Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:NGVC

Natural Grocers by Vitamin Cottage (NYSE:NGVC) Will Pay A Dividend Of $0.10

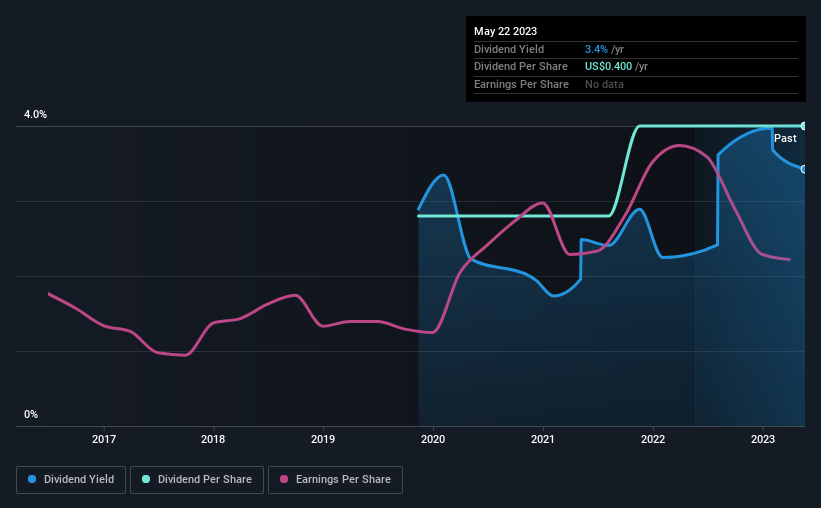

The board of Natural Grocers by Vitamin Cottage, Inc. (NYSE:NGVC) has announced that it will pay a dividend on the 14th of June, with investors receiving $0.10 per share. The dividend yield will be 3.4% based on this payment which is still above the industry average.

View our latest analysis for Natural Grocers by Vitamin Cottage

Natural Grocers by Vitamin Cottage's Dividend Is Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, Natural Grocers by Vitamin Cottage was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. The company is clearly earning enough to pay this type of dividend, but it is definitely focused on returning cash to shareholders, rather than growing the business.

If the trend of the last few years continues, EPS will grow by 9.2% over the next 12 months. If the dividend continues on this path, the payout ratio could be 66% by next year, which we think can be pretty sustainable going forward.

Natural Grocers by Vitamin Cottage Is Still Building Its Track Record

Looking back, the dividend has been stable, but the company hasn't been paying a dividend for very long so we can't be confident that the dividend will remain stable through all economic environments. The dividend has gone from an annual total of $0.28 in 2020 to the most recent total annual payment of $0.40. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend Has Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Natural Grocers by Vitamin Cottage has seen EPS rising for the last five years, at 9.2% per annum. Shareholders are getting plenty of the earnings returned to them, which combined with strong growth makes this quite appealing.

In Summary

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. The low payout ratio is a redeeming feature, but generally we are not too happy with the payments Natural Grocers by Vitamin Cottage has been making. We don't think Natural Grocers by Vitamin Cottage is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 2 warning signs for Natural Grocers by Vitamin Cottage that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Natural Grocers by Vitamin Cottage might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NGVC

Natural Grocers by Vitamin Cottage

Natural Grocers by Vitamin Cottage, Inc., together with its subsidiaries, retails natural and organic groceries, and dietary supplements in the United States.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor