Gorman-Rupp (GRC) shares have recently gained traction, delivering an 18% return over the past 3 months. As investors watch for the company's next move, the stock's recent momentum highlights ongoing interest in industrial equipment makers.

Gorman-Rupp’s share price has built steady momentum this year, with an impressive 1-year total shareholder return of 16% and nearly doubling investors’ money over the last three years. Recent movement suggests investors are starting to factor in improved growth outlook and resilience, which keeps the stock’s performance firmly on watch.

With strong recent gains and a record of outperformance, the critical question now is whether Gorman-Rupp’s stock is still undervalued or if investors have already priced in the company’s brighter outlook, which may leave little room for a bargain opportunity.

Advertisement

Price-to-Earnings of 22.5x: Is it justified?

At a price-to-earnings (P/E) ratio of 22.5x, Gorman-Rupp trades below its peer group average of 40.2x, as well as just under the US Machinery industry’s average of 23.8x. The current share price of $44.4 places the stock at a modest discount relative to its closest sector peers.

The price-to-earnings ratio reflects how much investors are willing to pay for each dollar of earnings. In the industrial equipment sector, P/E is a key benchmark. Companies with reliable profit growth and resilience often garner higher multiples.

Gorman-Rupp’s P/E is notably lower than sector averages and peers, which could signal that the market doubts the sustainability of its recent robust earnings growth or simply has not caught up to its potential. If the market recognizes lasting improvements, there is room for the share price to move closer to its fair ratio.

When comparing to the machinery industry and the estimated fair price-to-earnings ratio of 18.8x, Gorman-Rupp’s multiple hovers slightly above fair value, but still offers better relative value than its peer group. This gap may attract investors searching for an industrial outlier with increasing profits.

However, there are still risks, including a slowdown in industrial demand or weaker-than-expected earnings, that could limit further upside for Gorman-Rupp shares.

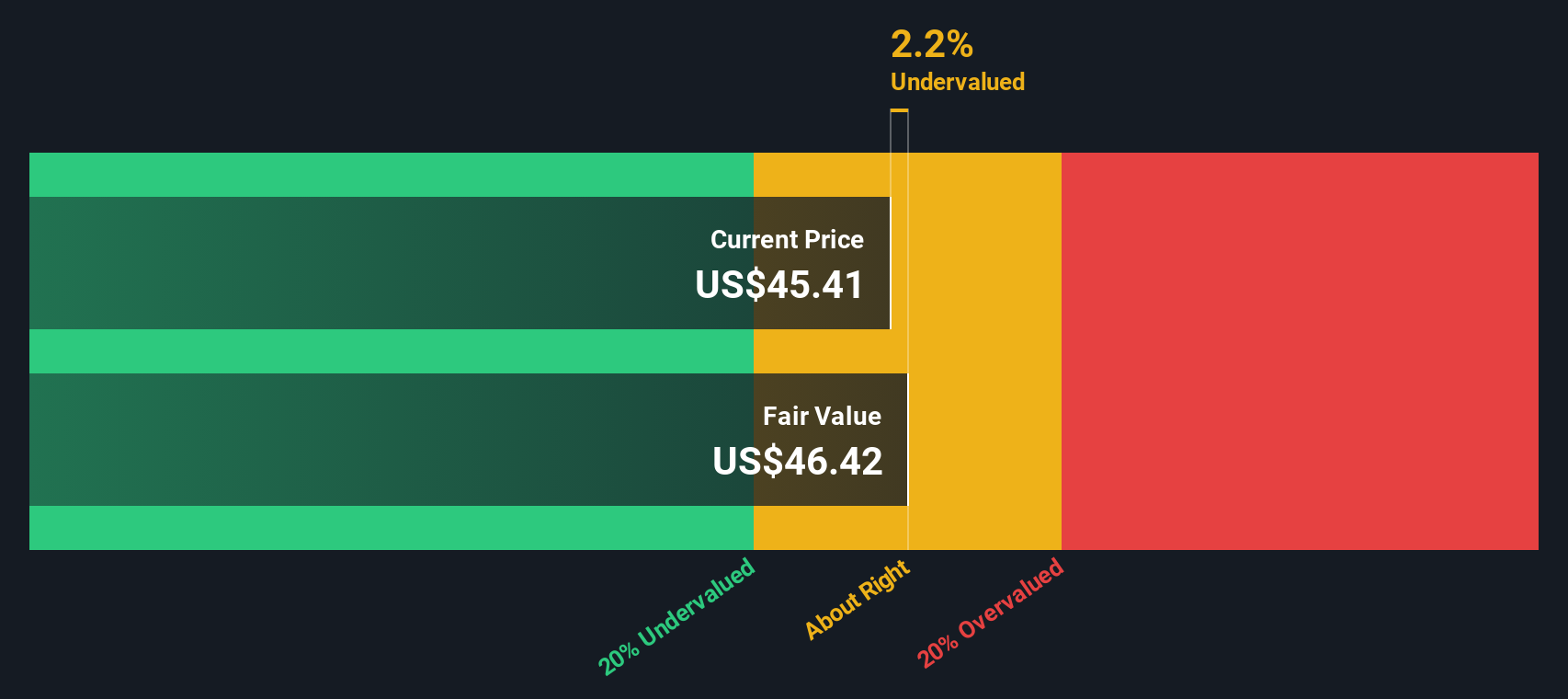

The SWS DCF model estimates that Gorman-Rupp is trading about 4.6% below its calculated fair value. This suggests there may still be some upside left in the share price. While multiples tell one story, discounted cash flow uses projected future earnings to offer a different perspective on what the stock could be worth. Which view best captures where the company will go next?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Gorman-Rupp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Gorman-Rupp Narrative

If you want to run your own analysis or come to your own conclusion, take a few minutes and see what story the numbers tell. Do it your way

A great starting point for your Gorman-Rupp research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Staying ahead means acting on fresh opportunities before others do. Don’t limit your portfolio to just one winner when new trends are gaining momentum right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks