Advertisement

- United States

- /

- Electrical

- /

- NYSE:BE

Is Bloom Energy’s 349% Surge in 2025 Still Supported by Its Fundamentals?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Bloom Energy is still a smart buy after its massive run, or if you are late to the party, you are in the right place. This article focuses on what the current share price really implies.

- After a blistering 349.3% gain year to date and 301.7% over the last year, the stock has still been choppy, with an 11.4% rise in the past week but a 20.6% pullback over the last 30 days that hints at shifting risk appetite.

- Recent headlines have focused on Bloom Energy's positioning in clean hydrogen and distributed power, including new partnerships and project announcements that highlight growing demand for reliable, lower carbon energy solutions. At the same time, market chatter around policy incentives and the long term viability of hydrogen infrastructure has kept sentiment swinging between enthusiasm and caution.

- On our framework, Bloom Energy scores a 2/6 valuation score, suggesting pockets of value in some areas but clear stretch in others. In this article, we will break down what different valuation approaches say about the stock, and then finish with a more holistic way to think about its true worth.

Bloom Energy scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Bloom Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it could generate in the future and discounting those cash flows back to today in dollar terms.

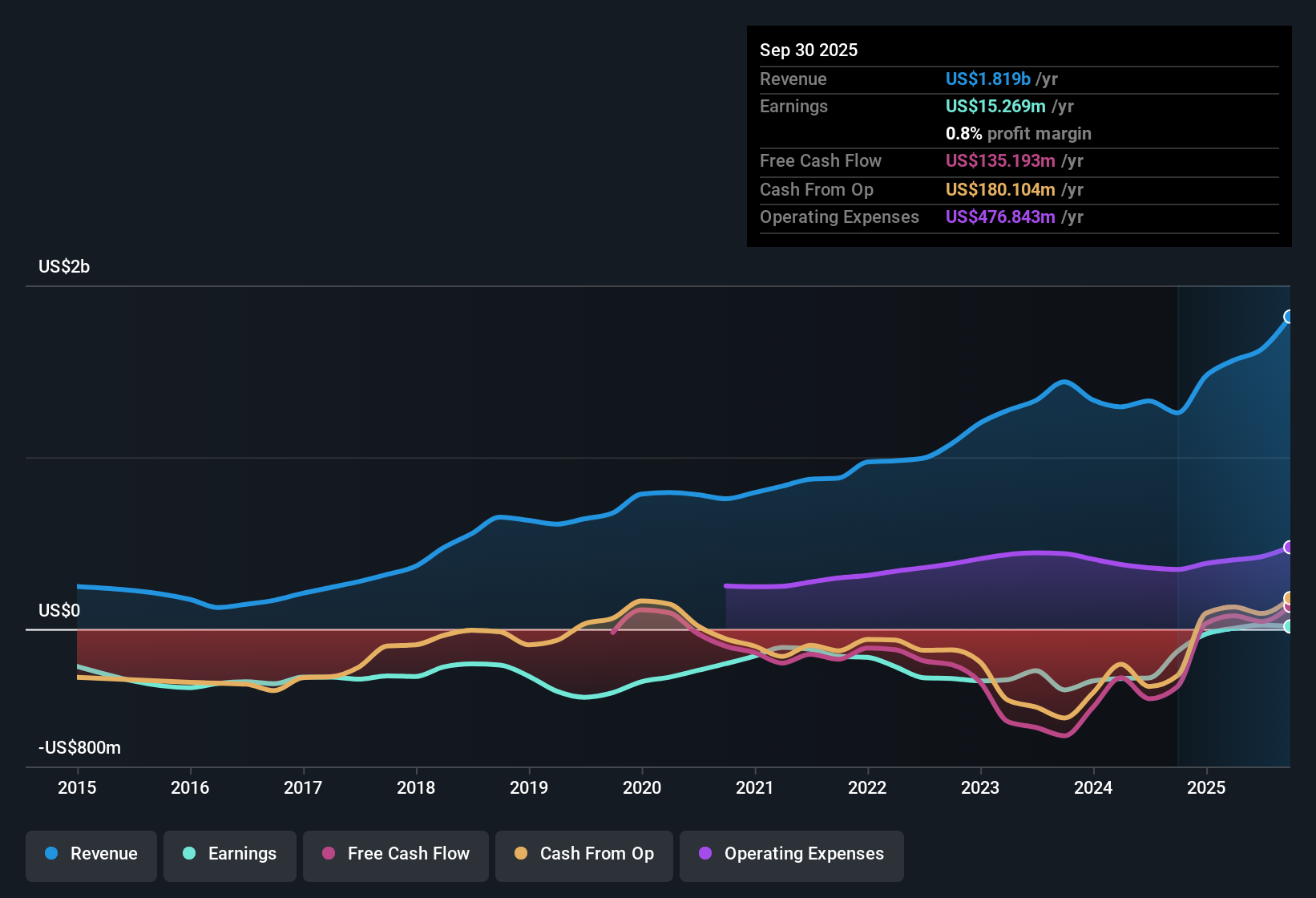

Bloom Energy currently produces around $94.6 million in free cash flow. Analysts expect this to increase as the business scales. Based on a two stage free cash flow to equity model, analyst forecasts and Simply Wall St extrapolations indicate free cash flow could reach roughly $1.5 billion by 2029, with further growth assumed into the early 2030s.

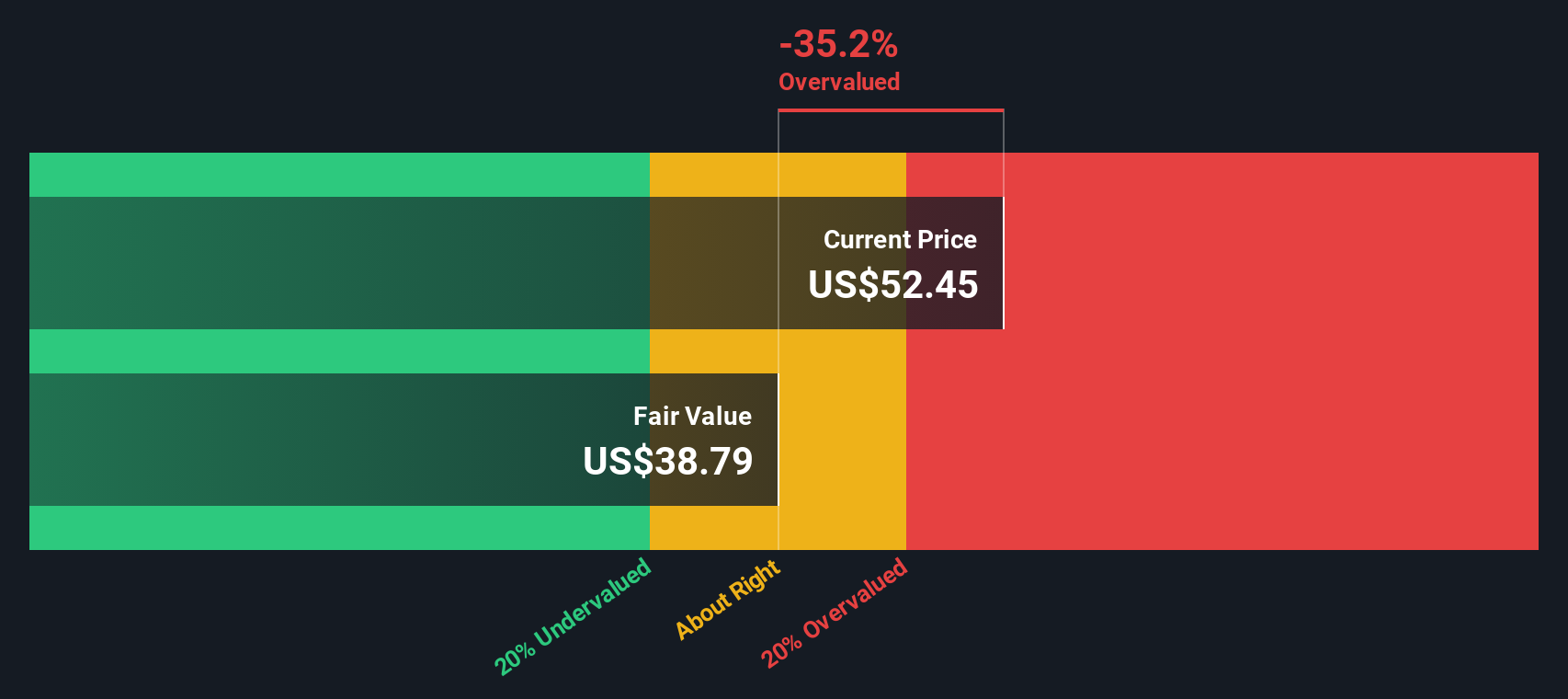

When these projected cash flows are discounted back to today, the model arrives at an intrinsic value of about $148 per share. Compared with the current share price, this implies the stock trades at roughly a 29.0% discount, indicating the market price may not fully reflect the assumed growth path in the model.

Result: UNDERVALUED (based on this DCF model)

Our Discounted Cash Flow (DCF) analysis suggests Bloom Energy is undervalued by 29.0%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: Bloom Energy Price vs Sales

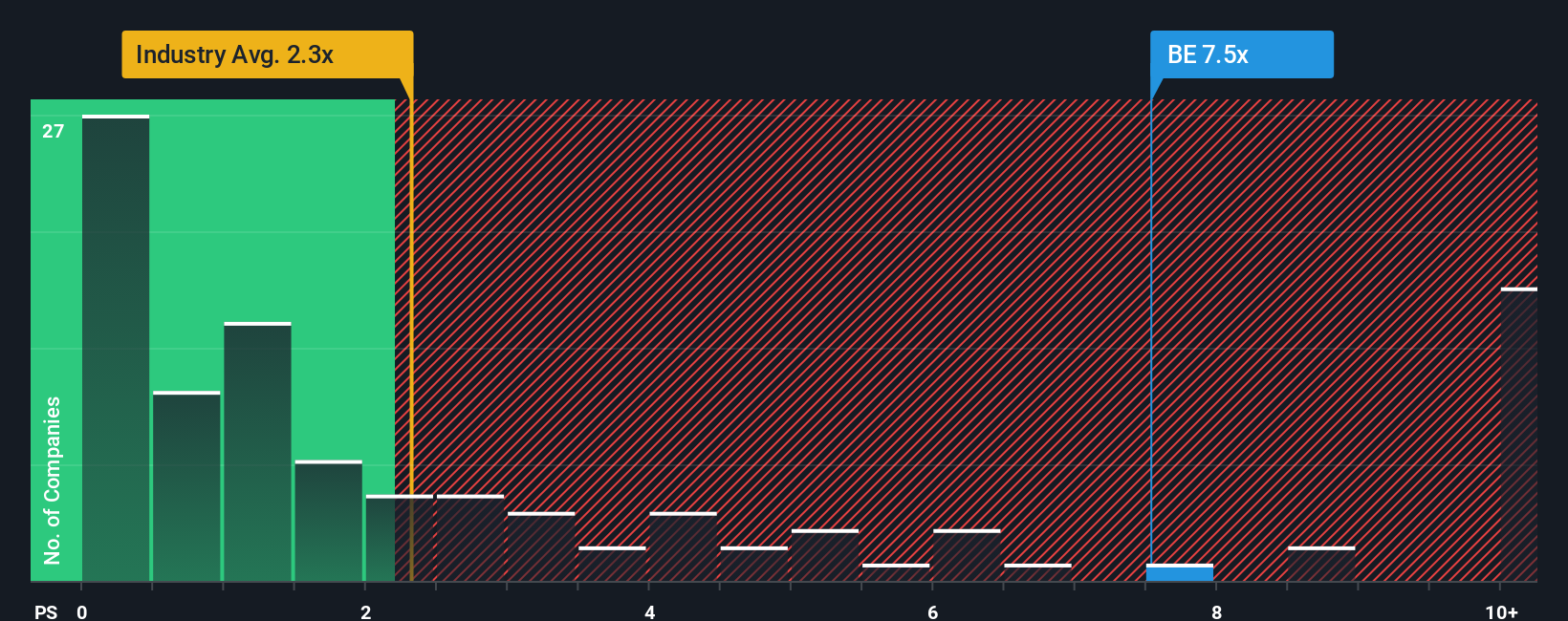

For companies like Bloom Energy that are still building toward consistent profitability, the price to sales (P/S) ratio is often a more practical yardstick than earnings based metrics. It focuses on how much investors are paying for each dollar of revenue, which is particularly useful when profits are volatile or still developing.

In general, higher growth expectations and lower perceived risk support a higher sales multiple, while slower growth or elevated risk usually mean a lower, more conservative ratio is appropriate. Bloom Energy currently trades on a P/S of about 13.65x, which is well above the Electrical industry average of roughly 2.09x and the peer group average of around 2.79x. This indicates that the market is already pricing in strong growth and a favorable outlook.

Simply Wall St’s proprietary Fair Ratio seeks to refine this comparison by estimating the P/S multiple a stock should command after accounting for its growth profile, profitability, industry, size, and risk factors. For Bloom Energy, this Fair Ratio is calculated at 8.48x, which is substantially below the current 13.65x. On this framework, the stock appears to be trading ahead of what its fundamentals would justify.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bloom Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simply your own story about Bloom Energy that connects what you believe about its products, competitive position, and industry tailwinds to specific forecasts for revenue, margins, and cash flows. You can then connect those forecasts to a Fair Value that you can compare with the current share price to help assess whether it looks attractive on Simply Wall St’s Community page, where millions of investors share these dynamic, auto updated views as new earnings or news arrives. One investor might build a bullish Bloom Energy Narrative around rapid AI driven power demand, strong policy support, and a Fair Value near the higher end of recent targets. Another investor could frame a far more cautious Narrative that focuses on natural gas reliance, execution risk, and competition, leading to a much lower Fair Value that helps them justify avoiding or trimming the stock at today’s price.

Do you think there's more to the story for Bloom Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bloom Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BE

Bloom Energy

Designs, manufactures, sells, and installs solid-oxide fuel cell systems for on-site power generation in the United States and internationally.

Exceptional growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

16 followersusers have followed this narrative

5 commentsusers have commented on this narrative

3 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative