- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:CART

Instacart (CART): Evaluating Valuation as New Retail Partnerships Drive Broader Technology Adoption

Reviewed by Simply Wall St

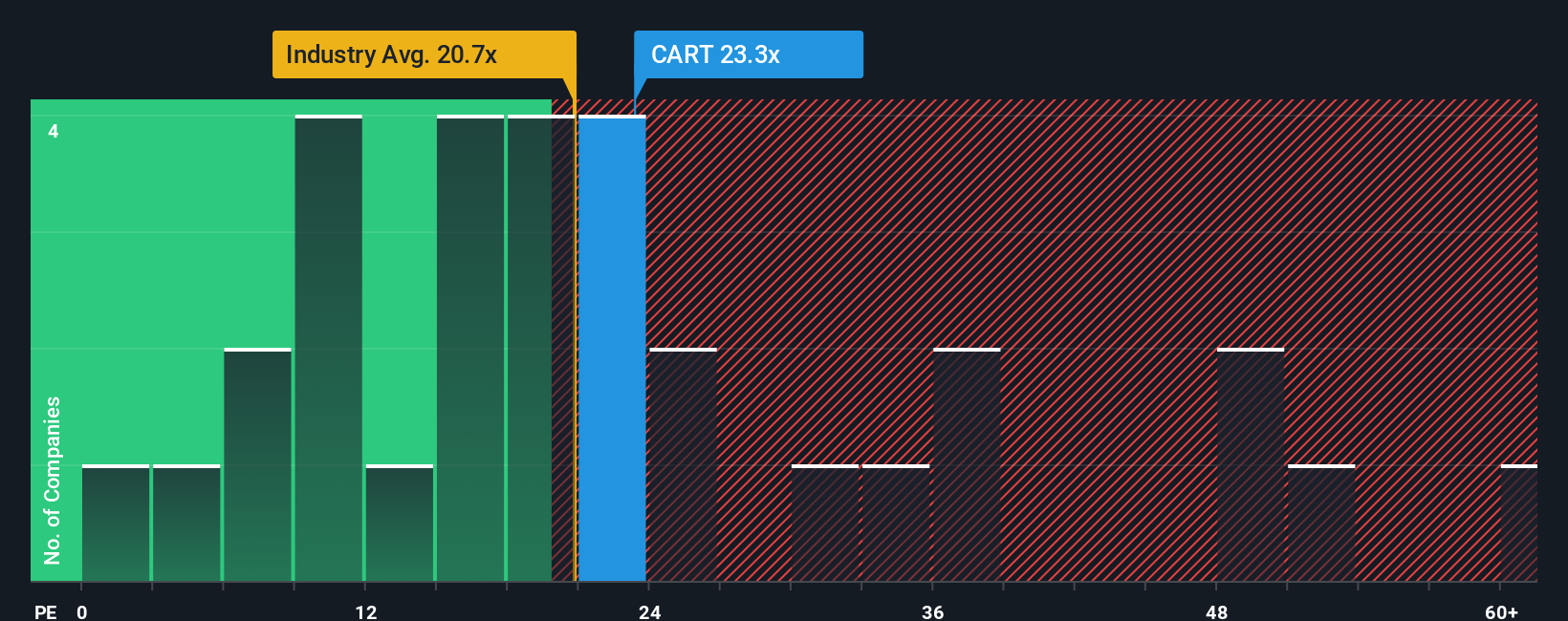

Most Popular Narrative: 24.6% Undervalued

The prevailing narrative sees Maplebear as materially undervalued, with analysts projecting upside well above the current share price based on future growth expectations.

"Maplebear (Instacart) is positioned to benefit from the continued shift of grocery and essential goods shopping to digital channels and e-commerce, which remains underpenetrated in the grocery sector. This long-term trend expands Instacart's addressable market and is evidenced by strong GTV/order growth, accelerating retention, and increasing Instacart+ penetration. These factors are likely to drive future increases in top-line revenue."

Curious about what really drives this bold valuation call? There is a surprising combination of faster digital adoption, clever technology upgrades, and aggressive financial projections that make this fair value number stand out. Want to know which moving parts are fueling such optimism, and what analysts believe Maplebear must achieve to justify this premium?

Result: Fair Value of $59.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising labor costs and stronger competition could slow Instacart’s momentum. These factors pose real challenges to the optimistic growth scenario analysts predict.

Find out about the key risks to this Maplebear narrative.Another View: What Do Earnings Ratios Say?

While the fair value model points to strong upside, another common approach is looking at the company's current earnings ratio versus the industry average. This comparison suggests Maplebear is not as cheap as the first method implies. Which view tells the real story?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding Maplebear to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Maplebear Narrative

If you want to dig into the details yourself or see things from a different angle, it’s easy to build your own perspective in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Maplebear.

Looking for More Investment Ideas?

Don’t wait for the next big headline to make your move. Use these hand-picked stock ideas and put your capital to work where the action is.

- Uncover high-yield opportunities and boost your income by checking out companies offering dividend stocks with yields > 3% to shareholders.

- Spot trailblazers shaping tomorrow’s tech landscape by finding innovation leaders in the world of quantum computing stocks research and advancements.

- Capture hidden value by targeting equities trading below their intrinsic worth with our tool for undervalued stocks based on cash flows stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:CART

Maplebear

Maplebear Inc., doing business as Instacart, engages in the provision of online grocery shopping services to households in North America.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)