Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:ROL

How Rollins’ (ROL) Revenue Growth and Cash Flow Strength May Shape Its Long-Term Investment Appeal

Simply Wall St

Reviewed by Sasha Jovanovic

- Recent investment analyses have highlighted Rollins' robust performance, noting an 11.5% annual revenue increase over the past two years and a strong free cash flow margin of 16.4%.

- This financial resilience and capital return capability set Rollins apart from peers facing sector headwinds, underlining its appeal among stability-focused investors.

- We'll now explore how the spotlight on Rollins' revenue growth and free cash flow may influence its long-term investment outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Rollins Investment Narrative Recap

To consider owning Rollins shares, an investor has to believe in the company's steady revenue growth, strong free cash flow, and its ability to maintain resilience even as sector peers struggle. The latest news does not materially shift the most important catalyst, ongoing growth in recurring commercial revenue, nor does it change the primary risk from macroeconomic swings, which could dampen demand in residential segments. Among recent developments, Rollins’ consistent dividend payments stand out, including a 10% increase declared earlier this year. This supports the view that capital returns remain a central part of the investment case, complementing ongoing organic and acquisition-driven growth as the key catalysts for the business. But contrasting its consistently growing revenues, investors should be aware that Rollins’ profitability still faces pressure when...

Read the full narrative on Rollins (it's free!)

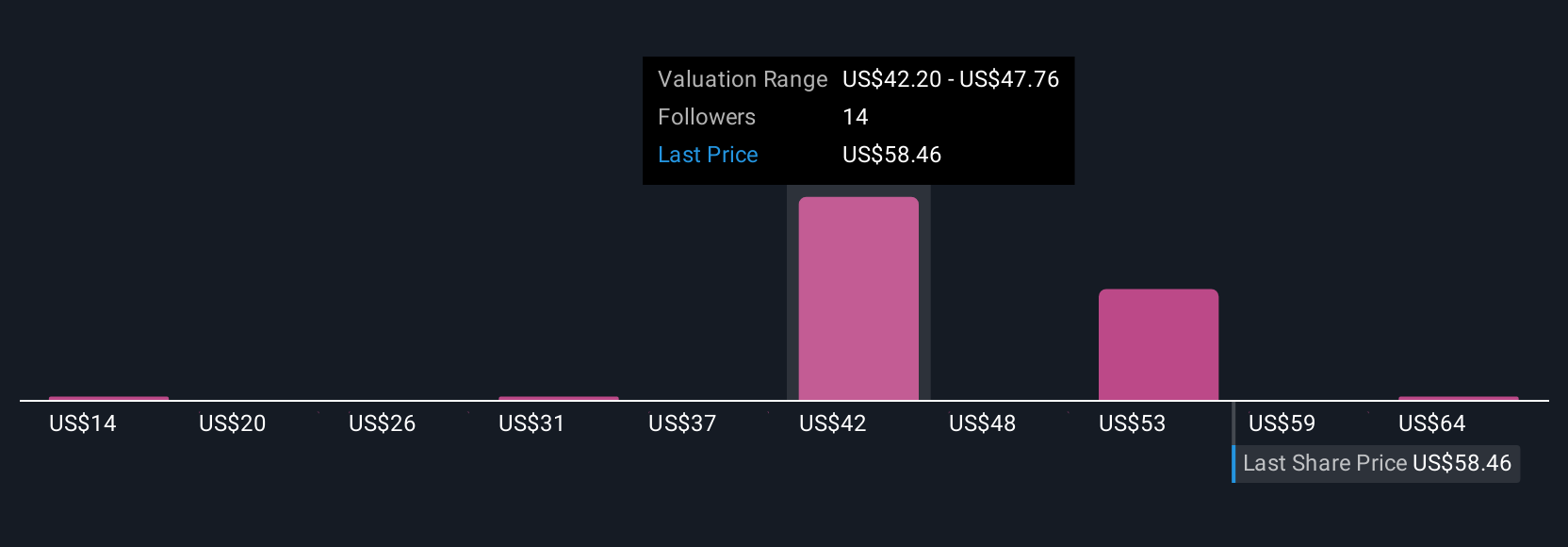

Rollins' narrative projects $4.6 billion in revenue and $686.0 million in earnings by 2028. This requires 8.8% yearly revenue growth and a $196.7 million earnings increase from $489.3 million today.

Uncover how Rollins' forecasts yield a $59.67 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community provided fair value estimates for Rollins, ranging widely from US$14.40 to US$72.00 per share. While many see upside in recurring revenue catalysts, there is ongoing debate about how external risks could shape the company’s growth ahead, consider reviewing several viewpoints to deepen your understanding.

Explore 4 other fair value estimates on Rollins - why the stock might be worth as much as 28% more than the current price!

Build Your Own Rollins Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Rollins research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Rollins research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rollins' overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ROL

Rollins

Through its subsidiaries, provides pest and wildlife control services to residential and commercial customers in the United States and internationally.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor