Advertisement

- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:CHEF

How Does Chefs' Warehouse Stack Up After Strategic Acquisitions and a 49.5% Stock Surge?

Reviewed by Bailey Pemberton

- Ever wondered whether Chefs' Warehouse is actually worth its current price tag? Let’s take a closer look at the signals behind the sticker.

- The stock has been on a real run this year, climbing 27.9% year-to-date and an impressive 49.5% over the past twelve months, hinting that investors are taking fresh interest.

- Recent headlines spotlighted the company’s strategic acquisition activity and growing market footprint, driving up optimism around its long-term prospects. Industry chatter also points to increased demand from high-end restaurants, which has helped fuel the latest rally.

- If you like to start with the numbers, Chefs' Warehouse scores a 3 out of 6 on our undervaluation checks. However, that’s only half the picture. Let’s dive into the usual approaches to valuation, and stick around for an even more insightful way to size up the stock at the end.

Approach 1: Chefs' Warehouse Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today. This accounts for the time value of money. In this case, the model uses the 2 Stage Free Cash Flow to Equity approach, which incorporates near-term analyst forecasts and longer-term extrapolations to outline Chefs' Warehouse's potential over time.

Currently, Chefs' Warehouse generates $71.7 million in Free Cash Flow. Analyst estimates project steady growth, and by 2028, Free Cash Flow is expected to reach $180 million. Looking further ahead, extrapolated figures suggest cash flows could surpass $203 million by 2035, with all values calculated in US dollars.

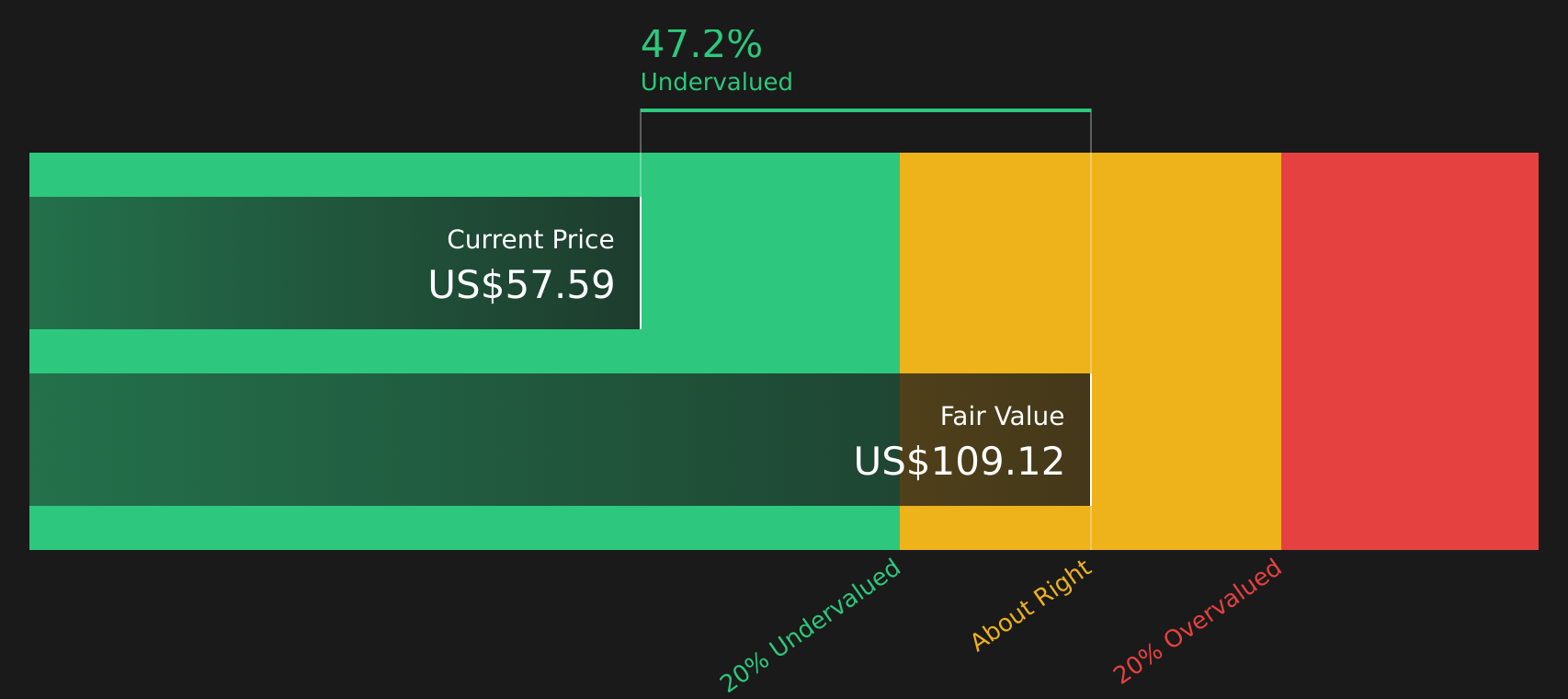

Based on these projections, the DCF analysis puts the intrinsic value of Chefs' Warehouse shares at $90.86. This implies the stock trades at a 30.1% discount to its fair value. This sizable undervaluation suggests substantial upside if the company's growth trajectory holds.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Chefs' Warehouse is undervalued by 30.1%. Track this in your watchlist or portfolio, or discover 838 more undervalued stocks based on cash flows.

Approach 2: Chefs' Warehouse Price vs Earnings

The price-to-earnings (PE) ratio is a classic valuation tool for profitable companies like Chefs' Warehouse. It lets investors quickly compare a company’s stock price to its earnings power. A "normal" or "fair" PE ratio varies across companies. It is typically higher when investors expect above-average growth or see less risk ahead, and lower for slower growers or more uncertain prospects.

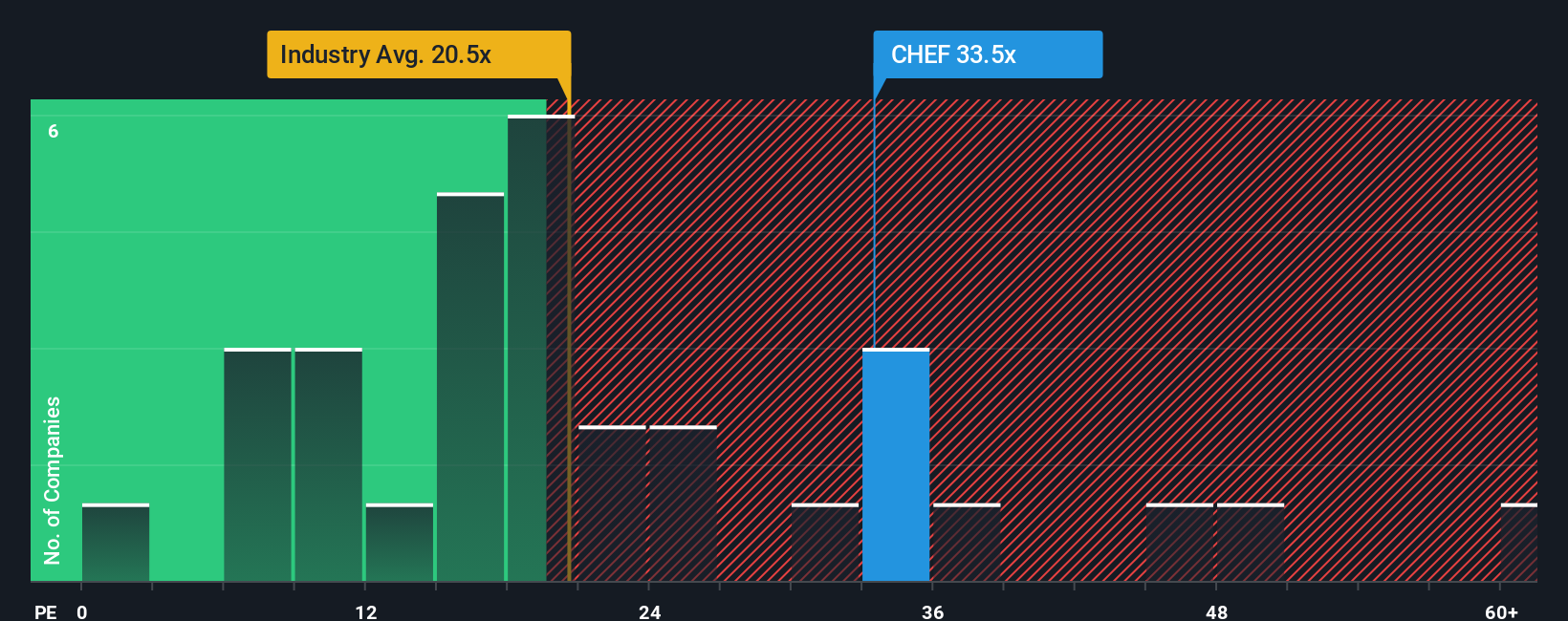

Chefs' Warehouse currently trades at 34.6x earnings. For context, this is noticeably above the Consumer Retailing industry average of 19.7x and also higher than the average PE for its direct peers, which sits at 26.2x. On the surface, this could suggest the stock is priced aggressively, given how much investors are willing to pay for each dollar of profit.

However, this is where Simply Wall St's “Fair Ratio” comes into play. Unlike a standard industry or peer comparison, the Fair Ratio digs deeper by factoring in Chefs' Warehouse's future earnings growth potential, profit margins, company size, and its risk profile. For Chefs' Warehouse, the Fair Ratio is 16.8x earnings. This holistic approach gives a more realistic sense of fair value instead of relying on a simple side-by-side multiple.

Comparing the actual PE of 34.6x with the Fair Ratio of 16.8x suggests Chefs' Warehouse stock may currently be overvalued based on these metrics.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1408 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Chefs' Warehouse Narrative

Earlier, we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. Rather than relying solely on numbers and ratios, a Narrative lets you tell your own story for a company by combining your unique perspective with forecasts, such as your expectations for Chefs' Warehouse’s future revenue, earnings, and margins. This approach directly links a company’s story to a financial forecast and, from there, to a calculated fair value, making the analysis more relevant and actionable for your own investment decisions.

On Simply Wall St, Narratives are an easy, accessible tool available within the Community page, used by millions of investors who want to bring their beliefs, research, and latest news together in one dynamic place. Narratives make it simple to decide when to buy or sell by comparing your assumed Fair Value with the current Price, updating dynamically as new information, like earnings releases or major news, becomes available. This ensures your assumptions are always current.

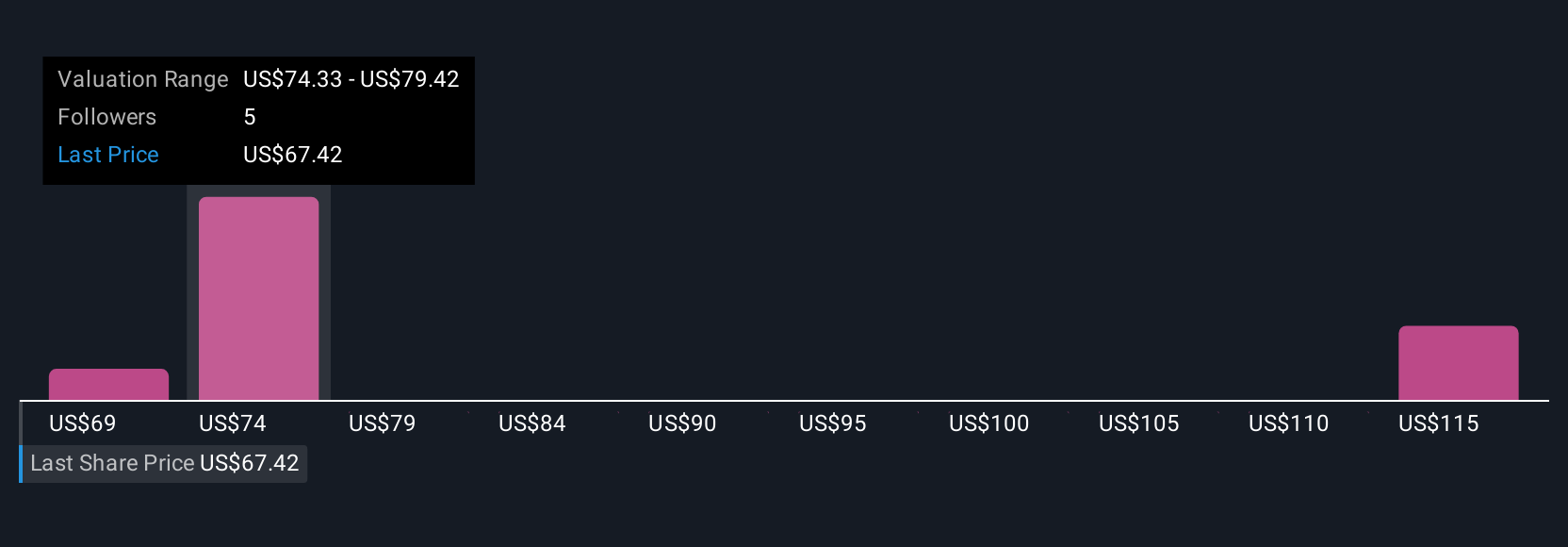

For example, with Chefs' Warehouse, some investors see big gains ahead if margin expansion and premium dining growth continue, giving them a Narrative-based fair value as high as $85 per share. Others worry about ongoing cost pressures and see a fair value closer to $66. Both perspectives shape individual investment decisions and keep analysis grounded in real-world expectations.

Do you think there's more to the story for Chefs' Warehouse? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CHEF

Chefs' Warehouse

Distributes specialty food and center-of-the-plate products in the United States, the Middle East, and Canada.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative