- United States

- /

- Trade Distributors

- /

- NasdaqGS:MGRC

McGrath RentCorp (NASDAQ:MGRC) Looks Like A Good Stock, And It's Going Ex-Dividend Soon

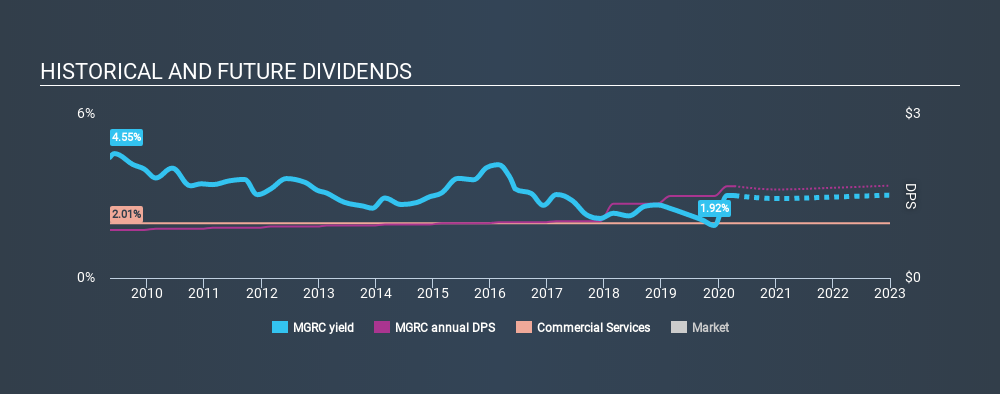

McGrath RentCorp (NASDAQ:MGRC) stock is about to trade ex-dividend in 2 days time. If you purchase the stock on or after the 14th of April, you won't be eligible to receive this dividend, when it is paid on the 30th of April.

McGrath RentCorp's next dividend payment will be US$0.42 per share, on the back of last year when the company paid a total of US$1.50 to shareholders. Based on the last year's worth of payments, McGrath RentCorp has a trailing yield of 3.0% on the current stock price of $55.72. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether McGrath RentCorp has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for McGrath RentCorp

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. McGrath RentCorp paid out a comfortable 38% of its profit last year. A useful secondary check can be to evaluate whether McGrath RentCorp generated enough free cash flow to afford its dividend. Dividends consumed 67% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's positive to see that McGrath RentCorp's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Fortunately for readers, McGrath RentCorp's earnings per share have been growing at 18% a year for the past five years. McGrath RentCorp has an average payout ratio which suggests a balance between growing earnings and rewarding shareholders. Given the quick rate of earnings per share growth and current level of payout, there may be a chance of further dividend increases in the future.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. McGrath RentCorp has delivered 6.7% dividend growth per year on average over the past ten years. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

To Sum It Up

From a dividend perspective, should investors buy or avoid McGrath RentCorp? From a dividend perspective, we're encouraged to see that earnings per share have been growing, the company is paying out less than half of its earnings, and a bit over half its free cash flow. It's a promising combination that should mark this company worthy of closer attention.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. In terms of investment risks, we've identified 2 warning signs with McGrath RentCorp and understanding them should be part of your investment process.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:MGRC

McGrath RentCorp

Operates as a business-to-business rental company in the United States and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)