Advertisement

- United States

- /

- Machinery

- /

- NYSE:CMI

Cummins (CMI) Valuation: Analyst Upgrade Highlights Potential of Electrification and Hydrogen Strategy

Simply Wall St

Reviewed by Kshitija Bhandaru

Recent activity around Cummins (CMI) has caught investors’ interest following a fresh upgrade from Hold to Buy by Melius Research. The company’s advances in electrification, hydrogen, and stationary storage are fueling optimism about future growth.

See our latest analysis for Cummins.

Momentum has been quietly building for Cummins, with its steady stream of innovation and a recent analyst upgrade nudging the share price to new highs. While the share price return remains modest over the past year, long-term total shareholder returns paint a stronger picture. This underscores how investor optimism is growing as Cummins expands into electrification and hydrogen technologies.

If Cummins’ progress has you thinking bigger, now is a smart time to broaden your discovery and explore See the full list for free.

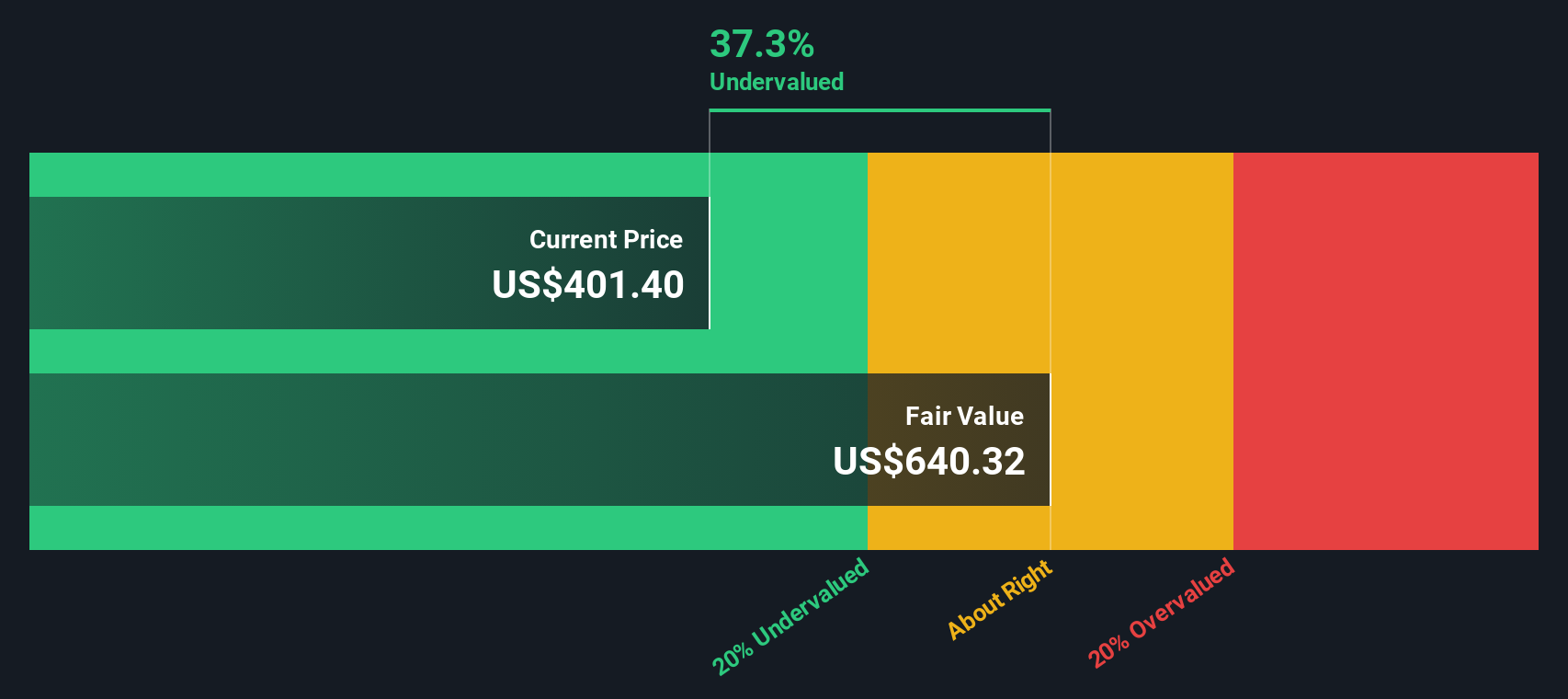

Despite the upbeat outlook and record-high share price, Cummins still trades below its analyst target and intrinsic value. Does this disconnect suggest an upside opportunity, or is the market already pricing in Cummins’ next wave of growth?

Most Popular Narrative: Fairly Valued

With Cummins’ current share price close to its analyst consensus fair value, the market seems to be weighing recent advances and future growth cautiously. The narrative highlights the company’s ability to capture new opportunities, but investor expectations remain in balance with these prospects.

Ongoing investments in electrification, hydrogen, and stationary energy storage broaden Cummins' long-term addressable market. As secular decarbonization trends accelerate, these initiatives can unlock new revenue streams and recurring income (aftersales, services), ultimately supporting long-term earnings growth.

Could Cummins’ aggressive push into next-generation power tech transform its profit picture? The fair value calculation hints at surprising projections for margins and forward earnings. Want to see what future growth assumptions are driving this consensus target? The missing numbers might challenge your expectations.

Result: Fair Value of $424.98 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weakness in North American truck demand or ongoing regulatory uncertainty could quickly challenge these positive growth assumptions for Cummins.

Find out about the key risks to this Cummins narrative.

Another View: Discounted Cash Flow Upside

Taking a different approach, our DCF model values Cummins at $611.39. This is significantly above both its current price and the analyst consensus. This suggests the market may be underpricing the company’s true earnings and cash generation potential. Could Wall Street be missing a longer-term opportunity?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Cummins Narrative

If you have a different take or want to shape your own outlook, try building your own narrative with the data in just a few minutes. Do it your way

A great starting point for your Cummins research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Jump on unique opportunities before the crowd catches on. Use the Simply Wall Street Screener to uncover the smartest plays across rapidly changing markets.

- Boost your portfolio’s long-term income by targeting high-yield payouts with these 19 dividend stocks with yields > 3% that consistently reward shareholders.

- Tap into early-stage innovation with these 24 AI penny stocks as artificial intelligence reshapes entire industries and launches new market leaders.

- Secure value now by grabbing these 896 undervalued stocks based on cash flows trading below their true potential and position yourself ahead of the next big move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CMI

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor