Advertisement

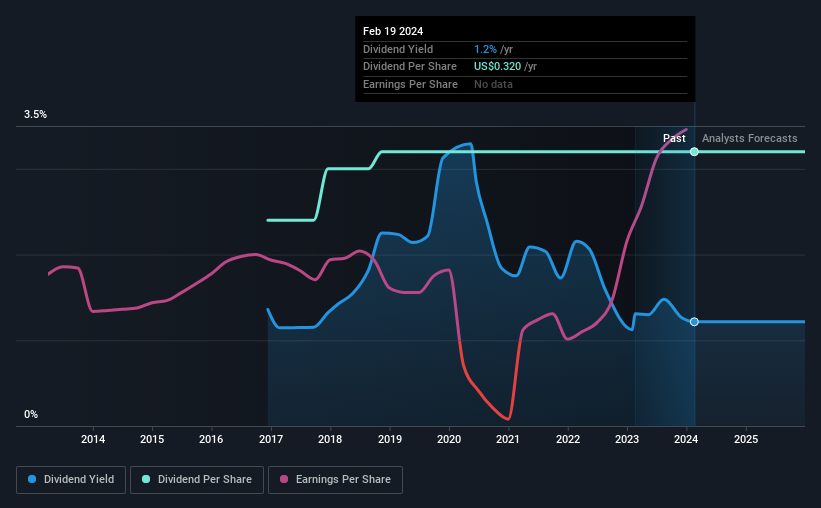

Wabash National Corporation (NYSE:WNC) has announced that it will pay a dividend of $0.08 per share on the 25th of April. This means the annual payment will be 1.2% of the current stock price, which is lower than the industry average.

Check out our latest analysis for Wabash National

Wabash National's Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. However, Wabash National's earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

Looking forward, earnings per share is forecast to fall by 72.9% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could be 25%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Wabash National Doesn't Have A Long Payment History

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. The dividend has gone from an annual total of $0.24 in 2017 to the most recent total annual payment of $0.32. This implies that the company grew its distributions at a yearly rate of about 4.2% over that duration. We like that the dividend hasn't been shrinking. However we're conscious that the company hasn't got an overly long track record of dividend payments yet, which makes us wary of relying on its dividend income.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see that Wabash National has been growing its earnings per share at 33% a year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

We Really Like Wabash National's Dividend

Overall, we like to see the dividend staying consistent, and we think Wabash National might even raise payments in the future. The company is generating plenty of cash, and the earnings also quite easily cover the distributions. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come across 2 warning signs for Wabash National you should be aware of, and 1 of them makes us a bit uncomfortable. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Wabash National might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WNC

Wabash National

Manufactures engineered solutions and services for transportation, logistics and infrastructure industry in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor