Advertisement

- United States

- /

- Machinery

- /

- NYSE:PH

Parker-Hannifin (NYSE:PH) Will Pay A Larger Dividend Than Last Year At $1.80

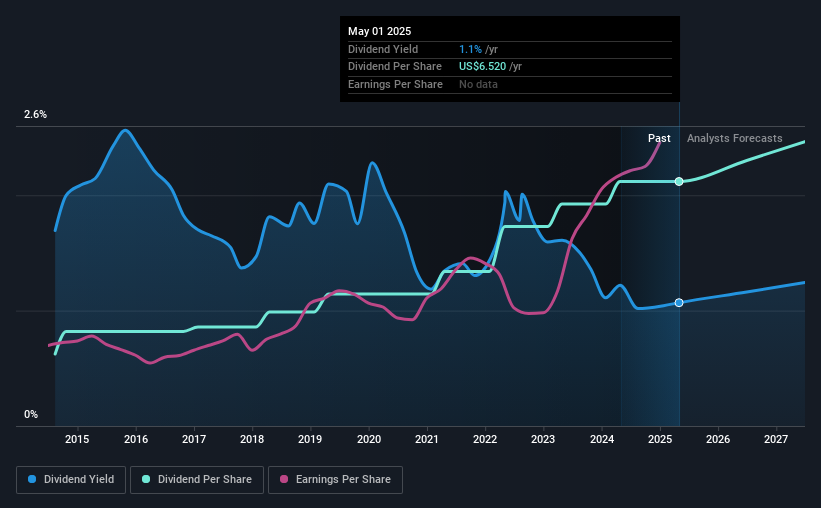

Parker-Hannifin Corporation (NYSE:PH) will increase its dividend on the 6th of June to $1.80, which is 10% higher than last year's payment from the same period of $1.63. Although the dividend is now higher, the yield is only 1.1%, which is below the industry average.

Our free stock report includes 1 warning sign investors should be aware of before investing in Parker-Hannifin. Read for free now.Parker-Hannifin's Payment Could Potentially Have Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. Before making this announcement, Parker-Hannifin was easily earning enough to cover the dividend. This means that most of what the business earns is being used to help it grow.

The next year is set to see EPS grow by 21.8%. If the dividend continues on this path, the payout ratio could be 25% by next year, which we think can be pretty sustainable going forward.

See our latest analysis for Parker-Hannifin

Parker-Hannifin Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2015, the annual payment back then was $1.92, compared to the most recent full-year payment of $6.52. This means that it has been growing its distributions at 13% per annum over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. We are encouraged to see that Parker-Hannifin has grown earnings per share at 19% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

We Really Like Parker-Hannifin's Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Parker-Hannifin that investors should take into consideration. Is Parker-Hannifin not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PH

Parker-Hannifin

Manufactures and sells motion and control technologies and systems for various mobile, industrial, and aerospace markets worldwide.

Outstanding track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor