- United States

- /

- Food and Staples Retail

- /

- NYSE:ACI

Does Albertsons Stock Offer Value After Its 12% Decline in 2025?

Reviewed by Bailey Pemberton

If you’re sitting on the fence about Albertsons Companies, you’re not alone. The grocery giant’s stock closed at $17.38 recently, and investors are wondering if now is the moment to buy, hold, or wait for a better price. Recent price action has been anything but dull: in the last week alone, Albertsons stock dipped by 1.0%, deepening a 10.0% slide over the past month. The stock is down 11.6% so far this year, which might feel discouraging, but if you take a step back, the 81.8% gain over the past five years tells a very different story. Clearly, there have been ups and downs, and like most in the retail world, Albertsons faces a complex mix of market trends, shifting consumer habits, and broader economic shifts that are always in play. This is especially true with competition and food inflation making waves across the sector.

What really catches the eye, though, is Albertsons’ valuation score. Out of six major checks for undervaluation, Albertsons passes every single one, scoring a standout 6. That is not something you see every day, especially in an industry known for razor-thin margins. In the sections ahead, I’ll break down the common approaches investors use to size up a company’s value, showing how Albertsons measures up. Then, I’ll introduce a way to look at valuation that goes even deeper, giving you the real story behind whether this low-priced stock is truly worth your investment.

Why Albertsons Companies is lagging behind its peers

Approach 1: Albertsons Companies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This approach provides a grounded way to assess what a business is truly worth, using professional forecasts and logical assumptions around growth and risk.

For Albertsons Companies, the DCF model is built from both analyst estimates and further long-term projections. The company reported a Last Twelve Months (LTM) Free Cash Flow of $409.26 million. Analysts provide forecasts for the next five years, after which projections continue based on expected trends. Cash flow is set to grow significantly, with projections reaching $1.62 billion by 2030. This growth path highlights optimism about Albertsons’ operational efficiency and its ability to generate cash in a competitive industry.

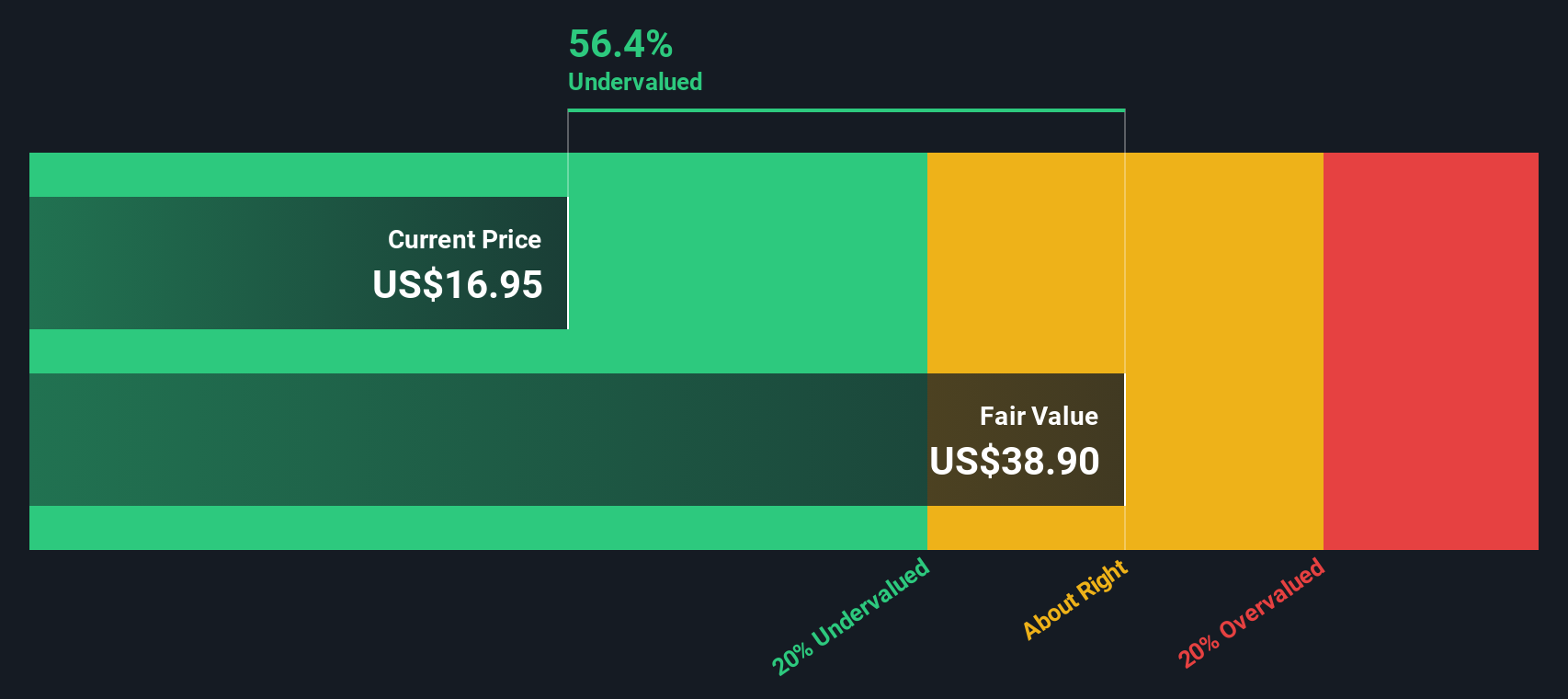

Based on these projections, the model concludes that the fair value of Albertsons shares is $39.38. With the recent share price closing at $17.38, this points to a substantial discount, as shares are trading at 55.9% below their estimated intrinsic value. This level of undervaluation is rare for a major retail player and suggests the market may be overlooking the company’s financial strength and future prospects.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Albertsons Companies is undervalued by 55.9%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Albertsons Companies Price vs Earnings

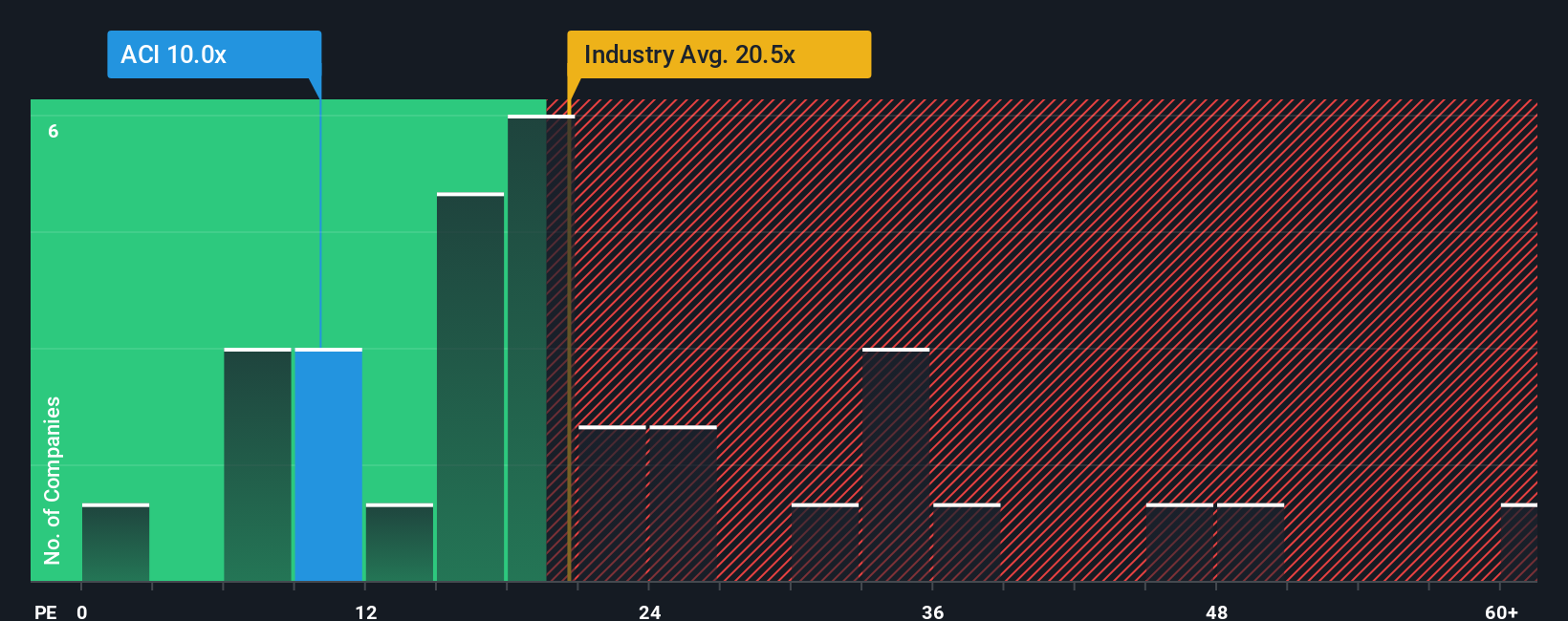

For profitable companies like Albertsons, the Price-to-Earnings (PE) ratio is a tried-and-true method to gauge whether shares are priced fairly. This ratio reflects how much investors are currently paying for each dollar of the company’s earnings, making it especially relevant for established firms turning a steady profit.

It’s important to note that a "normal" PE ratio isn't one-size-fits-all. Growth expectations, company-specific risks, and broader market sentiment all play a role. Higher growth and lower risk typically justify a higher PE, while slower growth or more uncertainty tend to pull the ratio down.

Right now, Albertsons trades at a PE of 10.2x, which stands well below both its industry average of 21.0x and the average PE among its peer group, which is 23.7x. This could indicate that the market is skeptical about the company’s future or simply overlooking its performance. To address this, Simply Wall St’s "Fair Ratio" offers a more nuanced benchmark. It factors in Albertsons’ unique drivers, such as growth forecasts, profit margins, industry context, and risk profile, to suggest a fair PE of 17.5x.

The Fair Ratio moves beyond basic peer or industry comparisons by accounting for the very things that make each business unique. That means you get a more tailored view, instead of a one-size-fits-all average that may not reflect Albertsons’ specific strengths or challenges.

With Albertsons’ current PE at 10.2x and its Fair Ratio at 17.5x, the shares screen as undervalued using this approach too. There is a meaningful gap, suggesting the market may be underpricing the company’s true earnings power and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Albertsons Companies Narrative

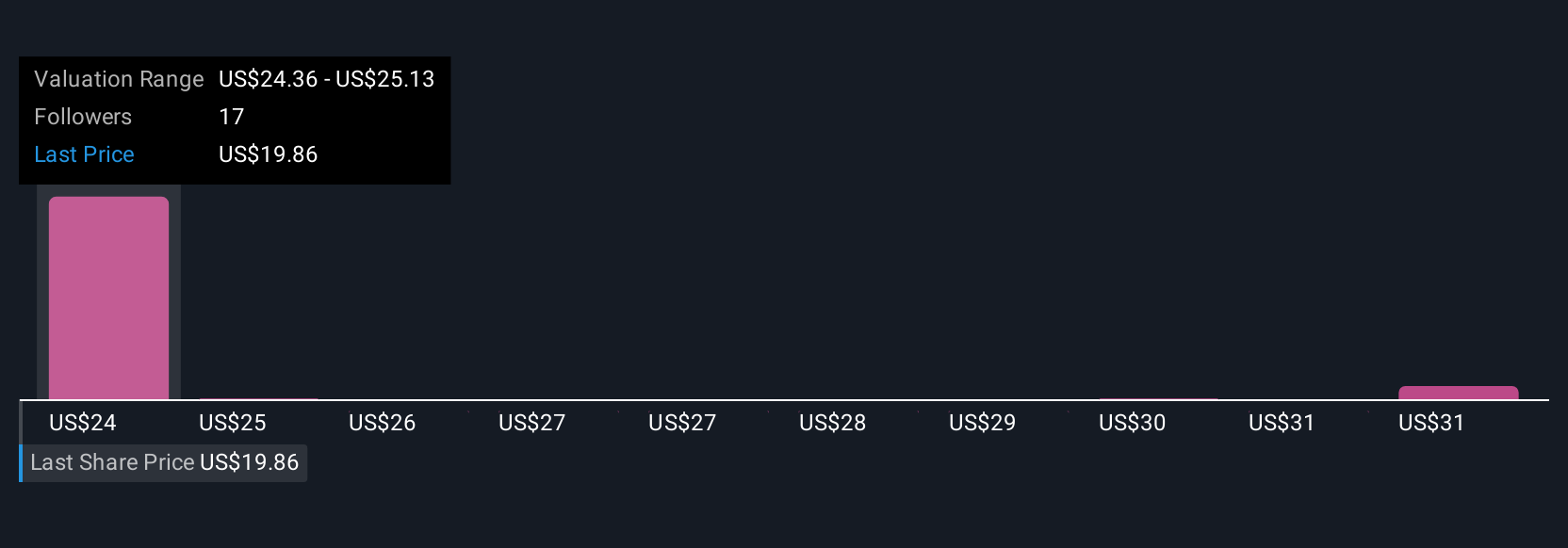

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story about a company, your beliefs about where it’s headed, linked directly to your assumptions for future revenue, profits, and margins. Instead of just looking at past numbers or a single price target, Narratives let you express your perspective on what you think drives Albertsons’ value, connect that story to financial forecasts, and immediately see what those views imply for fair value.

Narratives are available right on Simply Wall St’s Community page, where millions of investors use them to create, share, and compare viewpoints. They’re easy to update and dynamic, so if a news release or earnings update changes the outlook, your Narrative and its fair value automatically reflect the new info. Narratives make it easier to decide when to buy or sell, since you can directly compare your calculated Fair Value to today’s share price and see why views differ.

For example, Albertsons' analyst consensus Narrative currently estimates a fair value of $24.06, about 22.6% above the current share price, while the most bullish users see $28.00 and the most bearish see only $19.00. This helps you weigh different perspectives instantly.

Do you think there's more to the story for Albertsons Companies? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ACI

Albertsons Companies

Through its subsidiaries, operates in the food and drug retail industry in the United States.

Very undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion