Advertisement

- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:DLTR

Dollar Tree (DLTR) Margin Drop to 5.9% Undercuts Bullish Growth Narratives

Simply Wall St

Reviewed by Simply Wall St

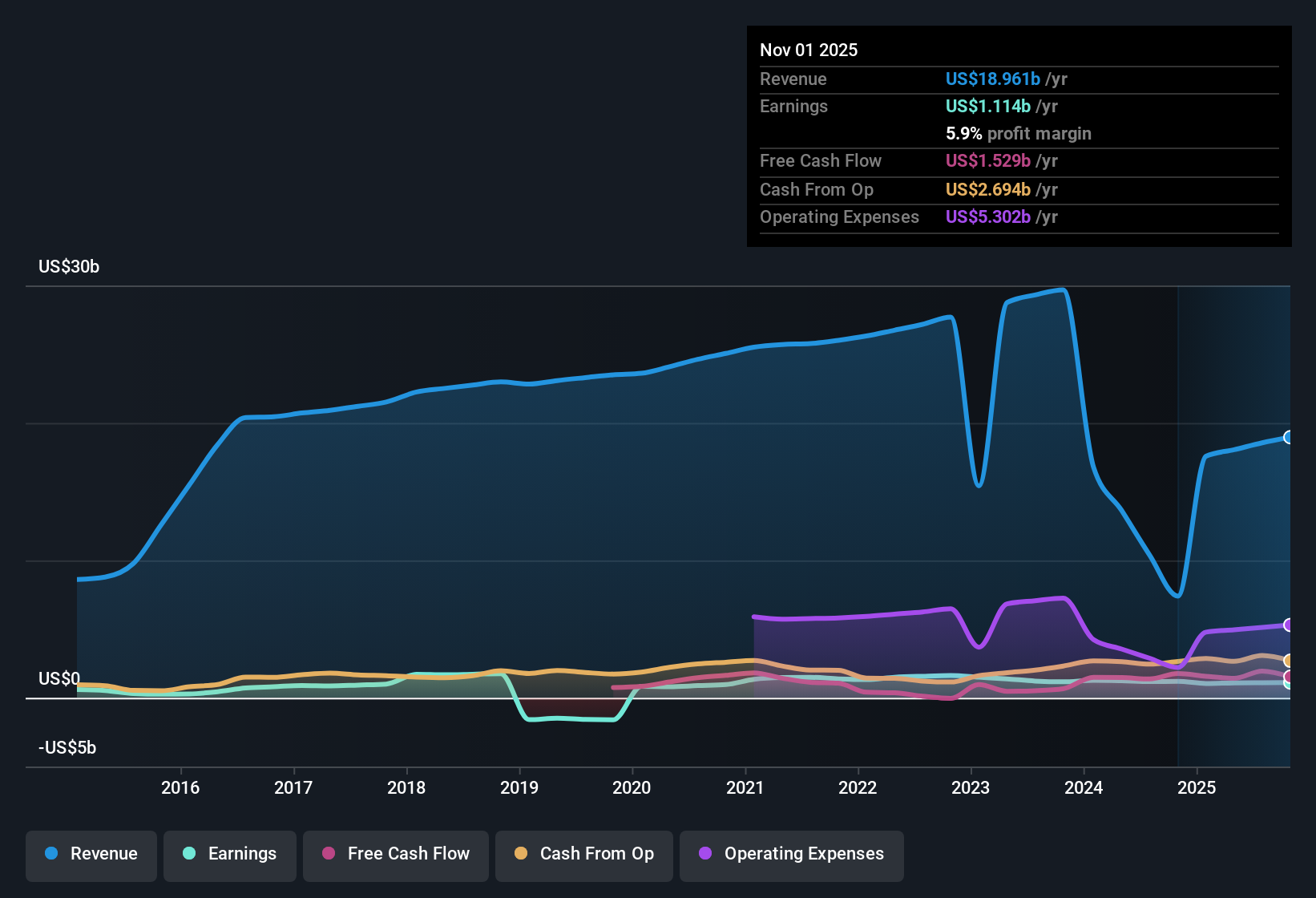

Dollar Tree (DLTR) kicked off its latest earnings update with Q2 2026 revenue of about $4.6 billion and EPS of $0.75, setting the tone for how investors digest a year that has seen both growth plans and profitability put under the microscope. The company has seen revenue move from $4.1 billion in Q2 2025 to $4.6 billion in Q2 2026, while quarterly EPS over that span has ranged from $0.66 to $1.86. This gives investors a clear view of how the top line and earnings power have tracked into the current release as margins come back into focus.

See our full analysis for Dollar Tree.With the latest numbers on the table, the next step is to line them up against the dominant narratives around Dollar Tree’s growth and margin story to see which views hold up and which need a rethink.

See what the community is saying about Dollar Tree

Same store sales up 6.5%

- Comparable sales growth accelerated to 6.5% in Q2 2026, up from 5.4% in Q1 2026 and 1.3% in Q2 2025, pointing to stronger traffic and basket trends at the core Dollar Tree banner.

- Consensus narrative highlights store growth and multi price assortments as key sales drivers, and the step up in same store sales from roughly 1 to over 6 percent aligns with that bullish angle, though:

- Quarterly revenue only moved from about $4.1 billion in Q2 2025 to $4.6 billion in Q2 2026, so most of the lift is coming off a relatively modest base.

- Analysts also flag consumer cost of living pressures, which could make sustaining mid single digit comps harder even as value focused traffic remains a tailwind.

Bulls argue that these comp gains signal a durable shift in shopper behavior toward Dollar Tree, but the latest numbers still need to prove they can power long term earnings growth. 🐂 Dollar Tree Bull Case

Margins under pressure at 5.9%

- On a trailing 12 month basis, net profit margin sits at 5.9%, down sharply from 11.3% a year earlier, even though TTM net income excluding extra items is still a solid $1.1 billion on about $18.6 billion of revenue.

- Bears focus on mounting cost pressures and operational complexity, and the drop in margin backs that cautious view in several ways:

- Q2 2026 net income excluding extra items is $155.5 million on $4.6 billion of revenue, noticeably lower than the $313.5 million earned on $4.6 billion in Q1 2026, showing recent profitability compression.

- Five year earnings have declined about 4.6 percent per year, so the weaker margin trend is not just a one off and directly challenges expectations for smooth EPS growth.

Skeptics warn that cost inflation and the complexity of the multi price strategy could keep net margins closer to today’s 5 to 6 percent rather than snapping back quickly. 🐻 Dollar Tree Bear Case

Premium valuation versus DCF fair value

- The stock trades around $112.92 with a P E of about 20.7 times, above both the consumer retailing industry at roughly 20 times and peers at 19.6 times, while the DCF fair value cited is lower at $58.51.

- What stands out is how this valuation sits against a relatively modest growth outlook:

- Earnings are forecast to grow about 4.6 percent per year and revenue about 5.3 percent per year, which is slower than the 10.5 percent growth rate noted for the broader US market.

- Analysts’ longer term work implies EPS of $7.05 by 2028 and an implied price target of $108.78, so today’s price already leans toward the optimistic end of those expectations.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Dollar Tree on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Use your own lens on the data, shape a concise view in just a few minutes and Do it your way.

A great starting point for your Dollar Tree research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Dollar Tree’s slowing earnings growth, margin compression and arguably stretched valuation leave investors paying a premium for financial performance that is not clearly accelerating.

If you want price tags that better match fundamentals, use our these 908 undervalued stocks based on cash flows to quickly zero in on candidates where discounted cash flows point to more compelling upside today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DLTR

Dollar Tree

Operates retail discount stores under the Dollar Tree and Dollar Tree Canada brands in the United States and Canada.

Mediocre balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

42 followersusers have followed this narrative

6 commentsusers have commented on this narrative

14 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative