Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:UPWK

Should You Investigate Upwork Inc. (NASDAQ:UPWK) At US$12.25?

Upwork Inc. (NASDAQ:UPWK), is not the largest company out there, but it received a lot of attention from a substantial price movement on the NASDAQGS over the last few months, increasing to US$15.66 at one point, and dropping to the lows of US$12.25. Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether Upwork's current trading price of US$12.25 reflective of the actual value of the small-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let’s take a look at Upwork’s outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

View our latest analysis for Upwork

What's The Opportunity In Upwork?

According to our price multiple model, where we compare the company's price-to-earnings ratio to the industry average, the stock currently looks expensive. In this instance, we’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. We find that Upwork’s ratio of 35.9x is above its peer average of 25.91x, which suggests the stock is trading at a higher price compared to the Professional Services industry. But, is there another opportunity to buy low in the future? Given that Upwork’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us another chance to buy in the future. This is based on its high beta, which is a good indicator for share price volatility.

What kind of growth will Upwork generate?

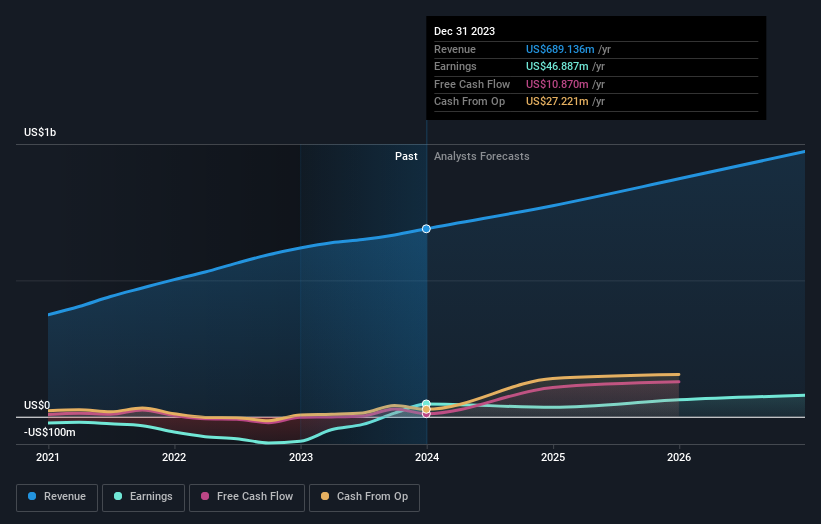

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Upwork's earnings over the next few years are expected to increase by 67%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

What This Means For You

Are you a shareholder? It seems like the market has well and truly priced in UPWK’s positive outlook, with shares trading above industry price multiples. However, this brings up another question – is now the right time to sell? If you believe UPWK should trade below its current price, selling high and buying it back up again when its price falls towards the industry PE ratio can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on UPWK for some time, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the optimistic prospect is encouraging for UPWK, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. To that end, you should learn about the 2 warning signs we've spotted with Upwork (including 1 which can't be ignored).

If you are no longer interested in Upwork, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:UPWK

Upwork

Operates a work marketplace that connects businesses with various independent professionals and agencies in the United States, India, the Philippines, and internationally.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|6.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor