- United States

- /

- Consumer Durables

- /

- NasdaqGM:LOVE

Why Investors Shouldn't Be Surprised By The Lovesac Company's (NASDAQ:LOVE) 38% Share Price Surge

The The Lovesac Company (NASDAQ:LOVE) share price has done very well over the last month, posting an excellent gain of 38%. Looking back a bit further, it's encouraging to see the stock is up 42% in the last year.

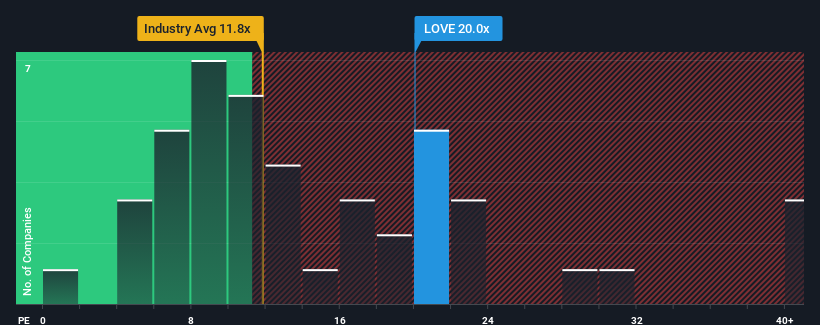

Since its price has surged higher, given around half the companies in the United States have price-to-earnings ratios (or "P/E's") below 16x, you may consider Lovesac as a stock to potentially avoid with its 20x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Lovesac has been very sluggish. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Lovesac

Is There Enough Growth For Lovesac?

There's an inherent assumption that a company should outperform the market for P/E ratios like Lovesac's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 37% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the five analysts covering the company suggest earnings should grow by 45% each year over the next three years. With the market only predicted to deliver 12% per annum, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Lovesac's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Lovesac's P/E

Lovesac shares have received a push in the right direction, but its P/E is elevated too. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Lovesac's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 2 warning signs for Lovesac that you need to take into consideration.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:LOVE

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives