Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:WM

Does Waste Management’s Long Run Still Leave Upside After Recent Recycling Investments?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Waste Management is still worth buying after its long run up, or if the trash giant is finally looking a bit pricey? Let us unpack what the current share price is really implying about its future cash flows.

- Despite a modest 0.8% dip over the past week, the stock is up 7.4% over the last month and 7.0% year to date, building on a hefty 35.3% gain over three years and 98.0% over five years, even though the last 12 months have seen a 3.3% pullback.

- Recently, the market has focused on Waste Management's ongoing investments in recycling and renewable natural gas projects, plus its steady contract wins with municipalities looking for stable long term waste and environmental services partners. These developments have reinforced its reputation as a defensive, cash generative business, even as investors debate how much future growth is already priced in.

- On our valuation checks, Waste Management scores a 3/6 value score. This suggests the stock looks reasonably priced on some metrics but not a screaming bargain on others. We will walk through those different valuation lenses next, while hinting at a deeper way of thinking about fair value that we will come back to at the end.

Approach 1: Waste Management Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a company is worth today by projecting the cash it can generate in the future and discounting those cash flows back to the present.

For Waste Management, the latest twelve month free cash flow is about $2.4 Billion. Analysts and extrapolations by Simply Wall St expect this to rise steadily, with projected free cash flow of roughly $5.3 Billion by 2035 in the second stage of a two stage Free Cash Flow to Equity model. These projections blend explicit analyst estimates for the next few years with gradually slowing growth assumptions further out.

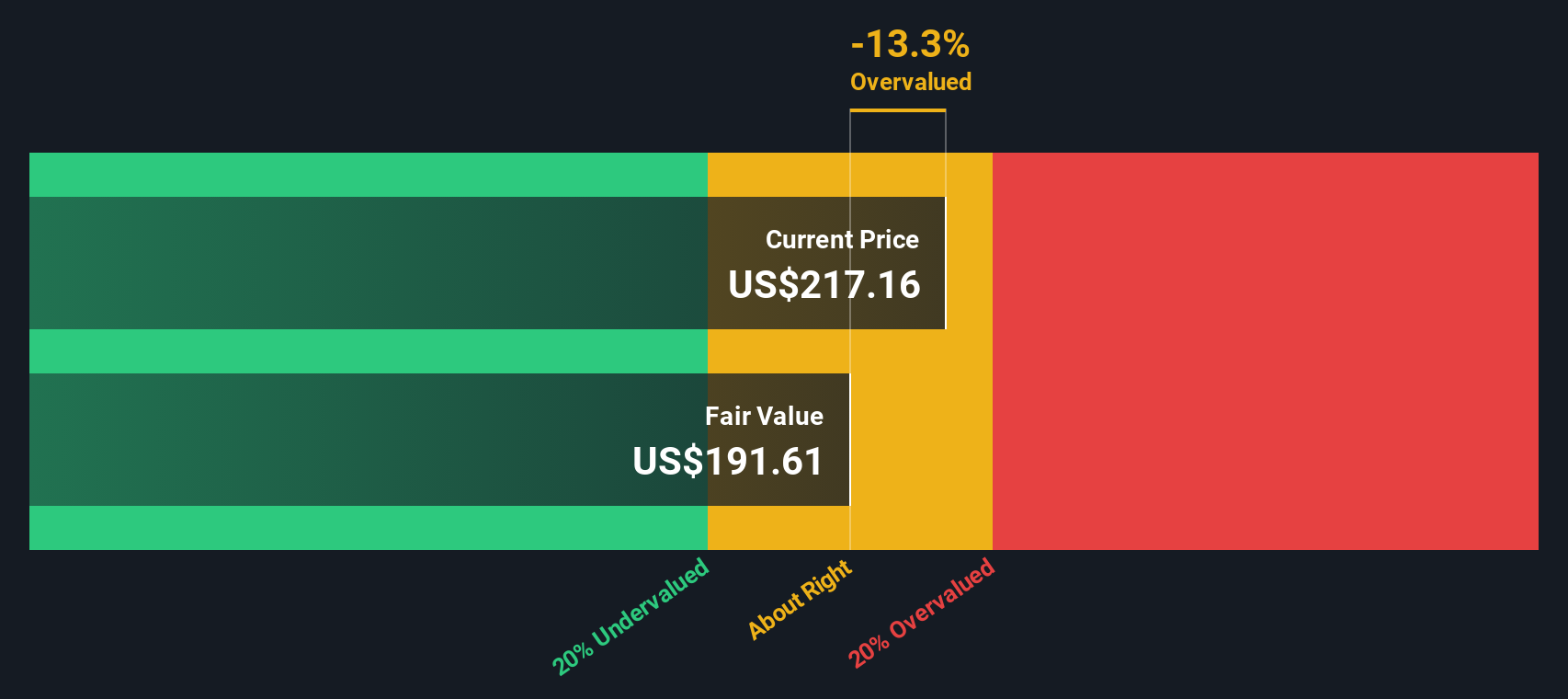

When all those future cash flows are discounted back, the model arrives at an intrinsic value of about $239.37 per share. Compared to the current share price, this implies the stock is around 10.4% undervalued, suggesting a modest margin of safety rather than a deep value opportunity.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Waste Management is undervalued by 10.4%. Track this in your watchlist or portfolio, or discover 935 more undervalued stocks based on cash flows.

Approach 2: Waste Management Price vs Earnings

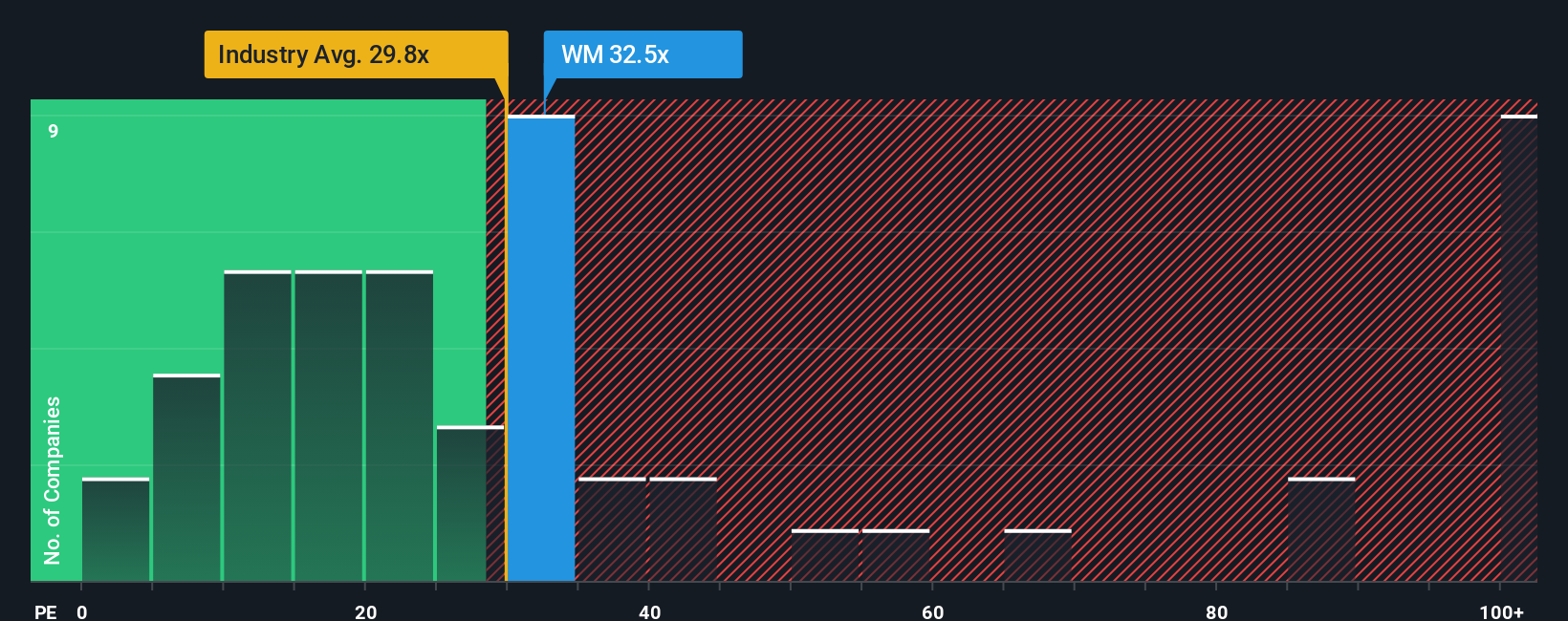

For a mature, consistently profitable business like Waste Management, the Price to Earnings (PE) ratio is a useful yardstick because it directly links what investors pay today to the profits the company is generating right now.

In general, faster growing and lower risk companies can justify a higher PE, while slower growth or higher uncertainty usually warrant a lower, more conservative multiple. That context matters because Waste Management currently trades on a PE of about 33.7x, which is well above the Commercial Services industry average of roughly 22.8x, but below the 46.8x average of its larger, more closely comparable peers.

Simply Wall St also calculates a proprietary Fair Ratio for the PE, which blends in Waste Management’s earnings growth outlook, profitability, industry, market cap and company specific risks. This Fair Ratio, around 35.4x, is designed to be more tailored than blunt comparisons to peers or the sector because it adjusts for the quality and durability of the earnings being valued. With the current PE of 33.7x sitting a little below that Fair Ratio, the shares appear slightly undervalued on this metric, rather than stretched.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Waste Management Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Waste Management’s future with the numbers by writing a short story that sits behind your assumptions for revenue, earnings, margins and fair value. You can then link that story to a forecast and finally to a fair value you can compare directly with today’s price to decide whether to buy, hold or sell.

On Simply Wall St’s Community page, millions of investors can easily build and share these Narratives. They update dynamically when new earnings, guidance or news arrives, so your fair value view evolves with the facts. You can quickly see how a bullish Narrative that expects WM’s technology, automation and renewable projects to deliver strong margin gains and justifies a fair value closer to the optimistic $277 target compares to a more cautious Narrative that focuses on revenue volatility, regulatory risk and integration challenges and lands nearer the $198 low end of analyst estimates.

Do you think there's more to the story for Waste Management? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Waste Management might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WM

Waste Management

Through its subsidiaries, provides environmental solutions to residential, commercial, industrial, and municipal customers in the United States, Canada, Western Europe, and internationally.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

9 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9238.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative