Grocery Outlet Holding (GO) has caught investor attention recently, not because of a headline-grabbing event but due to ongoing share price shifts that prompt some tough questions. While there has not been a specific catalyst driving the latest move, the changes in valuation and market sentiment might be more significant than they first appear. For investors weighing what comes next, now could be a pivotal moment to reconsider the fundamental outlook of this discount retailer.

Looking at the bigger picture, Grocery Outlet Holding’s share price has been on a bumpy ride. After some sharp swings earlier in the year, the stock is down more than 10% over the past 12 months and remains well below its price from three or five years ago. However, it has rebounded nearly 25% in the past three months. Revenue has grown steadily, and its net income is up strongly, but market momentum has only just started to recover from a long slump.

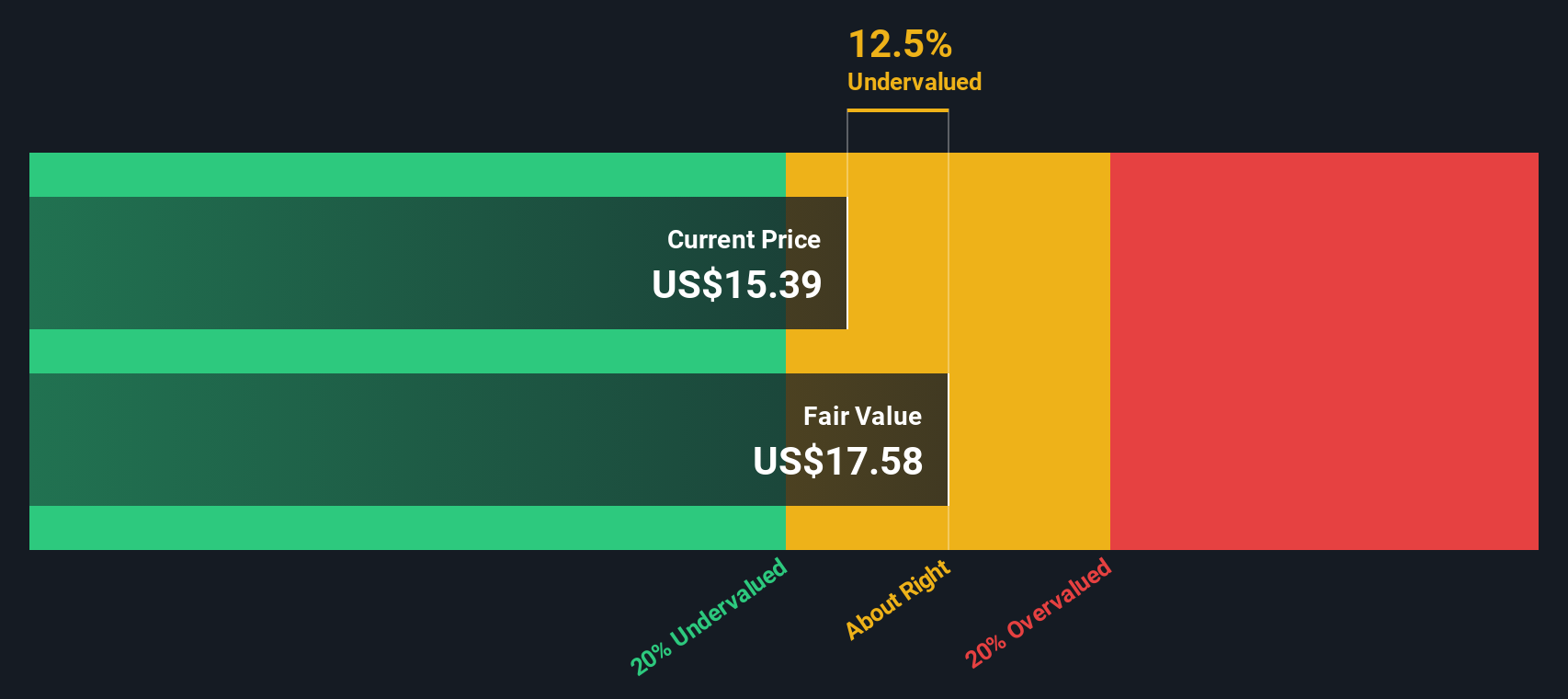

The real question for investors now is whether this recent pickup signals an undervalued opportunity or if the market is just baking in future growth expectations already. Is this a bargain, or is it fully priced?

Advertisement

Most Popular Narrative: 1.9% Undervalued

The most widely followed narrative positions Grocery Outlet Holding as slightly undervalued, suggesting that the current share price does not fully reflect its long-term growth potential and margin expansion.

Analysts are assuming Grocery Outlet Holding's revenue will grow by 8.3% annually over the next 3 years. Analysts assume that profit margins will increase from 0.2% today to 1.5% in 3 years time.

Think you know what’s powering this call? The fair value depends on projections that could influence both sales and profit. Will Grocery Outlet actually deliver on these big expectations? Explore the full narrative to see the bold quantitative targets and the aggressive future margins being considered.

However, persistent competition and shifting consumer habits could quickly challenge this outlook. This may make future growth less certain than current forecasts suggest.

Another View: SWS DCF Model Says Shares Are Overvalued

While the popular narrative suggests Grocery Outlet Holding is undervalued, our DCF model comes to the opposite conclusion and signals that the current share price is actually above fair value. Which method do you trust more?

If you have a different take, or simply want to use your own data-driven approach, you can craft your own analysis in just a few minutes. Do it your way.

A great starting point for your Grocery Outlet Holding research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t leave your next big opportunity on the table. With the right tools, you can spot hidden winners and shape your portfolio for the trends ahead.

Spot under-the-radar bargains by unlocking potential with undervalued stocks based on cash flows. This is perfect for those seeking strong value before the crowd catches on.

Boost your income stream by tapping into reliable picks through dividend stocks with yields > 3%, focusing on companies with yields that can enhance your returns.

Ride the future of healthcare innovation and see which stocks are shaping tomorrow’s breakthroughs with healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks