Advertisement

- United States

- /

- Leisure

- /

- NYSE:PII

Will Polaris' (PII) 2026 Off Road Lineup Refresh Strengthen Its Competitive Edge in Key Markets?

Simply Wall St

Reviewed by Sasha Jovanovic

- In October 2025, Polaris Off Road unveiled a second wave of 2026 vehicle enhancements, including a dramatic RZR XP redesign, the all-new 72" wide RZR XP S, special editions like the RZR PRO S Calavera, and new RANGER XD 1500 NorthStar versions tailored for specific markets.

- This latest wave of innovation underscores Polaris' active focus on customer-driven engineering and its celebration of significant milestones in key international markets.

- We'll now explore how Polaris' expanded 2026 lineup and high-profile RZR XP redesign could influence its future investment case.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

Polaris Investment Narrative Recap

For Polaris shareholders, the core investment belief often centers on the company's resilience in the face of external challenges, balancing innovation in its product portfolio with ongoing margin pressures from significant tariff costs and economic headwinds. The unveiling of the advanced 2026 RZR and RANGER models is a signal of product momentum, yet this news does not materially shift the current catalyst: managing through a period of depressed retail sales as consumers remain cautious and tariffs weigh on earnings, with margin compression as the primary risk.

Among recent updates, Polaris' introduction of feature-rich models like the redesigned RZR XP and RZR XP S directly aligns with its ongoing strategy to use new launches to bolster retail interest and average selling prices. While these launches have the potential to influence demand, their immediate impact is balanced against broader market forces and uncertain consumer appetite for higher-ticket items in the current climate.

Yet, before considering a position, investors should not overlook that, despite new product advances, uncertainty around gross tariff costs of US$320 million to US$370 million could still...

Read the full narrative on Polaris (it's free!)

Polaris' outlook anticipates $7.5 billion in revenue and $224.6 million in earnings by 2028. This is based on annual revenue growth of 2.4% and an increase in earnings of $332.4 million from the current level of -$107.8 million.

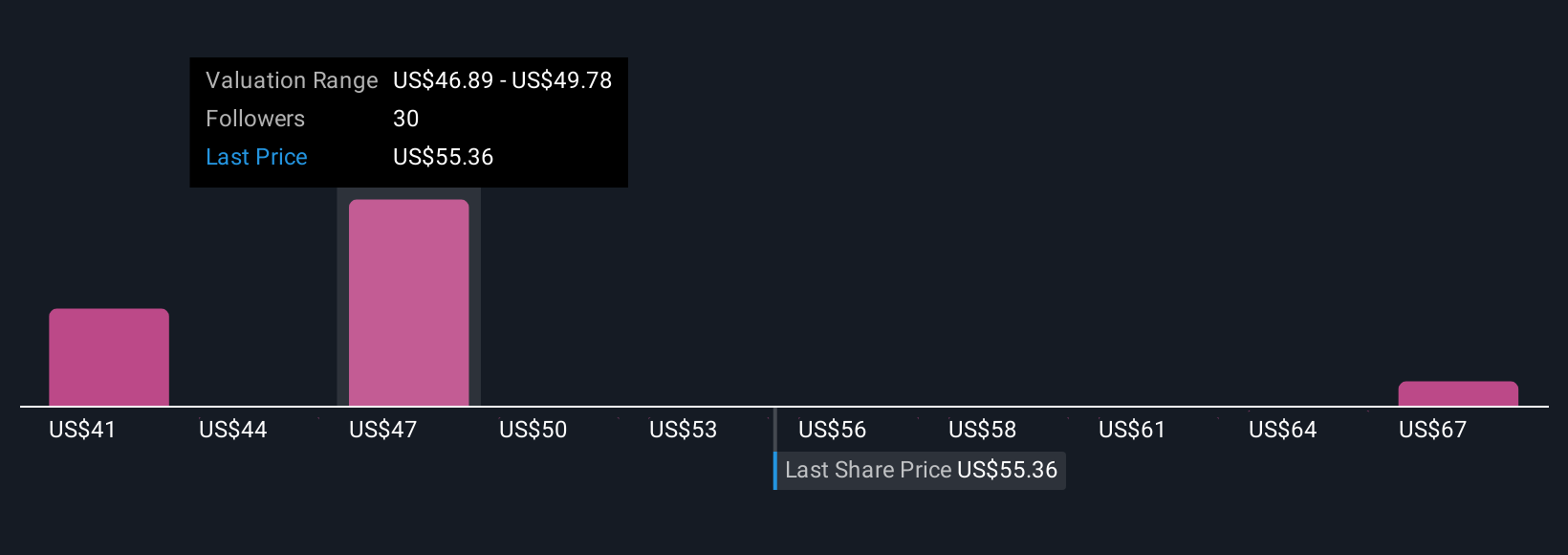

Uncover how Polaris' forecasts yield a $56.73 fair value, a 15% downside to its current price.

Exploring Other Perspectives

The Simply Wall St Community included 5 unique fair value estimates for Polaris, ranging from US$47.31 to US$70 per share. While opinions differ on upside potential, many focus on how persistent margin pressures tied to tariffs could continue to sway future results, inviting a variety of perspectives on what Polaris’ next chapter holds.

Explore 5 other fair value estimates on Polaris - why the stock might be worth as much as 5% more than the current price!

Build Your Own Polaris Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PII

Polaris

Designs, engineers, manufactures, and markets powersports vehicles in the United States, Canada, and internationally.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

26 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1161.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8685.8% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative