Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:TMHC

I Ran A Stock Scan For Earnings Growth And Taylor Morrison Home (NYSE:TMHC) Passed With Ease

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

In contrast to all that, I prefer to spend time on companies like Taylor Morrison Home (NYSE:TMHC), which has not only revenues, but also profits. Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

See our latest analysis for Taylor Morrison Home

How Fast Is Taylor Morrison Home Growing?

As one of my mentors once told me, share price follows earnings per share (EPS). It's no surprise, then, that I like to invest in companies with EPS growth. Over the last three years, Taylor Morrison Home has grown EPS by 13% per year. That growth rate is fairly good, assuming the company can keep it up.

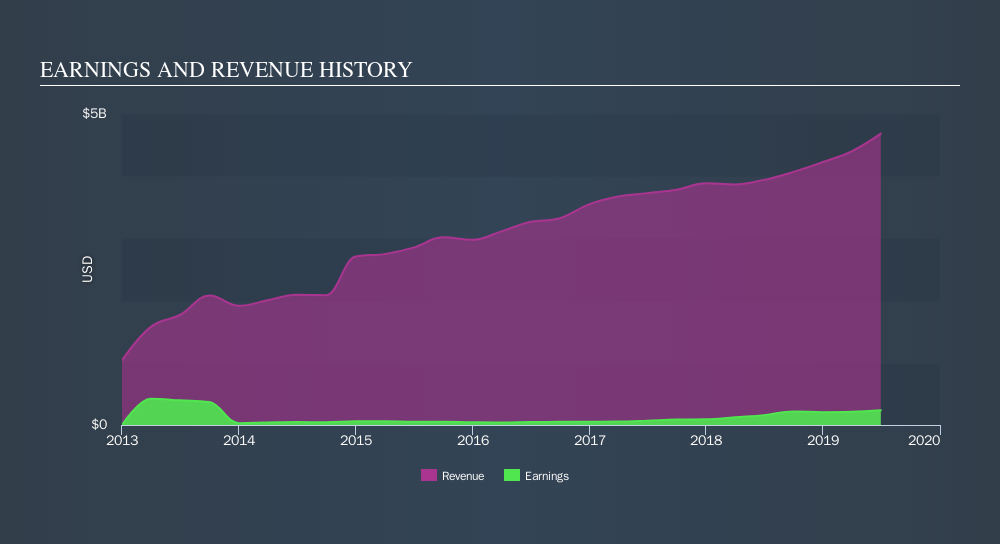

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. While we note Taylor Morrison Home's EBIT margins were flat over the last year, revenue grew by a solid 19% to US$4.7b. That's a real positive.

In the chart below, you can see how the company has grown earnings, and revenue, over time.

Fortunately, we've got access to analyst forecasts of Taylor Morrison Home's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Taylor Morrison Home Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. So it is good to see that Taylor Morrison Home insiders have a significant amount of capital invested in the stock. To be specific, they have US$13m worth of shares. That's a lot of money, and no small incentive to work hard. Despite being just 0.4% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Is Taylor Morrison Home Worth Keeping An Eye On?

One positive for Taylor Morrison Home is that it is growing EPS. That's nice to see. Just as polish makes silverware pop, the high level of insider ownership enhances my enthusiasm for this growth. That combination appeals to me, for one. So yes, I do think the stock is worth keeping an eye on. Once you've identified a business you like, the next step is to consider what you think it's worth. And right now is your chance to view our exclusive discounted cashflow valuation of Taylor Morrison Home. You might benefit from giving it a glance today.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:TMHC

Taylor Morrison Home

Operates as a land developer and homebuilder in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor