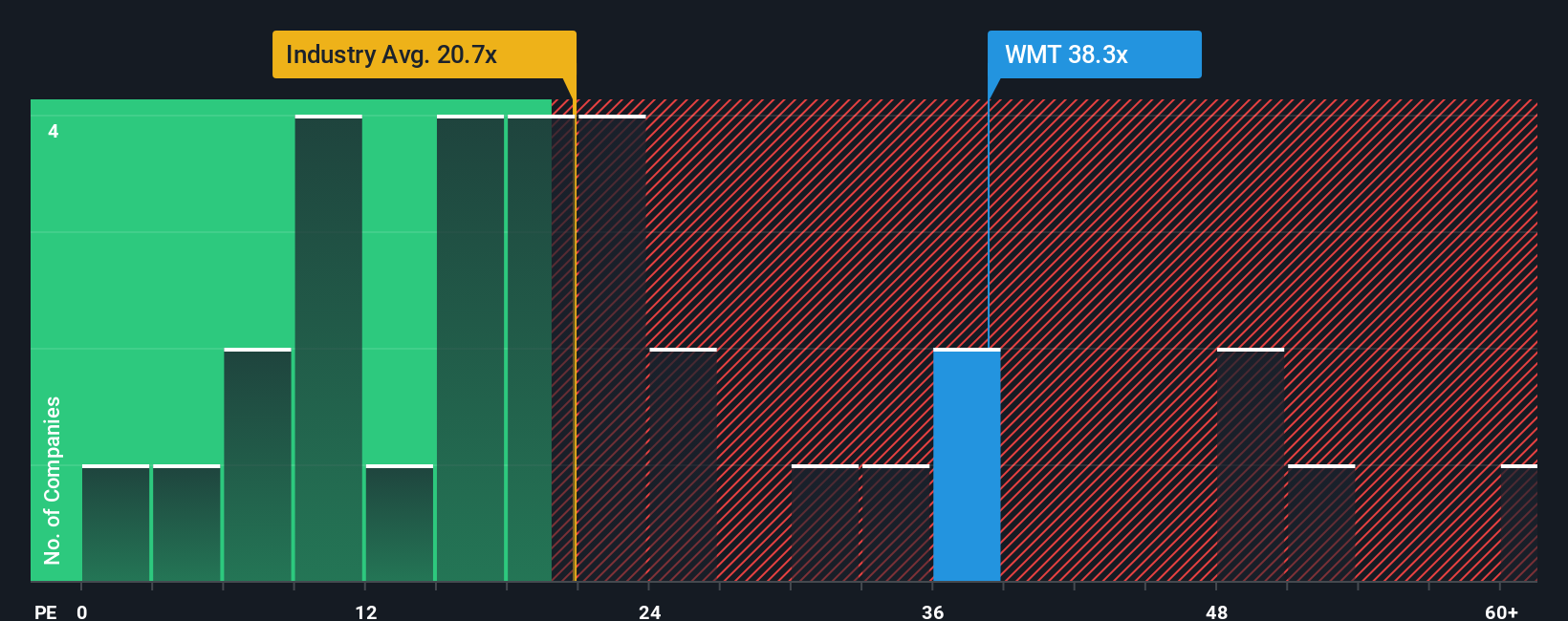

Another View: Multiples Tell a Different Story

While analysts see Walmart as undervalued based on future cash flows, a look at its current price-to-earnings ratio reveals a much pricier picture. Walmart trades at 38x earnings, noticeably higher than the industry average of 20.5x and the fair ratio of 31.9x. This gap highlights potential valuation risk if growth does not keep pace. Is the market overly optimistic, or is Walmart’s premium deserved?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Walmart Narrative

If you’d rather investigate the numbers yourself or shape your own interpretation, you can easily build your own Walmart narrative in just a few minutes: Do it your way

A great starting point for your Walmart research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Open up your portfolio to more possibilities with these standout stock themes, each engineered for growth and staying ahead of the market.

- Grow your wealth with consistent income by tapping into these 19 dividend stocks with yields > 3%, which offers yields over 3% and financial resilience.

- Catalyze your gains by targeting innovation with these 24 AI penny stocks, focused on the fast-evolving artificial intelligence space.

- Amplify your strategy with hidden value by exploring these 892 undervalued stocks based on cash flows, featuring stocks trading below their potential based on real cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Walmart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WMT

Walmart

Engages in the operation of retail and wholesale stores and clubs, eCommerce websites, and mobile applications worldwide.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor