Advertisement

- United States

- /

- Professional Services

- /

- NYSE:PAYC

Is Paycom Software Attractive After 20% Decline Amid Platform Strategy Shift?

Reviewed by Bailey Pemberton

- Wondering if Paycom Software is a hidden bargain or a value trap? You are not alone, especially with so much happening in the tech sector recently.

- The stock is down 8.2% over the last 30 days and 20.0% over the past year, which hints at shifting sentiment and could open up fresh opportunities for savvy investors.

- Industry chatter has been lively after analysts weighed in on the company's evolving strategy, with several commentators noting increased competition and the company's moves to enhance its platform. These headlines help explain some of the recent price volatility and are worth keeping in mind as we dig deeper.

- With Paycom's current value score at 6 out of 6 undervalued checks, it is clear the numbers are impressive, but numbers are only part of the story. Next, we will explore several classic ways to assess value, and at the end, we will reveal an even more powerful approach to understanding Paycom's true worth.

Find out why Paycom Software's -20.0% return over the last year is lagging behind its peers.

Approach 1: Paycom Software Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s dollars. This approach provides a present-day valuation based on those expectations. For Paycom Software, this method helps investors gauge what the business is fundamentally worth, independent of market moods or recent price swings.

Currently, Paycom generates $350 million in Free Cash Flow (FCF), with analysts projecting this to more than double over the coming years. In fact, FCF is expected to reach $813 million by 2029. The growth is projected to remain robust over the following years, with ten-year extrapolations suggesting FCF could climb to $1.27 billion by 2035. While analyst forecasts directly cover up to five years, further growth estimates are derived systematically from recent trends.

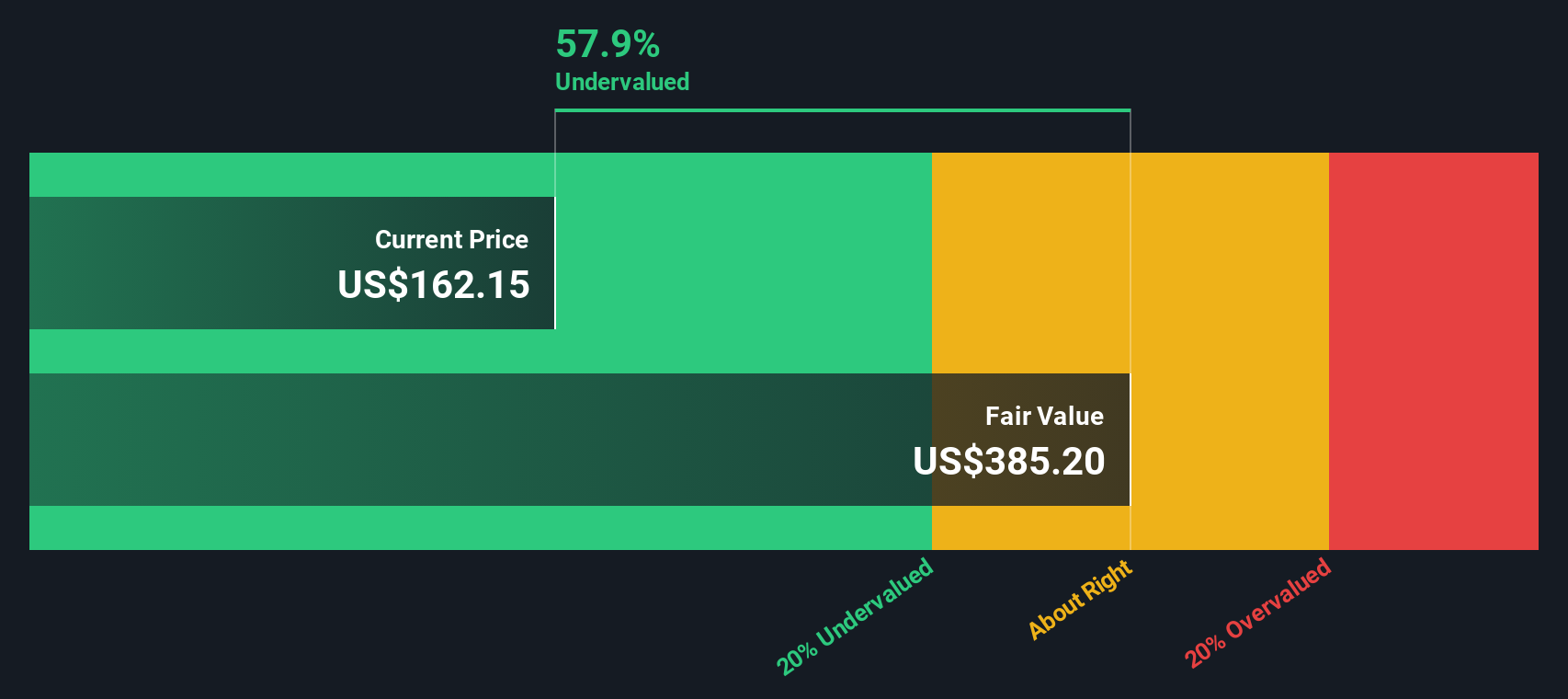

Based on these projections and using the 2 Stage Free Cash Flow to Equity model, the estimated intrinsic fair value of Paycom Software is $411.59 per share. With the DCF indicating the stock is trading at a 55.4% discount to this fair value, the model suggests Paycom Software is significantly undervalued relative to its underlying cash flow potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Paycom Software is undervalued by 55.4%. Track this in your watchlist or portfolio, or discover 836 more undervalued stocks based on cash flows.

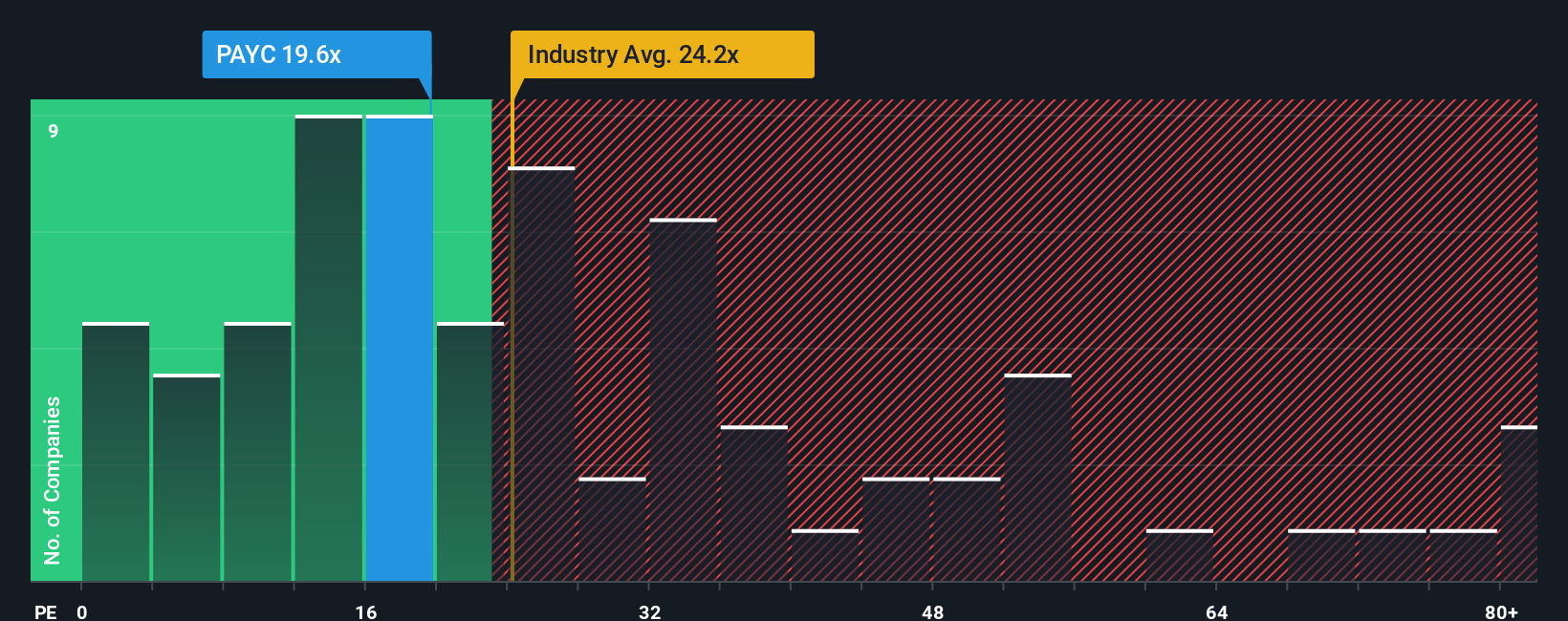

Approach 2: Paycom Software Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is widely recognized as a key valuation tool for profitable companies like Paycom Software. It expresses what investors are willing to pay today for a dollar of current earnings, making it particularly relevant for businesses with recurring profits. Factors like growth expectations and perceived risk play a big role in determining what a "normal" or "fair" PE should look like, since faster-growing or less risky companies tend to trade at higher multiples.

Paycom Software currently trades at a PE ratio of 24.9x. When we compare this to the Professional Services industry average of 25.1x and the average across its peer group at 26.9x, it appears the company’s valuation is in line with sector standards. However, these simple averages may not capture the nuances of Paycom's specific growth outlook, risk profile, margins, and market position.

This is where Simply Wall St’s Fair Ratio comes in. The Fair Ratio for Paycom Software is 25.2x, reflecting its growth prospects, profit margins, company size, industry positioning, and associated risk factors. Unlike broad industry or peer multiples, this proprietary benchmark aims to pinpoint a more tailored and meaningful valuation mark for the company.

Given that Paycom's current PE of 24.9x is effectively identical to its Fair Ratio of 25.2x, the stock appears to be fairly valued at present, with only a slight difference that is not statistically significant for investors.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1402 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Paycom Software Narrative

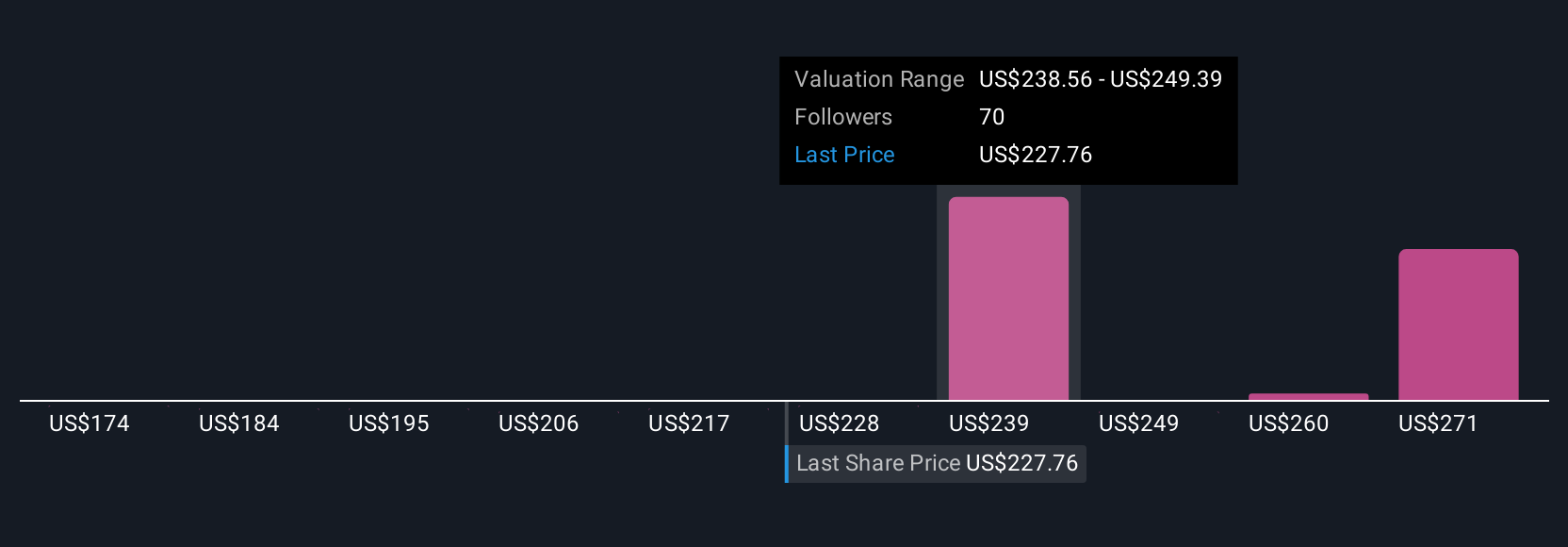

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story about a company, describing how you see its prospects, risks, and future. With Narratives, you tie together your perspective on a business with your own assumptions for revenue, earnings, margins, and ultimately, a fair value estimate. Narratives make investing practical and accessible to everyone by letting you turn the financial numbers into a cohesive story and see how it stacks up against the market price.

Available on Simply Wall St’s Community page and used by millions of investors, Narratives empower you to easily compare your fair value to the current stock price and decide whether to buy, sell, or hold. They update dynamically as new information, such as news, earnings, or guidance, emerges, keeping your decisions timely and relevant. For example, one Paycom Software Narrative might see the fair value as high as $260.61 per share based on accelerated growth, while another, more cautious view sets it at $208.00, reflecting heightened sector risks. Narratives help you invest with clarity by making your unique assumptions visible and actionable in real time.

Do you think there's more to the story for Paycom Software? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PAYC

Paycom Software

Provides cloud-based human capital management (HCM) solution delivered as software-as-a-service for small to mid-sized companies in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.3% undervalued

206 followersusers have followed this narrative

1 commentusers have commented on this narrative

29 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

51 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.2% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k36.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Hektar Real Estate Investment Trust ·

Hektar REIT: Outlook is getting more interesting as retail stabilises and diversification starts to kick in

Fair Value:RM 0.4910.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Guanajuato Silver ·

A Case for Guanajuato Silver (TSXV:GSVR) to reach (low end) CAD$4 (high end) CAD$18 by 2031

Fair Value:CA$1896.6% undervalued

19 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9828.2% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.2% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.0k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative