Advertisement

- United States

- /

- Professional Services

- /

- NYSE:PSN

A Fresh Look at Parsons (PSN) Valuation After Major Hudson Tunnel Project Contract Win

Simply Wall St

Reviewed by Kshitija Bhandaru

Parsons (NYSE:PSN) is in the spotlight after its joint venture was awarded a $665 million, 4.5-year contract extension to help manage the ongoing Hudson Tunnel Project. This contract highlights the company’s expanding role in major infrastructure development along with its rising financial performance.

See our latest analysis for Parsons.

The Hudson Tunnel Project win is just the latest sign of momentum for Parsons. After a strong stretch of news and consistently rising earnings, the company’s share price has jumped 16% in the past month and nearly 16% over the last quarter, in stark contrast to its -3% year-to-date share price return. While the one-year total shareholder return stands at -18%, Parsons’ three-year figure shines at 110%. This points to longer-term value for investors who have remained with the story as growth drivers accumulate.

If this run of infrastructure deals has you curious about other high-potential companies, now is a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares surging on impressive contract wins and solid earnings, some might wonder if Parsons remains undervalued by the market or if its current price already reflects all the optimism about future growth.

Most Popular Narrative: Fairly Valued

With Parsons’ last close price nearly identical to its consensus analyst fair value, the stock is currently seen as neither significantly under- nor overvalued. This balanced stance follows a sustained rally and suggests the next big shift could rely on fresh growth drivers or changes in market sentiment.

Parsons is poised to benefit from ongoing multi-year increases in global and U.S. infrastructure investment, particularly in hard infrastructure such as roads, bridges, airports, and transit. This trend is driven by bipartisan government support and major legislation (IIJA, Surface Transportation Reauthorization), with revenue visibility and growth supported by an $8.9 billion backlog and substantial unbooked pipeline. This positions revenue to accelerate through at least 2028 and beyond.

What’s the secret sauce behind this “just right” fair value? Throughout the narrative, bold assumptions about segment growth, global expansion, and rising project backlogs shape this valuation. Want the full story? The details may surprise you.

Result: Fair Value of $86.67 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifts in U.S. government funding or sharp competition for major contracts could quickly unsettle Parsons’ growth trajectory and investor expectations.

Find out about the key risks to this Parsons narrative.

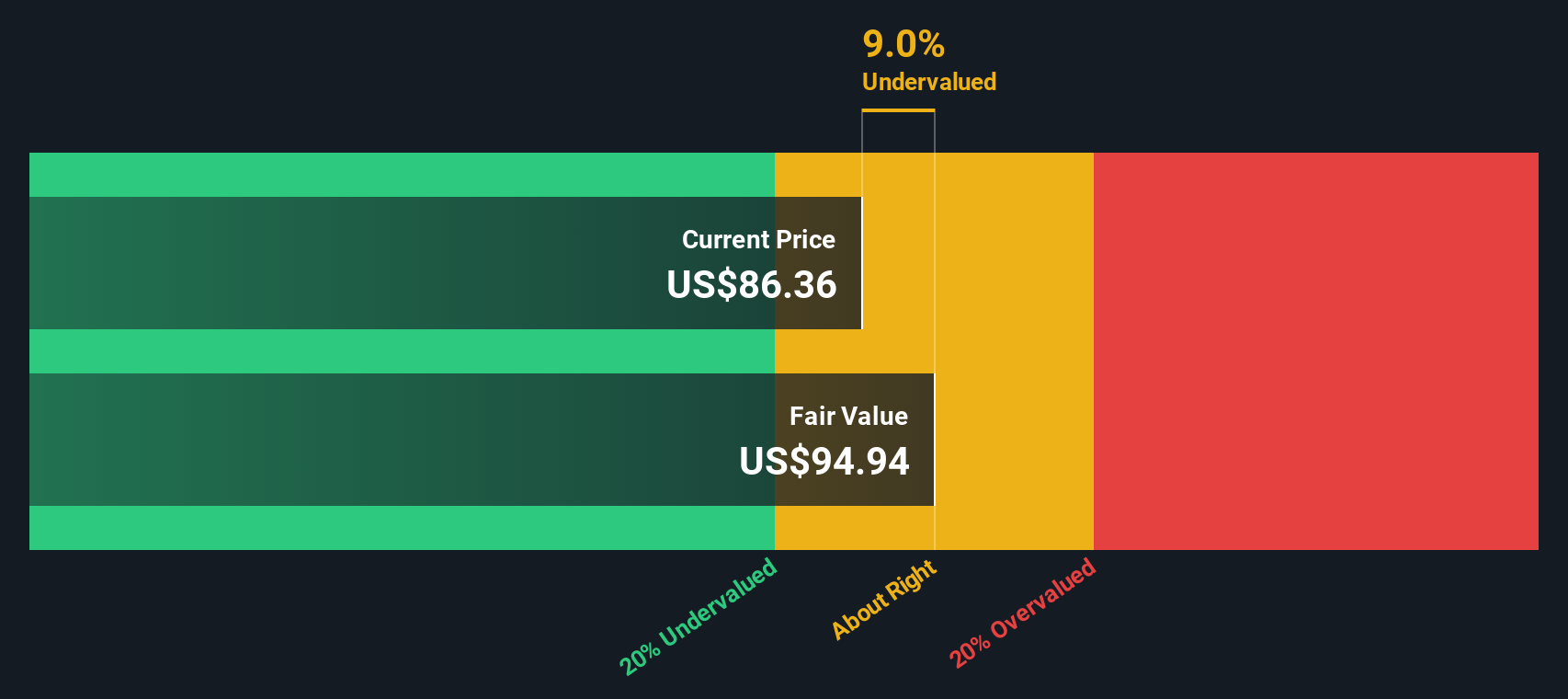

Another View: Discounted Cash Flow Perspective

Looking through the lens of our DCF model, Parsons appears undervalued. The DCF estimate of fair value sits at $94.97, which is higher than its current share price of $87.77. This suggests there could be some overlooked upside for investors. However, is the market missing something, or is caution warranted?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Parsons for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Parsons Narrative

If you see things differently or want to dig into the numbers yourself, you can build your own Parsons narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Parsons.

Looking for more investment ideas?

Don’t let the next big opportunity pass you by. Use the Simply Wall Street Screener to find stocks that fit your goals before the market catches on.

- Target smart value plays by checking out these 898 undervalued stocks based on cash flows. These may offer strong upside based on robust cash flows and solid fundamentals.

- Boost your passive income strategy by evaluating these 19 dividend stocks with yields > 3%, which features consistent yields above 3% and stable performance histories.

- Ride the AI wave and see which companies are positioned to benefit from rapid advances with these 25 AI penny stocks leading this fast-moving sector.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PSN

Parsons

Provides integrated solutions and services in the defense, intelligence, and critical infrastructure markets in North America, the Middle East, and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor