Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:VRSK

How Verisk Analytics’ (VRSK) Earnix Integration Could Redefine Insurance Rating Automation and Compliance

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 12, 2025, Earnix announced a new integration with Verisk Analytics, enabling insurance carriers to import Verisk's ISO Electronic Rating Content directly into Earnix's Price-It enterprise pricing engine for faster, automated model updates and streamlined compliance processes.

- This collaboration promises to help insurers accelerate regulatory filings, reduce operational rework, and ease the adoption of state or circular rating changes by leveraging automation and impact analysis tools.

- We'll examine how this integration, which aims to automate complex insurance rating updates for clients, could shape Verisk Analytics' investment narrative going forward.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

Verisk Analytics Investment Narrative Recap

To be comfortable as a Verisk Analytics shareholder, you need to believe in insurers transitioning to automation for pricing, compliance, and regulatory updates. The recent Earnix partnership could enhance Verisk’s value proposition for core clients, but short-term results are still far more influenced by insurers’ willingness to spend in an uncertain insurance and macro environment, a factor that this news alone is unlikely to materially change.

Of recent company announcements, the Q3 2025 earnings report stands out as most relevant, revealing net income growth alongside a downward revision in revenue guidance. The integration with Earnix may support Verisk’s long-term data analytics revenue growth, yet current headwinds, including client sector caution and slower projected top-line growth, remain the dominant near-term catalysts for performance.

However, investors should take note of the persistent risk that volatile insurance markets and macroeconomic pressures could still limit clients’ spending on data services...

Read the full narrative on Verisk Analytics (it's free!)

Verisk Analytics' outlook anticipates $3.9 billion in revenue and $1.2 billion in earnings by 2028. This projection is based on a 9.1% annual revenue growth rate and an increase in earnings of about $290 million from the current $909.3 million.

Uncover how Verisk Analytics' forecasts yield a $251.29 fair value, a 13% upside to its current price.

Exploring Other Perspectives

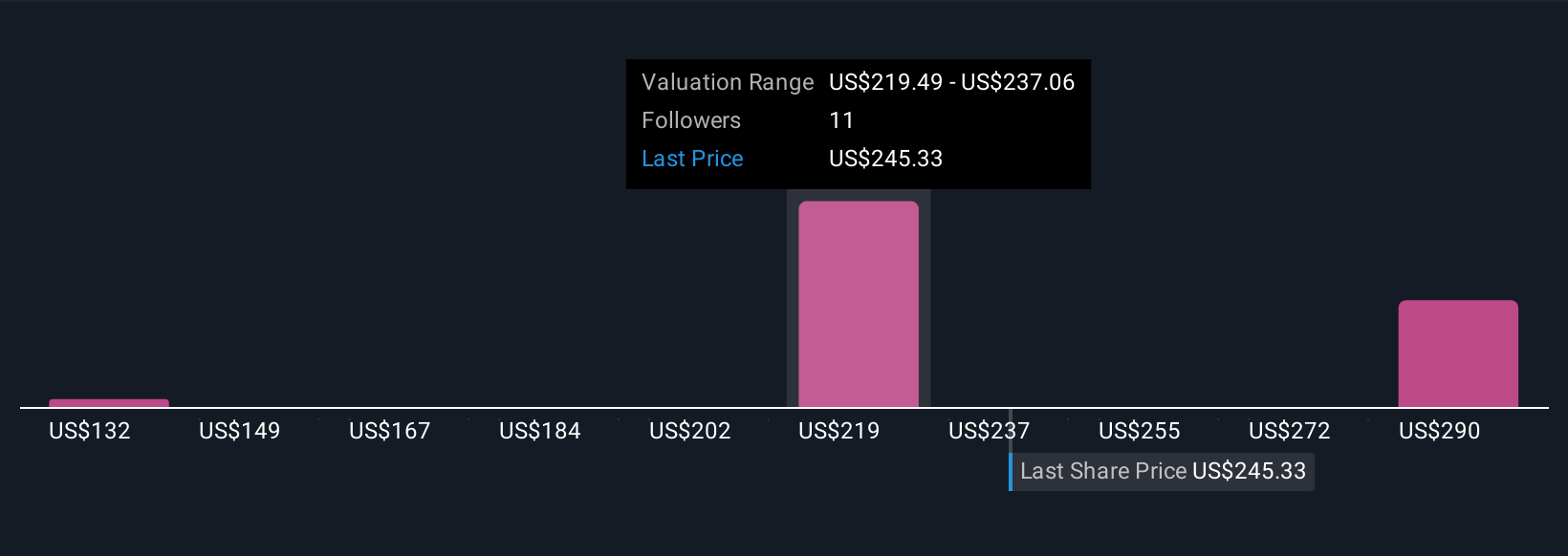

Fair value estimates for Verisk from four Simply Wall St Community members range from US$131.67 to US$277.85 per share, highlighting substantial differences in outlook. Some investors see long-term revenue growth from product innovation, though continued insurer caution could significantly affect near-term financial results.

Explore 4 other fair value estimates on Verisk Analytics - why the stock might be worth as much as 25% more than the current price!

Build Your Own Verisk Analytics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Verisk Analytics research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Verisk Analytics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Verisk Analytics' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRSK

Verisk Analytics

Engages in the provision of data analytics and technology solutions to the insurance industry in the United States and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative