Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:ADP

Does ADP’s Recent Product Innovations Signal a Hidden Opportunity for Investors in 2025?

Reviewed by Bailey Pemberton

- Wondering if Automatic Data Processing is trading at a fair price or if there's untapped value hidden in plain sight? You're not alone in asking that question.

- Lately, the stock has been a bit of a mixed bag: it nudged up 0.5% over the last week, dipped 2.6% in the past month, and is down 12.2% so far this year. These shifts suggest both opportunity and caution among investors.

- Much of this movement has happened as investors digest broader market volatility and shifting demand for outsourcing and HR technology services. Recently, headlines have focused on the company's product innovations and increased competition in payroll technology, fueling both optimism and speculation about its future direction.

- On the valuation front, Automatic Data Processing scores a 3 out of 6 on our undervaluation checks, so there is a lot to unpack. We will break down what traditional metrics say next, and provide a different way to look at valuation that you may find interesting.

Approach 1: Automatic Data Processing Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model works by estimating a company's future cash flows and discounting them back to today’s value. This provides a snapshot of what the business is intrinsically worth. The calculation incorporates both analyst forecasts and longer-term projections to determine whether a stock is undervalued or overvalued based on its future earnings potential.

For Automatic Data Processing, the most recent Free Cash Flow reported is $4.16 Billion. Analyst consensus points to steady annual growth, projecting Free Cash Flow to rise to $5.58 Billion by 2028, with further increases extrapolated out to 2035. While analyst estimates are available up to five years, long-term projections are provided to give a broader perspective.

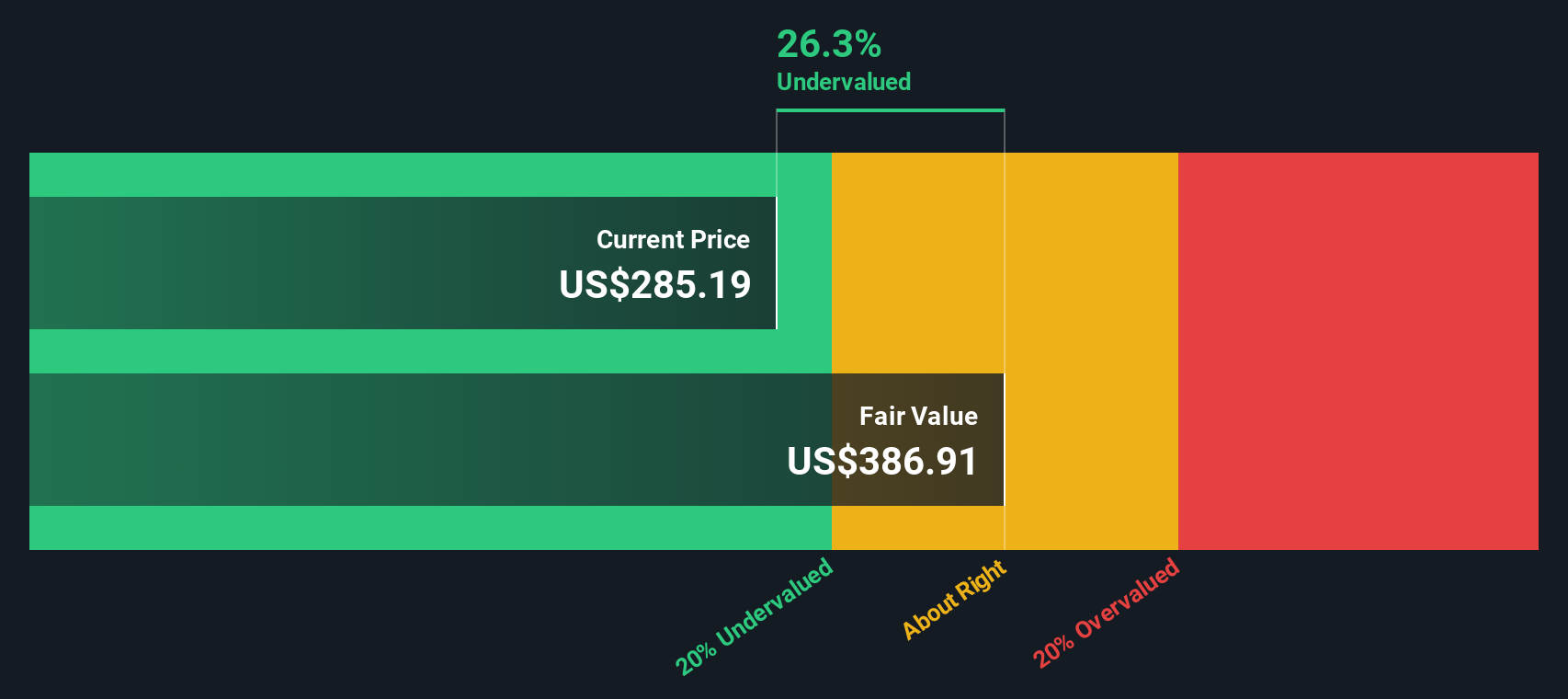

After discounting these future cash flows back to present value using the 2 Stage Free Cash Flow to Equity model, the estimated intrinsic fair value per share is $316.40. This represents a 19.6% discount compared to the current market price, suggesting that the stock is meaningfully undervalued at present.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Automatic Data Processing is undervalued by 19.6%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

Approach 2: Automatic Data Processing Price vs Earnings

The Price-to-Earnings (PE) ratio is widely regarded as the preferred multiple for valuing consistently profitable companies like Automatic Data Processing. It offers a clear snapshot of what investors are willing to pay today for a dollar of current earnings, making it especially relevant for businesses with steady profitability and established earnings histories.

However, what constitutes a "normal" or "fair" PE ratio depends on several factors. Higher growth expectations, stronger profitability, or lower perceived risks can all support premium valuations, while slower growth or elevated risks tend to justify lower ratios. Comparing a company’s PE with industry averages and competitors provides initial context, but does not always tell the full story.

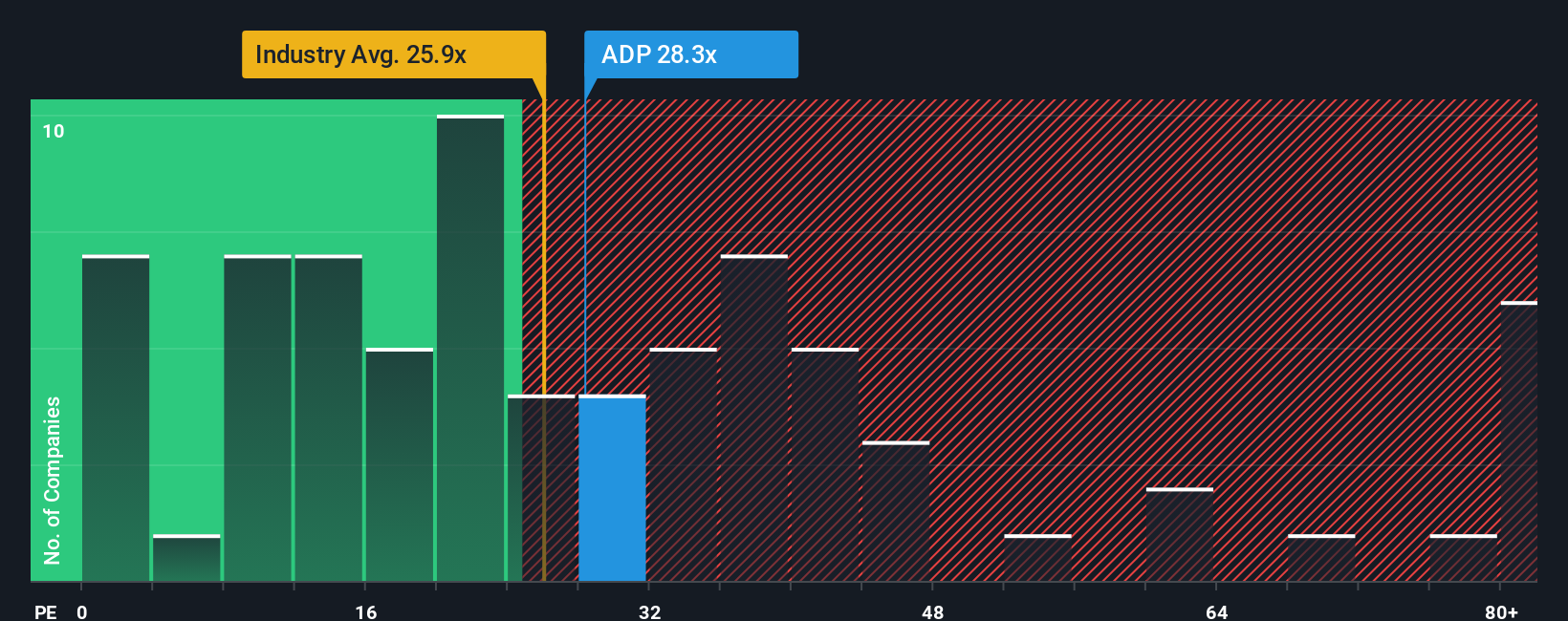

Currently, Automatic Data Processing trades at a PE ratio of 24.9x. This is slightly above the broader Professional Services industry average of 24.3x, but below the peer group average of 27.2x. To provide a more tailored benchmark, Simply Wall St calculates a “Fair Ratio” based on a blend of factors, such as the company’s market cap, earnings growth rates, profit margins, industry trends, and risk profile. In ADP’s case, the calculated Fair Ratio is 29.8x.

The Fair Ratio is a comprehensive gauge, factoring in more than simple averages do. It blends forward-looking growth prospects and quality signals, so it better reflects what investors ought to pay, rather than what others are currently paying for similar stocks. When we compare ADP’s current PE with its Fair Ratio, the current multiple is noticeably lower, suggesting the stock is trading below its intrinsic value based on its fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Automatic Data Processing Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple, user-driven story behind a company’s numbers, where you get to spell out your assumptions on fair value, and map out how you think future revenue, earnings, or margins will play out, backing up your views with real estimates and logic.

Unlike traditional models, Narratives seamlessly tie together a company’s story with a customized financial forecast, and then connect that to a clear fair value, so every number actually means something in context. The best part is that Narratives are quick to create and even quicker to update; they are built right into Simply Wall St’s Community page, used by millions of investors worldwide.

Narratives cut through the noise, helping you make investment decisions by showing whether a stock’s Fair Value stacks up favorably against the current market Price, so you can act on your own convictions, not just market consensus. And whenever news, earnings, or company developments surface, Narratives respond instantly to incorporate that fresh data and demonstrate how it impacts your case.

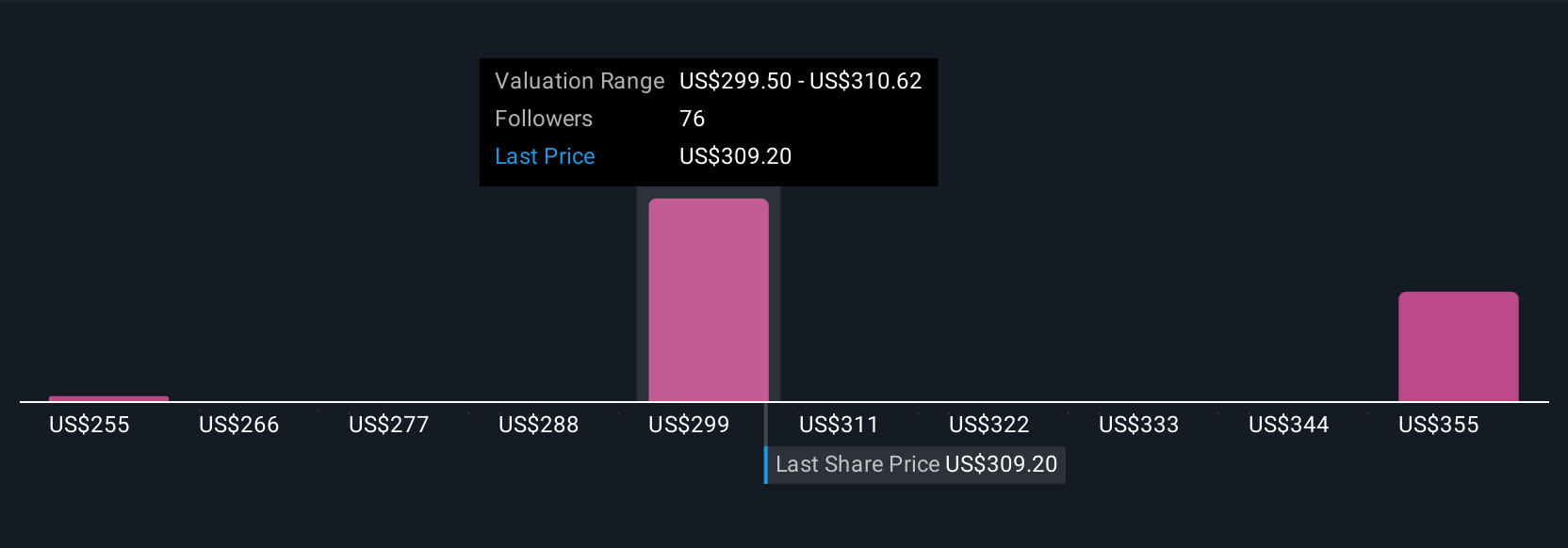

For Automatic Data Processing, one investor’s Narrative might point to rapid AI adoption and a $387 per share fair value, while another’s could highlight slower payroll growth and see just $293 as fair. Each story reflects a different, but valid, way to interpret the same stock.

Do you think there's more to the story for Automatic Data Processing? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADP

Automatic Data Processing

Provides cloud-based human capital management (HCM) solutions worldwide.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

20 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

DS

DS2invest on PayPal Holdings ·

PayPal: Undervalued Cash Flow Machine or Value Trap?

Fair Value:US$69.0318.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MI

MineStackr on AbraSilver Resource ·

NAV $4B CAD

Fair Value:CA$3661.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0