Advertisement

- United States

- /

- Professional Services

- /

- NYSE:CBZ

Will CBIZ's (CBZ) Strong Earnings Momentum Reshape Its Competitive Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- CBIZ, Inc. has announced it will share its third-quarter and year-to-date financial results for the period ended September 30, 2025, following market close on October 29, 2025, accompanied by a webcast conference call led by company leadership.

- This announcement comes as CBIZ is receiving increased attention for its solid revenue and earnings per share growth, particularly in comparison to industry peers facing more challenging conditions.

- We'll explore how CBIZ's upcoming earnings announcement, amid solid performance versus competitors, may influence its investment narrative and outlook.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

CBIZ Investment Narrative Recap

To be a shareholder in CBIZ, you need to believe that its expanded scale following the Marcum acquisition, resilient demand for essential business services, and improving technology offerings can drive sustained growth and margin expansion, even as pricing pressure and reliance on acquisition integration present ongoing challenges. The upcoming Q3 earnings announcement is unlikely to materially shift the primary short-term catalyst, which remains the successful integration of Marcum, but it will provide a timely check on progress and pricing trends; meanwhile, the most pressing risk continues to be persistent pricing pressure, especially if market constraints prove structural rather than cyclical.

Of the recent company disclosures, CBIZ’s continued share repurchase activity is particularly relevant, signaling underlying confidence in long-term value despite sector volatility and near-term margin pressure. These buybacks, alongside integration progress updates, serve as a key focal point as investors watch for signs that CBIZ can leverage its new scale to enhance profitability beyond industry peers.

By contrast, investors should be aware that a structural shift in pricing pressures could have longer-lasting effects on revenue growth and...

Read the full narrative on CBIZ (it's free!)

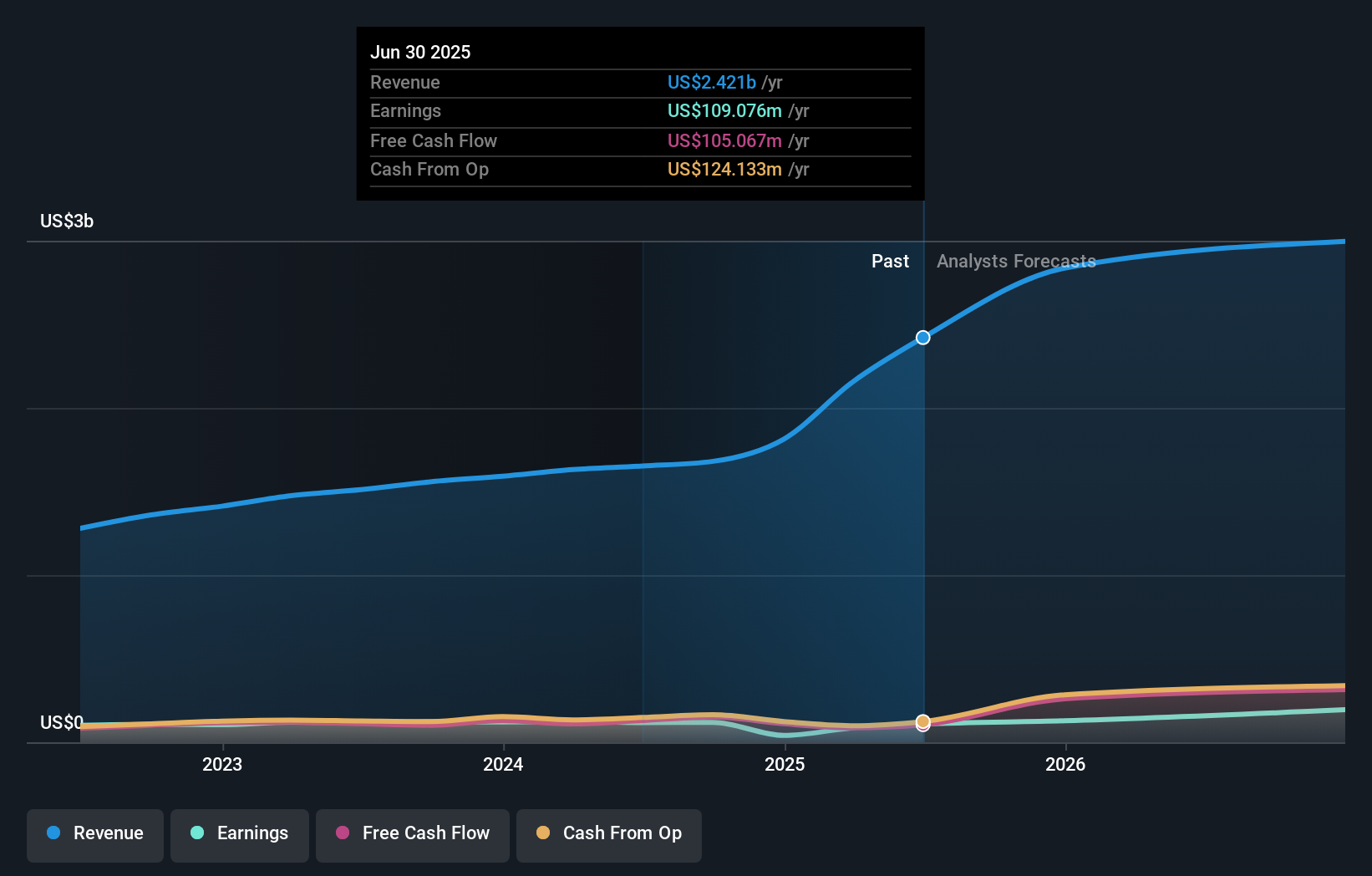

CBIZ's narrative projects $3.3 billion in revenue and $257.7 million in earnings by 2028. This requires 10.9% yearly revenue growth and a $148.6 million increase in earnings from the current $109.1 million.

Uncover how CBIZ's forecasts yield a $95.00 fair value, a 82% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members shared two fair value estimates for CBIZ ranging from US$95 to US$226.52 per share. Against this backdrop of differing outlooks, the sustained integration costs from recent acquisitions may shape your own view of future returns and margin stability.

Explore 2 other fair value estimates on CBIZ - why the stock might be worth just $95.00!

Build Your Own CBIZ Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CBIZ research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free CBIZ research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CBIZ's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CBZ

CBIZ

Provides financial, insurance, and advisory services in the United States and Canada.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets