Steelcase (SCS) shares have shown some interesting trends over the past several months, with the stock up more than 54% in the past 3 months. This performance draws attention to what is driving recent momentum.

While Steelcase’s impressive 54% share price return over the past three months has stolen the spotlight, momentum has really taken shape against a much bigger backdrop. The one-year total shareholder return stands at a robust 30%. What is truly remarkable is the three-year total return of 166%, indicating that long-term investors have been rewarded as the company’s prospects and risk profile have shifted for the better recently.

If Steelcase’s recent surge made you wonder what other opportunities are out there, now is a great time to broaden your investing universe and discover fast growing stocks with high insider ownership

But after such strong gains in a short span, is there still value left in Steelcase shares? Or is the recent rally simply reflecting expectations for continued growth? Could this be a buying opportunity, or is everything already priced in?

Advertisement

Most Popular Narrative: 4.4% Overvalued

According to the most prominent narrative from codabat, Steelcase’s current share price of $16.29 sits slightly above the narrative’s calculated intrinsic fair value of $15.60. This sets the stage for exploring whether current market optimism might be overextended, or if a different story is being told beneath the surface.

Based on sector-relative P/E analysis, Steelcase appears moderately undervalued. Using TTM EPS of $1.04 and applying the furniture industry average P/E multiple of 15x, the intrinsic fair value equals $15.60 per share. Key Assumptions: Normalized P/E: 15x (furniture industry median). EPS sustainability: Current $1.04 TTM earnings maintainable. Sector convergence: SCS multiple should align with furniture peers. Cyclical recovery: Office furniture demand stabilization expected.

Curious which critical financial levers and cyclical assumptions are behind this number? There is a unique mix of industry alignment and financial consistency driving the narrative’s fair value. The full analysis reveals which business forces shape that number and how a sector-wide rebound could tip the balance. Do not miss the main quantitative trigger that could spark a major price move from here.

However, sustained margin pressure or a slow office real estate recovery could quickly challenge this fair value narrative and shift market sentiment on Steelcase’s prospects.

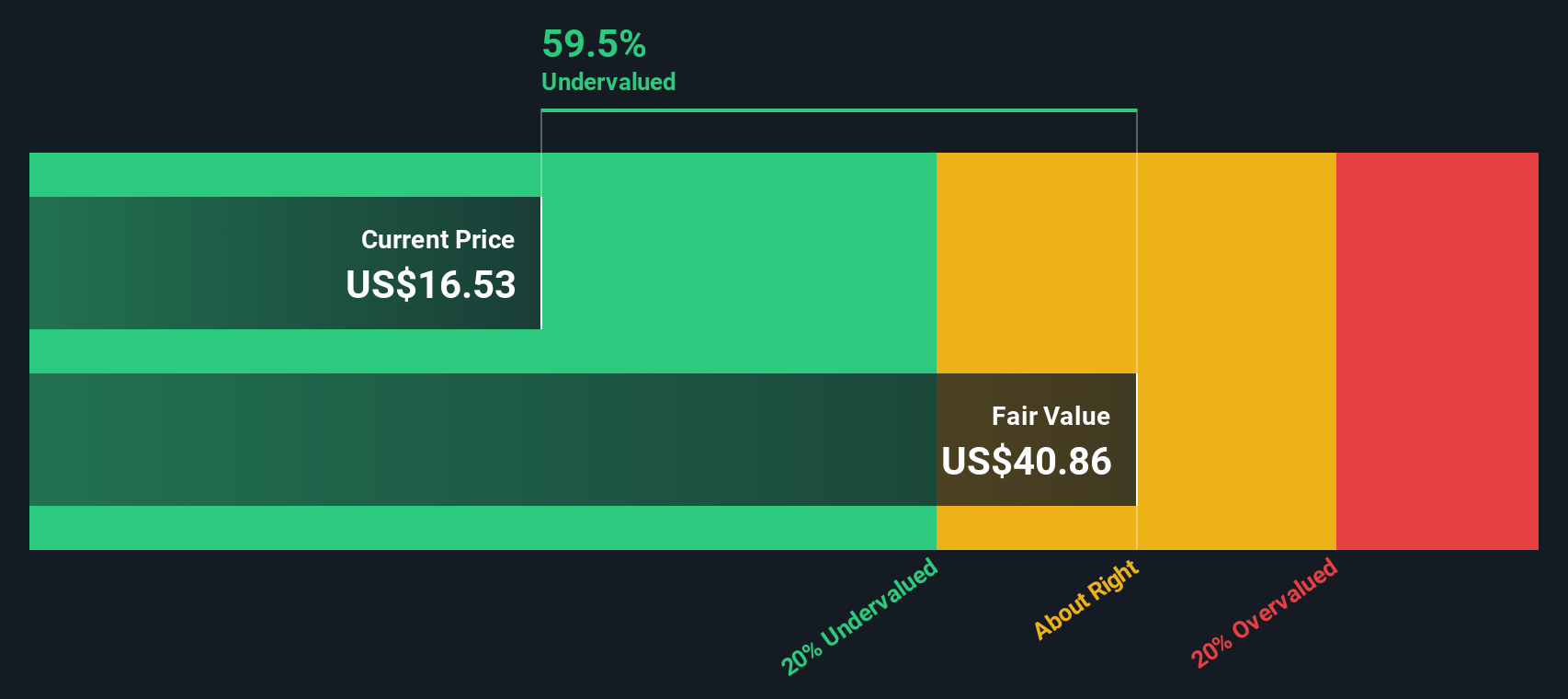

Taking a different approach, our DCF model suggests Steelcase shares are dramatically undervalued, trading more than 60% below its estimated fair value of $40.80. This signals a potentially significant upside; however, does such a wide gap signal opportunity, or is the market pricing in hidden risks?

If you see things differently or would rather dig into the numbers yourself, you can develop your own narrative perspective in just a few minutes. Do it your way

Strengthen your portfolio by exploring unique opportunities beyond Steelcase. Don’t miss the chance to get ahead with smart stock picks tailored for tomorrow’s trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks