Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:GRDN

Guardian Pharmacy Services (GRDN): Assessing Valuation After Recent Share Price Volatility

Simply Wall St

Reviewed by Kshitija Bhandaru

Guardian Pharmacy Services (GRDN) has been catching some attention lately, with its shares moving around over the past month. Investors seem to be sizing up the company’s recent performance and are looking for hints on where it might be headed next.

See our latest analysis for Guardian Pharmacy Services.

Zooming out, Guardian Pharmacy Services’ recent volatility comes on the heels of strong year-to-date momentum. The share price is up over 20% since January, while its 1-year total shareholder return is an impressive 39.9%. That kind of performance suggests investors see both growth potential and fresh catalysts on the horizon, even after a bumpy last month.

If today’s moves have you looking for your next opportunity, this could be the right time to explore fast growing stocks with high insider ownership.

With shares trading about 21% below analyst price targets and after recent strong gains, the big question is whether Guardian Pharmacy Services is undervalued, or if the market has already priced in all the potential upside.

Price-to-Sales of 1.1x: Is it justified?

At the last close of $24, Guardian Pharmacy Services trades at a price-to-sales ratio of 1.1x, noticeably higher than its sector peers and industry averages. This raises questions about whether the current premium is warranted, especially given recent performance figures.

The price-to-sales (P/S) ratio measures how much investors are willing to pay for each dollar of a company’s sales. For a business like Guardian Pharmacy Services operating within Consumer Retailing, this multiple can provide insight into how the market views its revenue-generating potential compared to competitors and industry norms.

The company’s P/S multiple not only outpaces the peer group average (0.2x), but also stands well above the U.S. Consumer Retailing industry average (0.4x). In fact, the statistically estimated fair P/S ratio for Guardian is just 0.3x. This suggests the current valuation embeds aggressive expectations. If sentiment shifts, this multiple could move closer to fair value levels.

Explore the SWS fair ratio for Guardian Pharmacy Services

Result: Price-to-Sales of 1.1x (OVERVALUED)

However, slowing revenue growth and significant recent losses could dampen optimism, particularly if investor sentiment shifts in response to changing market dynamics.

Find out about the key risks to this Guardian Pharmacy Services narrative.

Another View: What About the SWS DCF Model?

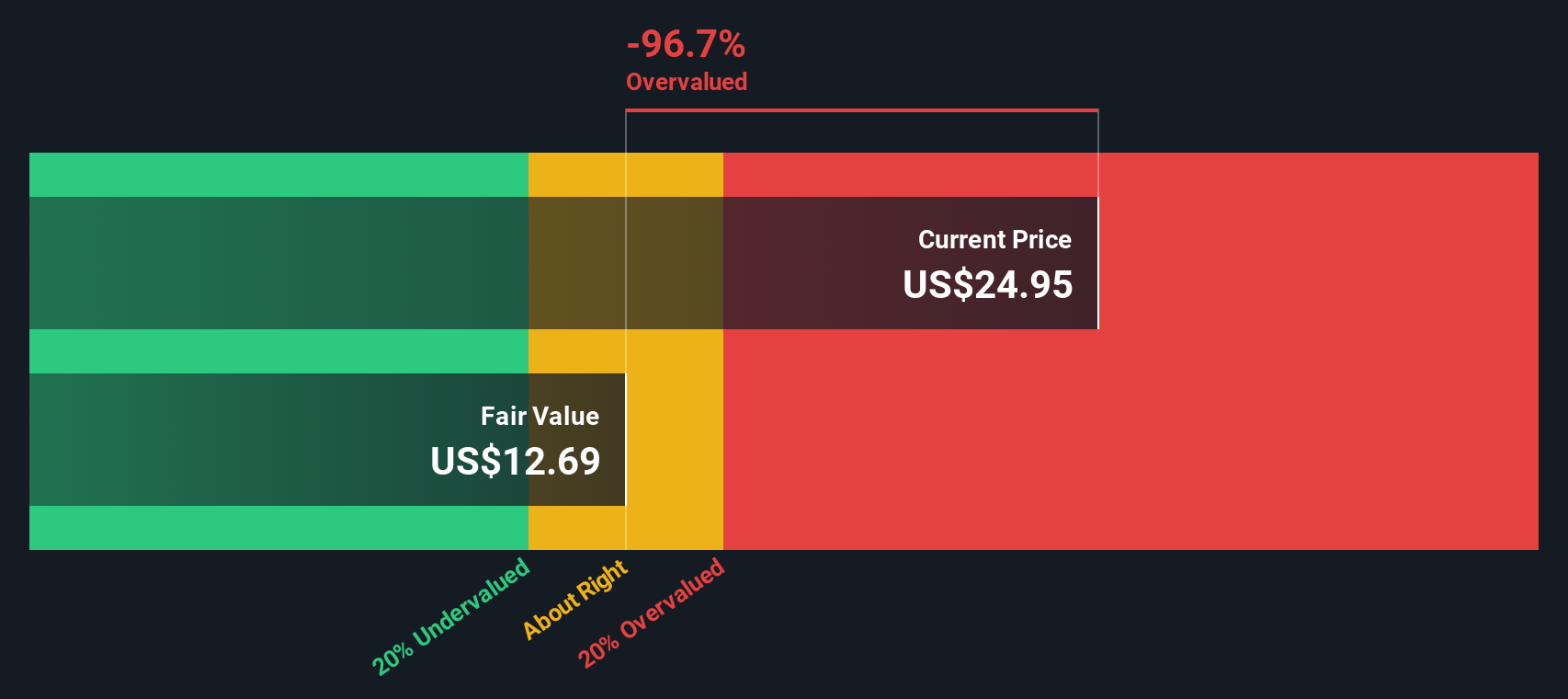

Looking through the lens of our DCF model, Guardian Pharmacy Services appears significantly overvalued, trading well above its estimated fair value of $12.67 per share. This approach, which projects future cash flows, challenges the optimism built into the price-to-sales multiple. Could the current market enthusiasm be overestimating the company’s near-term prospects?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Guardian Pharmacy Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Guardian Pharmacy Services Narrative

If you see things differently or want to dive into the numbers on your own terms, you can build a custom narrative in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Guardian Pharmacy Services.

Looking for more investment ideas?

Take your investing game to the next level by checking out proven strategies on Simply Wall Street. You could stumble on something that reshapes your portfolio.

- Tap into market shifts by reviewing these 893 undervalued stocks based on cash flows, which are currently trading below their true worth and may be poised for a potential rebound.

- Catch emerging growth by browsing these 25 AI penny stocks, which are set to capitalize on the rise of artificial intelligence across industries.

- Grow your wealth steadily by checking out these 18 dividend stocks with yields > 3%, designed to provide consistent income and financial resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GRDN

Guardian Pharmacy Services

A pharmacy service company, provides a suite of technology-enabled services to help residents of long-term health care facilities (LTCFs) in the United States.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.4% undervalued

TR

Community Contributor