Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:DRVN

Results: Driven Brands Holdings Inc. Beat Earnings Expectations And Analysts Now Have New Forecasts

As you might know, Driven Brands Holdings Inc. (NASDAQ:DRVN) just kicked off its latest quarterly results with some very strong numbers. It was a solid earnings report, with revenues and statutory earnings per share (EPS) both coming in strong. Revenues were 16% higher than the analysts had forecast, at US$375m, while EPS were US$0.21 beating analyst models by 57%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Driven Brands Holdings after the latest results.

View our latest analysis for Driven Brands Holdings

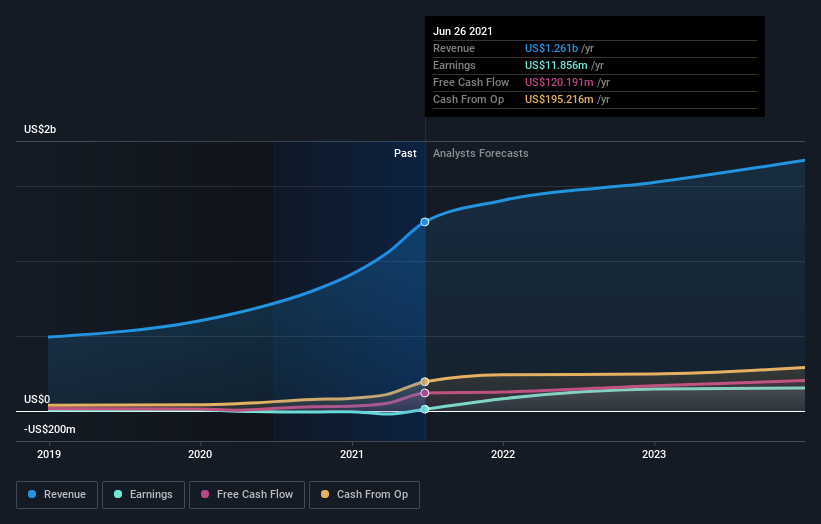

After the latest results, the eight analysts covering Driven Brands Holdings are now predicting revenues of US$1.40b in 2021. If met, this would reflect a solid 11% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to leap 482% to US$0.50. In the lead-up to this report, the analysts had been modelling revenues of US$1.31b and earnings per share (EPS) of US$0.27 in 2021. So it seems there's been a definite increase in optimism about Driven Brands Holdings' future following the latest results, with a very substantial lift in the earnings per share forecasts in particular.

It will come as no surprise to learn that the analysts have increased their price target for Driven Brands Holdings 7.3% to US$39.33on the back of these upgrades. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Driven Brands Holdings, with the most bullish analyst valuing it at US$47.00 and the most bearish at US$32.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Driven Brands Holdings shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that Driven Brands Holdings' revenue growth is expected to slow, with the forecast 24% annualised growth rate until the end of 2021 being well below the historical 74% growth over the last year. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.9% per year. So it's pretty clear that, while Driven Brands Holdings' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Driven Brands Holdings' earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Driven Brands Holdings analysts - going out to 2023, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 2 warning signs for Driven Brands Holdings (of which 1 can't be ignored!) you should know about.

If you decide to trade Driven Brands Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:DRVN

Driven Brands Holdings

Provides automotive services to retail and commercial customers in the United States, Canada, and internationally.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor