- United States

- /

- Luxury

- /

- OTCPK:EVKG

Shareholders Will Probably Be Cautious Of Increasing Ever-Glory International Group, Inc.'s (NASDAQ:EVK) CEO Compensation At The Moment

The underwhelming performance at Ever-Glory International Group, Inc. (NASDAQ:EVK) recently has probably not pleased shareholders. The next AGM coming up on 10 December 2021 will be a chance for shareholders to have their concerns addressed by the board, challenge management on company strategy and vote on resolutions such as executive remuneration, which may help change the company's future prospects. The data we gathered below shows that CEO compensation looks acceptable for now.

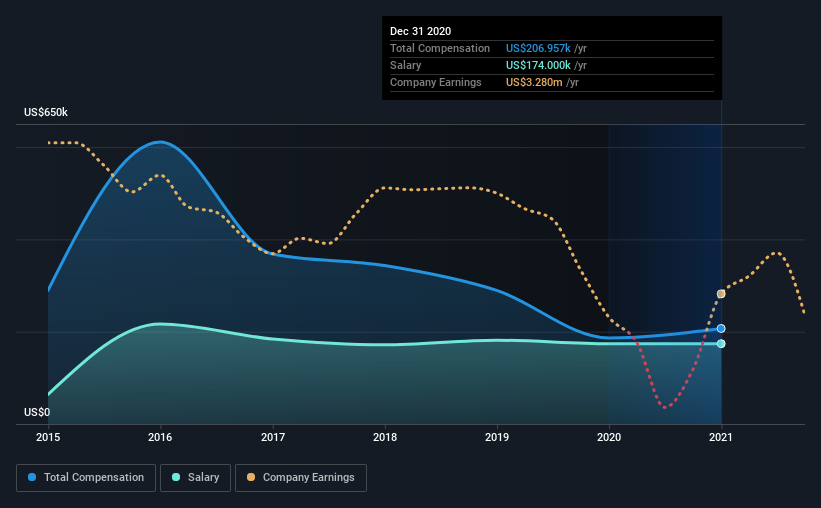

See our latest analysis for Ever-Glory International Group

Comparing Ever-Glory International Group, Inc.'s CEO Compensation With the industry

At the time of writing, our data shows that Ever-Glory International Group, Inc. has a market capitalization of US$37m, and reported total annual CEO compensation of US$207k for the year to December 2020. We note that's an increase of 11% above last year. In particular, the salary of US$174.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below US$200m, we found that the median total CEO compensation was US$463k. This suggests that Edward Kang is paid below the industry median. Moreover, Edward Kang also holds US$12m worth of Ever-Glory International Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$174k | US$174k | 84% |

| Other | US$33k | US$13k | 16% |

| Total Compensation | US$207k | US$187k | 100% |

On an industry level, around 23% of total compensation represents salary and 77% is other remuneration. Ever-Glory International Group is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Ever-Glory International Group, Inc.'s Growth Numbers

Over the last three years, Ever-Glory International Group, Inc. has shrunk its earnings per share by 52% per year. It achieved revenue growth of 4.1% over the last year.

Few shareholders would be pleased to read that EPS have declined. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Ever-Glory International Group, Inc. Been A Good Investment?

The return of -40% over three years would not have pleased Ever-Glory International Group, Inc. shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 4 warning signs for Ever-Glory International Group you should be aware of, and 1 of them is a bit concerning.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Ever-Glory International Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:EVKG

Ever-Glory International Group

Manufactures, supplies, and retails apparel in Mainland China, Hong Kong, Germany, the United Kingdom, Europe, Japan, and the United States.

Low with weak fundamentals.