It’s now been three weeks since the U.S. and Israel launched air strikes against Iran, plunging the Persian Gulf into crisis. The immediate impact on markets has been fairly predictable. But where we go from here is anything but predictable.

We aren’t going to pretend we know what happens next. But we can map out a few scenarios, and the potential impact on the global economy and markets. Some knock on effects are obvious, others less so, and some are counter-intuitive.

What Happened In Markets This Week

🤖 Meta’s AI agent mishap highlights rising data governance risks ( Storyboard18 )

• What happened: A Meta AI agent exposed sensitive company and user data to unauthorized employees for about two hours after posting flawed guidance on an internal forum. The incident, classified as a high-severity internal event, was triggered when another employee followed the agent’s instructions and unintentionally broadened data access.

• How it impacts investors: Agentic AI can all too easily expose sensitive data or create vulnerabilities for hackers to exploit. This is both regulatory and reputational risk for companies. Cybersecurity has been a growth industry for a long time, and that’s not going to change anytime soon.

• Next steps: Explore cybersecurity companies using the Cybersecurity screener.

💾 Micron’s earnings surge signals AI memory supercycle strength ( CNBC )

• What happened: Micron reported US$12.20 adjusted EPS and US$23.86 billion in revenue, both well above expectations, with revenue nearly tripling year over year. The company also issued strong guidance for the next quarter, citing continued supply shortages and robust AI-driven demand. However, the stock price fell after the company announced a $25 billion spending plan.

• How it impacts investors: The results reinforce that the AI hardware boom is still accelerating, benefiting memory makers while creating cost pressure for downstream tech companies. Investors may see continued divergence between chip suppliers and device manufacturers.

• Next steps: Have a look at the Micron Technology community page to read a range of narratives for the company.

🥇 Gold slump reveals shifting macro pressures despite geopolitical tension ( Yahoo Finance )

• What happened: Gold prices fell about 8% over the week, marking their worst decline in six years, as rising energy prices and a stronger US dollar dampened rate-cut expectations. The drop was driven by higher real yields and forced liquidations despite ongoing geopolitical conflict.

• How it impacts investors: The move highlights how macro forces like interest rates and liquidity can outweigh traditional safe-haven demand. The central bank buying catalyst is also looking less certain, now that policy makers may need to provide stability to the market.

• Next steps: Use the global gold stock screener to find shares that may be trading at a bargain.

🏦 Central banks pause as geopolitical risks reshape rate outlook ( Yahoo Finance )

• What happened: The US Federal Reserve and European Central Bank both held interest rates steady, citing uncertainty linked to the Iran conflict. Updated forecasts showed fewer expected rate cuts and higher inflation projections, alongside weaker growth expectations in Europe.

• How it impacts investors: Prolonged higher rates could weigh on rate-sensitive sectors like real estate and growth stocks, while supporting energy and defense industries. The shift also suggests a more volatile macro backdrop for global equities.

• Next steps : Use The Simply Wall St Markets Page to keep an eye on rate sensitive sectors.

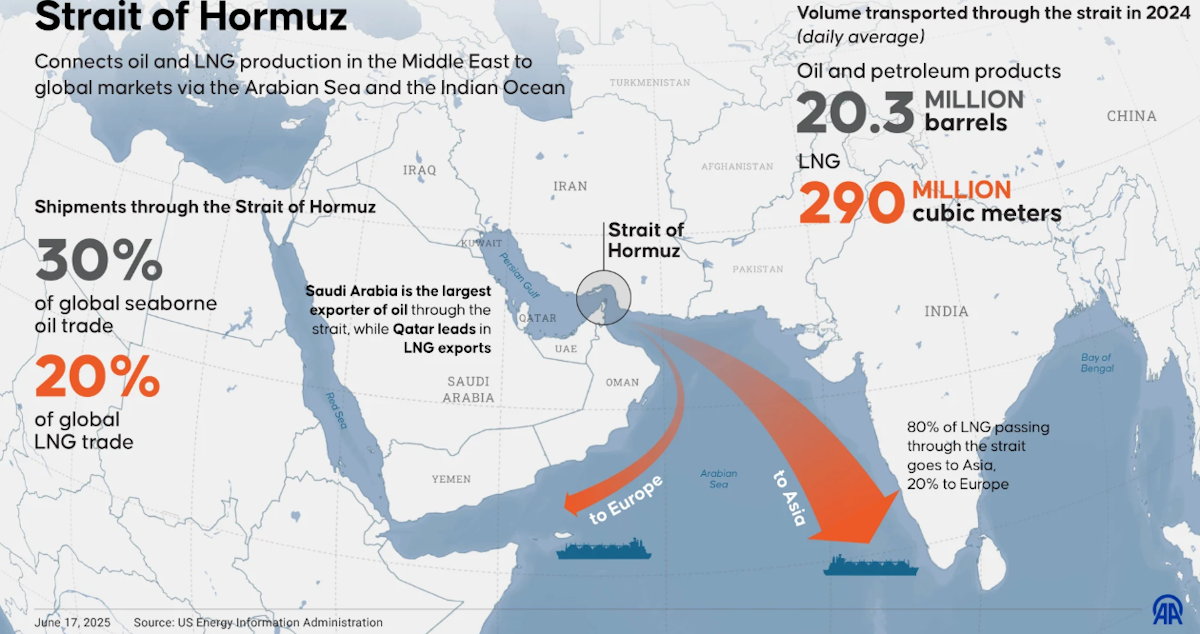

War in the Persian Gulf and its impact to investors

The immediate impact of the war has been higher energy prices and a sell-off of global equity and bond markets. In the months ahead we could see a de-escalation of some sort, or a drawn out war but with limited impact on energy production and shipping.

But it’s important to consider what’s at stake if shipping remains restricted or if production facilities are damaged.

The largest oil supply shock in history and why prices aren't higher

By most measures we have just witnessed the largest oil price shock in history.

The Strait of Hormuz was carrying roughly 20 million barrels per day before the conflict — about one-fifth of global oil consumption . That flow has been reduced to a trickle. Gulf production has been curtailed by at least 8 million barrels per day, with a further two million barrels of condensates and NGLs shut in.

At around $92, the oil price is up over 40% since the end of January, and it briefly traded as high as $120. Given the impact on oil shipments, and the potential impact on production, you might expect it to be a lot higher.

There are a few reasons for this:

- Global crude and product stocks stood at 8,210 million barrels in January, the highest since February 2021 .

- On March 11, the IEA coordinated the largest emergency reserve release in its history: 400 million barrels.

- The IEA has also cut its 2026 demand growth forecast by 210 thousand barrels per day due to flight cancellations and LPG disruptions. Paradoxically, war-driven demand destruction is helping cap prices at the same time as supply collapses.

Capital Economics now models two paths : US$65 per barrel by year-end if the conflict resolves quickly, or US$130 in Q2 if it drags on, with a three-month conflict potentially averaging US$150 per barrel.

Gulf economies beyond crude

While most of the attention has been on the oil price, the damage to other parts of the global economy could be more long lasting, starting with economies in the gulf itself:

Refined products and LPG

Gulf states supply 3.3 million barrels per day of refined products and 1.5 million barrels per day of LPG , not just crude. Over three million barrels per day of Gulf refining capacity has already been shut. LNG prices have surged nearly 60% and jet fuel 65–120% since the conflict began.

Logistics

The logistics picture is just as alarming. Dubai's Jebel Ali port handles 15 million containers annually and connects to over 150 ports globally, and it's now running at one-fifth of normal capacity .

Over 500 Chinese companies use it as their regional distribution hub. Gulf airports handle roughly 10% of global air cargo volume, and more than 70% of flights to the UAE, Qatar, and Bahrain have been canceled.

A drone strike has already caused shrapnel damage to an AWS data center in Dubai – the first time a major cloud data center has been damaged in a war.

Fertilizer

Approximately one-third of global seaborne fertilizer trade transits the Strait . Gulf countries produce around 20% of global phosphate fertilizers and around 25% of global sulfur, two inputs that cannot be easily rerouted to alternative suppliers.

Fertilizer plants in India, Bangladesh, Pakistan, and Egypt have shut down or cut capacity from lost Qatari gas.

The global economy: Which economies and industries are most exposed?

Economies

Energy importers are amongst the most exposed. Japan imports roughly 75% of its oil from the Middle East and is the world's second-largest LNG importer . South Korea sources over 14% of its LNG from Qatar and the UAE alone, and imposed its first fuel price cap in nearly three decades .

India imports over 55% of its crude from the Middle East, and Qatar and the UAE account for more than 50% of its LNG supply, creating a dual crude-and-gas shock that did not apply in previous crises.

Equity markets in Japan, India and South Korea have been amongst the hardest hit the hardest, and also rallied most when Donald Trump told reporters the war was "very complete, pretty much."

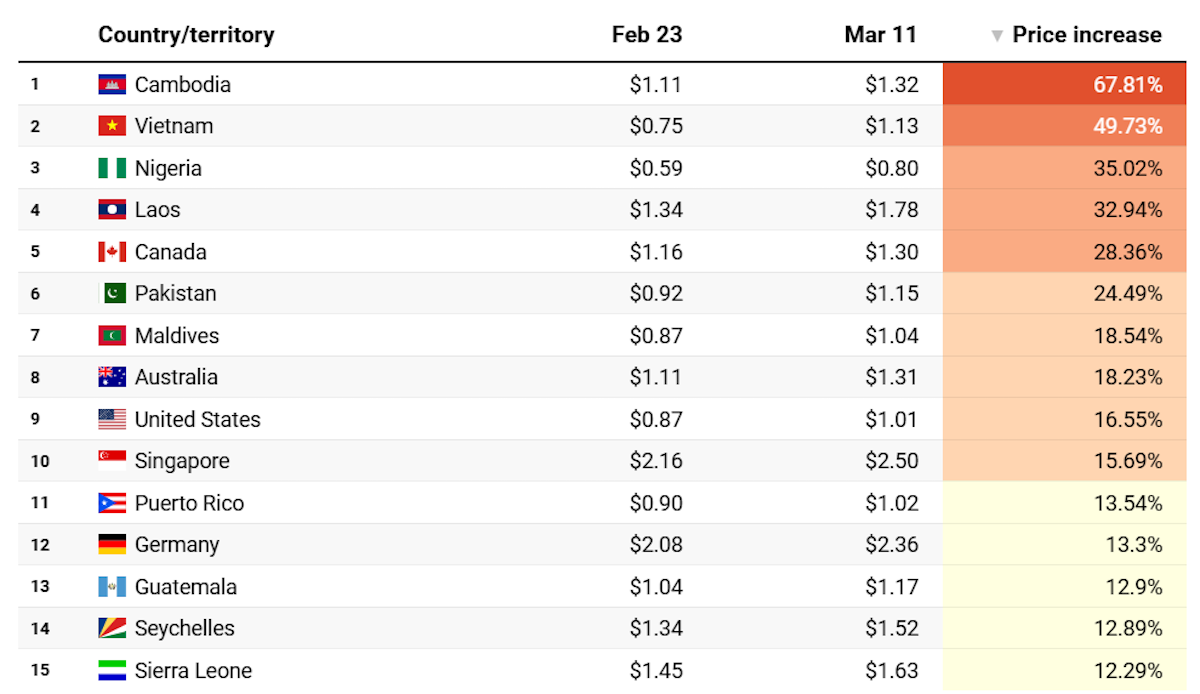

Emerging markets often suffer a ‘double-whammy’ when energy prices rise. Their currencies and debt sell-off, which makes imports even more expensive. Below we see the impact on petrol prices in less than three weeks.

Europe's vulnerability looks different but is equally structural. It entered 2026 with gas storage at 46 billion cubic meters , down from 60 billion cubic meters in February 2025 and 77 billion cubic meters in February 2024. It is now competing to buy LNG with equally desperate Asian buyers.

China is a notable outlier, so far. The country holds 1.4 billion barrels in strategic crude storage , receives Russian pipeline imports that bypass the Strait entirely, and Iranian vessels have allowed Chinese ships through the blockade. For now, Chinese manufacturers are facing a meaningfully lower energy cost shock than their Indian, Japanese, South Korean, and European competitors.

Head to the Simply Wall St Markets Page, pick a market (Japan, India, or the Eurozone are the obvious starting points right now), and check sector valuations. If a market has already repriced its energy-exposed sectors well below historical averages, you may be looking at an overshoot. If those sectors haven't moved much, the market might still be in denial.

Industries

Agriculture

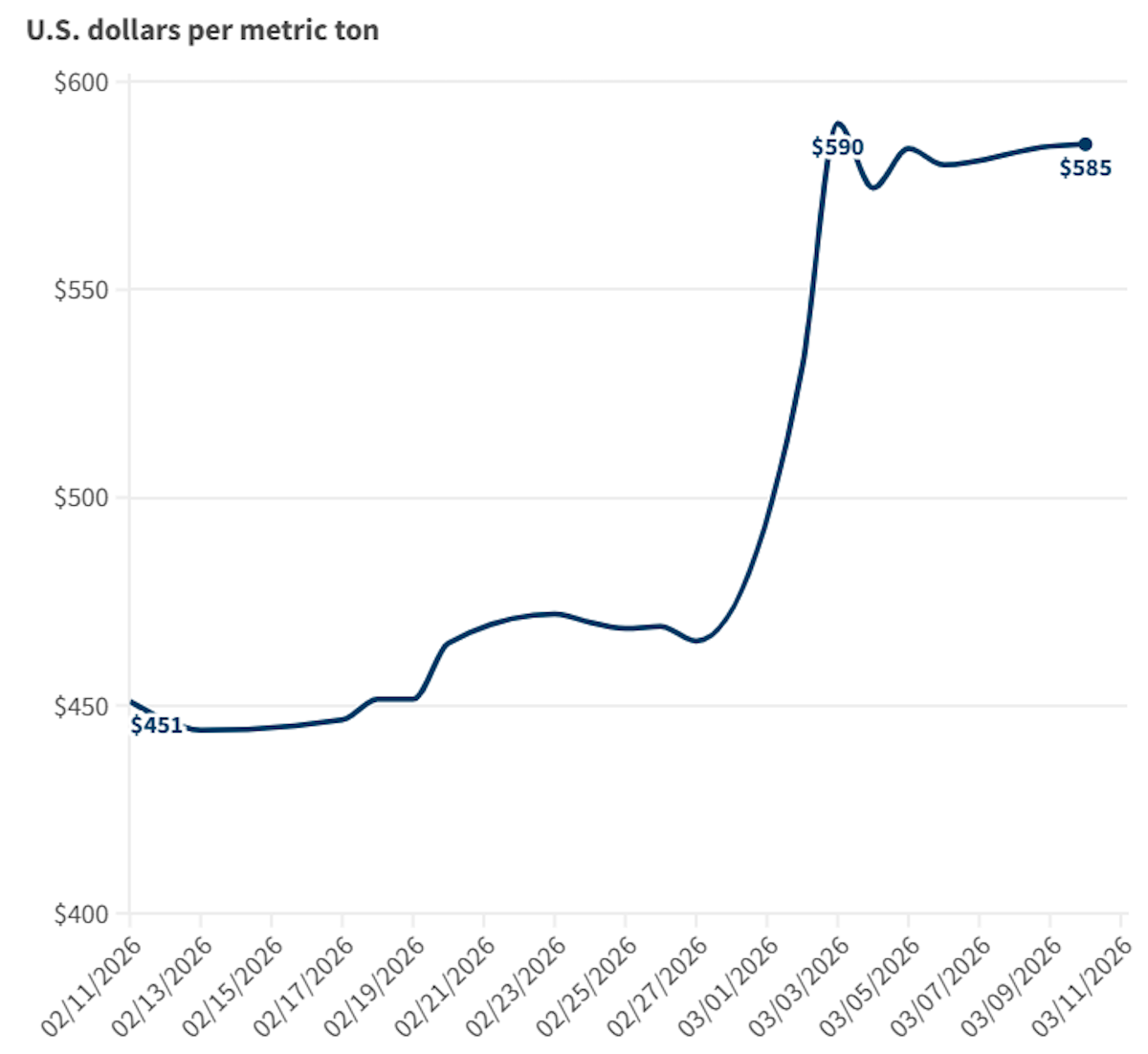

The potential impact on agriculture could be more permanent, and more widespread. Urea (high-nitrogen fertilizer) prices are up 25 to 30% since the blockade. If farmers can’t secure, or afford, fertilizer when they need it, they miss the opportunity to plant their crops. That affects yields and production months into the future, even if the blockade ends months before then.

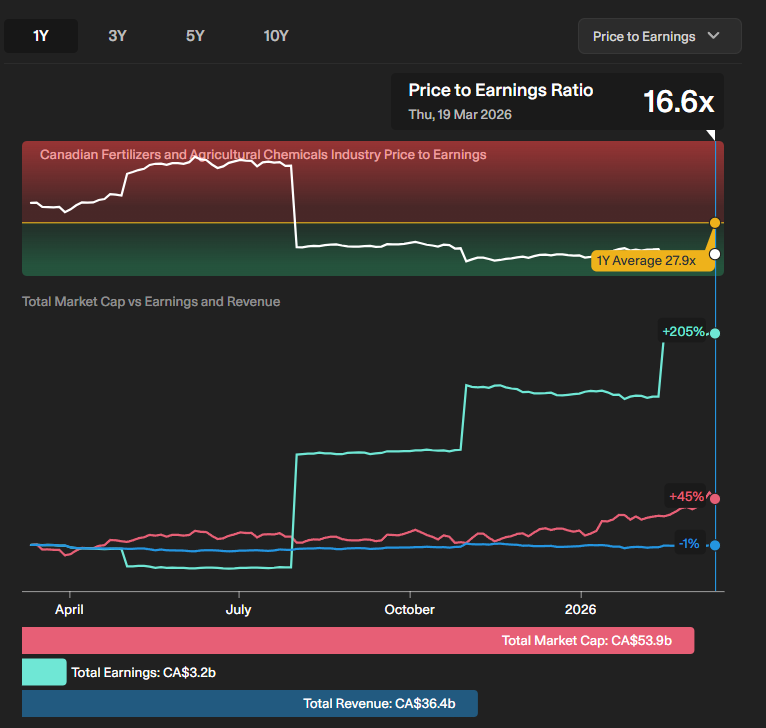

Potential winners? Have a look at the Fertilizers and Agricultural Producers screener - but check that companies aren’t dependent on imports from the Gulf.

Canadian producers (below) are one example:

The AI Infrastructure Build

Gulf sovereign wealth funds have been amongst the largest investors in AI infrastructure. GCC funds reportedly deployed US$126 billion globally in 2025, with some US$66 billion flowing into AI and digitalization .

In 2026, investments from those funds may be directed inward. That would increase competition for capital amongst AI infrastructure companies, as well as anyone else needing capital.

Gold may not be immune either

Typically, gold is a go to asset during a crisis. Not so this time around, with the metal down 15% since February. The price was already losing momentum after its massive run over the last few years. But one of the core narratives driving the gold price recently, central bank buying, is now also in doubt. Quite simply, central banks may need to use their reserves to stimulate local economies, and may be forced to sell some too.

Stagflation, and more headwinds for 60/40 portfolios

If the war drags on, stagflation could be a likely scenario. Higher energy prices, means higher inflation, and probably lower growth.

Analysts see Eurozone GDP tracking toward 0.5% with inflation above 4%. China risks falling below 3% growth, and the US holds at roughly 2.25% growth with 3% inflation. If that turns out to be correct, bonds and equities would both be under pressure.

Head to the Simply Wall St company report for any holding you're questioning and go straight to the Financial Health section. Check debt-to-equity and short-term coverage. If the snowflake is thin on the health axis, this is a good time to know.

The Insight: Navigating the Uncertainty

When a crisis like this occurs, markets find themselves pricing in scenarios that might not occur. And the knee jerk reaction often turns out to be wrong.

In 1990, during the First Gulf War, the oil price peaked as soon as the US launched strikes against Iraq. When Russia invaded Ukraine, the oil price also peaked with days of the invasion.

The chart below shows how differently things can play out each time there’s an oil shock.

As a long-term investor, here are a few things you can do:

- Beware of the obvious, and of crowded trades. The chance of huge reversals is high.

- Try to find companies that have strong fundamentals regardless of the war. Non-Gulf energy producers could be one, and agricultural commodity producers that aren’t dependent on imports from the region are another.

- Keep an eye on exposure to companies that were already exposed to higher inflation and interest rates.,i.e. emerging markets and highly leveraged companies.

- Be patient and wait for share prices to reach your fair value, based on long term fundamentals.

Key Events Next Week

Tuesday

-

🇯🇵 Japan National CPI YoY (Feb)

-

📉 Forecast: 1.3%, Previous: 1.5%

-

➡️ Why it matters: A rebound would support the BoJ's case for further gradual rate hikes later this year.

Wednesday

-

🇬🇧 UK CPI YoY (Feb)

-

📉 Forecast: 2.8%, Previous: 3.0%

-

➡️ Why it matters: The BoE forecasts CPI falling to 2.1% by the mid-2026, but current events will probably outweigh historical data.

Thursday

-

🇺🇸 US Initial Jobless Claims

-

📊 Previous : 205K

-

➡️ Why it matters : Weekly claims are the fastest labour market pulse so any spike would flag a consumer spending downturn.

Friday

-

🇬🇧 UK Retail Sales MoM (Feb)

-

📉 Forecast: 0.1%, Previous: 1.8%

-

➡️ Why it matters: January's 1.8% surge was the strongest since May 2024. A pullback is likely, but the size will signal consumer resilience.

-

🇺🇸 UoM Consumer Sentiment Final

-

📉 Forecast: 55.5, Previous: 56.6

-

➡️ Why it matters: Households are reacting to the Iran conflict and rising gas prices. This data point will be more closely watched than usual.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.