Advertisement

- United States

- /

- Machinery

- /

- NYSE:XYL

There May Be Underlying Issues With The Quality Of Xylem's (NYSE:XYL) Earnings

Unsurprisingly, Xylem Inc.'s (NYSE:XYL) stock price was strong on the back of its healthy earnings report. However, our analysis suggests that shareholders may be missing some factors that indicate the earnings result was not as good as it looked.

Check out our latest analysis for Xylem

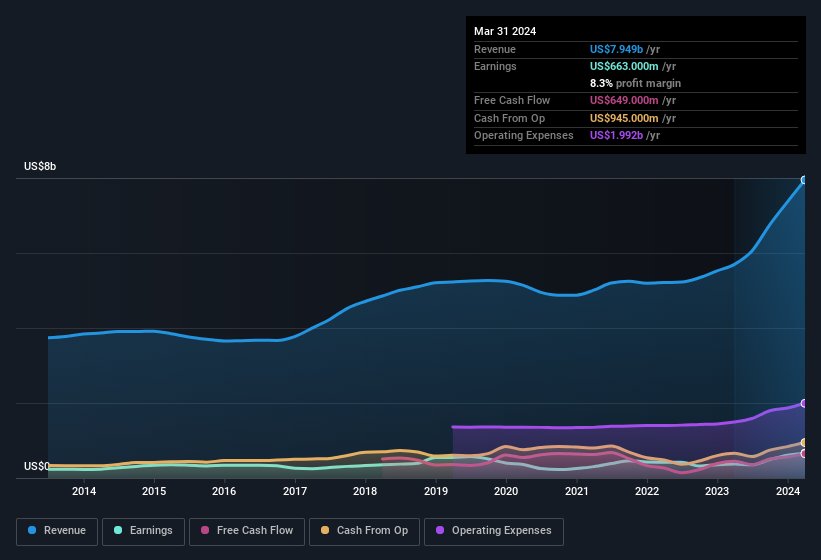

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. Xylem expanded the number of shares on issue by 34% over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Xylem's historical EPS growth by clicking on this link.

How Is Dilution Impacting Xylem's Earnings Per Share (EPS)?

As you can see above, Xylem has been growing its net income over the last few years, with an annualized gain of 119% over three years. But EPS was only up 70% per year, in the exact same period. And the 78% profit boost in the last year certainly seems impressive at first glance. On the other hand, earnings per share are only up 38% in that time. So you can see that the dilution has had a fairly significant impact on shareholders.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So Xylem shareholders will want to see that EPS figure continue to increase. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Xylem's profit suffered from unusual items, which reduced profit by US$210m in the last twelve months. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Xylem to produce a higher profit next year, all else being equal.

Our Take On Xylem's Profit Performance

Xylem suffered from unusual items which depressed its profit in its last report; if that is not repeated then profit should be higher, all else being equal. But unfortunately the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income. Based on these factors, we think it's very unlikely that Xylem's statutory profits make it seem much weaker than it is. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. At Simply Wall St, we found 3 warning signs for Xylem and we think they deserve your attention.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:XYL

Xylem

Engages in the design, manufacture, and servicing of engineered products and solutions for utility, industrial, and residential and commercial building services settings worldwide.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor