Advertisement

- United States

- /

- Consumer Durables

- /

- NasdaqGS:CRCT

Cricut (CRCT): Is the Stock’s Current Valuation Justified After Recent Declines?

Simply Wall St

Reviewed by Kshitija Bhandaru

Cricut (CRCT) stock has been on investors’ radar lately as its shares edged up slightly over the past week, despite a dip of 21% over the past month. This price movement has some market watchers examining its recent trends and valuation.

See our latest analysis for Cricut.

While Cricut’s 1-year total shareholder return sits at -11.1% and its share price is down more than 20% in the past month, these moves fit a broader trend as momentum has faded after a stronger start to the year. The most recent price swings may reflect investor uncertainty around the company’s valuation and future growth story.

If you’re tracking shifts in this space and want to expand your search, it could be the perfect time to discover fast growing stocks with high insider ownership.

With shares lagging and valuation metrics flashing mixed signals, investors are left wondering: is Cricut trading at a discount after recent declines, or is the market already factoring in muted growth prospects ahead?

Price-to-Earnings of 15.4x: Is it justified?

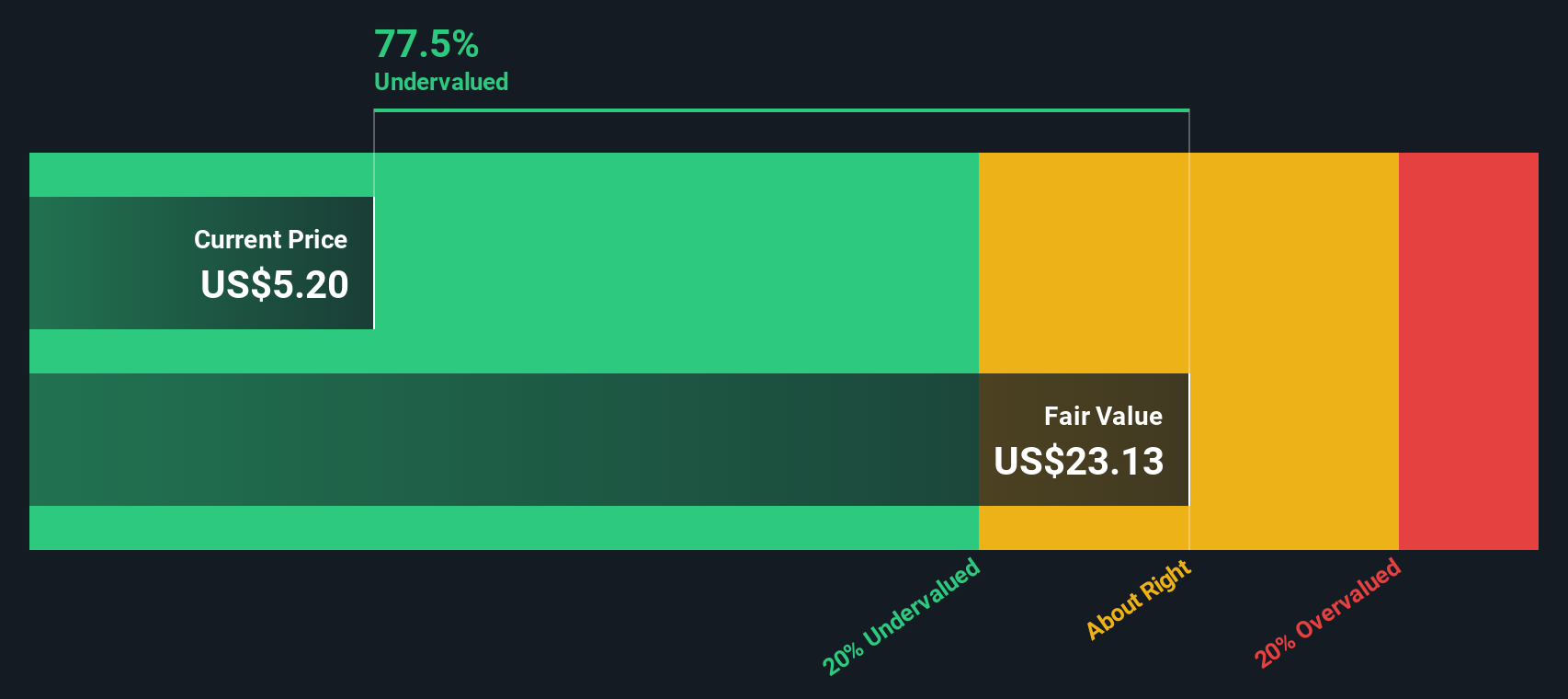

Cricut shares are trading on a price-to-earnings (P/E) ratio of 15.4x, putting the stock well above the Consumer Durables industry average. At a last close price of $5.22, this multiple raises the question of whether the market is too optimistic about the company’s near-term profit outlook.

The P/E ratio indicates how much investors are willing to pay for each dollar of the company’s earnings, and it is a popular way to benchmark valuation across consumer-focused businesses with stable earnings histories.

While the P/E is a useful shorthand, in Cricut’s case it may suggest the market is pricing in more positive momentum than recent financial trends support. A 15.4x ratio is noticeably higher than the US Consumer Durables industry average of 10.2x and above the typical peer at 12x. This suggests Cricut’s shares offer less value relative to expected earnings.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 15.4x (OVERVALUED)

However, weak revenue growth and a 22% discount to analyst price targets are risks that could challenge the argument for an overvalued stock.

Find out about the key risks to this Cricut narrative.

Another View: Discounted Cash Flow Perspective

While the price-to-earnings ratio suggests Cricut may be overvalued, our DCF model presents a different perspective. According to this approach, the stock is trading at a significant 77.5% discount compared to what we estimate as its fair value. Could the market be overlooking Cricut’s long-term potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cricut for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Cricut Narrative

Keep in mind that if you see things differently or want to investigate for yourself, you can quickly build your own view in just a few minutes with Do it your way.

A great starting point for your Cricut research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let opportunity pass you by. Take charge of your financial goals and broaden your watchlist with some of the market’s most exciting stock themes.

- Fuel your portfolio with growth potential by checking out these 878 undervalued stocks based on cash flows that stand out for compelling valuations and future upside.

- Capitalize on big trends in artificial intelligence by reviewing these 24 AI penny stocks showing strong momentum in next-generation tech.

- Unlock steady income streams by exploring these 18 dividend stocks with yields > 3% offering attractive yields and the potential for reliable returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRCT

Cricut

Engages in the design, marketing, and distribution of a creativity platform that enables users to turn ideas into professional-looking handmade goods in the United States, Canada, the United Kingdom, Ireland, Australia, New Zealand, Western Europe, the Middle East, Latin America, South Africa, and Asia.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets