Advertisement

- United States

- /

- Electrical

- /

- NYSE:BE

Bloom Energy (BE): Reassessing Valuation After a Volatile Year and Sharp Three-Month Rebound

Simply Wall St

Reviewed by Simply Wall St

Bloom Energy (BE) has quietly become a magnet for investors trying to make sense of volatile clean-energy names, especially after wild swings over the past month and a strong rebound in the past 3 months.

See our latest analysis for Bloom Energy.

Despite a choppy year that included a steep 30 day share price return of minus 28.0 percent, Bloom Energy has staged a powerful comeback, with a 90 day share price return of 86.7 percent and a 1 year total shareholder return of 290.0 percent suggesting that momentum and risk appetite are rebuilding.

If Bloom Energy’s surge has you rethinking where growth could come from next, it might be worth scanning high growth tech and AI stocks for other tech driven names with structural tailwinds.

With explosive returns, double digit revenue growth, and shares still trading below some valuation estimates, is Bloom Energy now a rare mispriced clean tech winner, or is the market already baking in years of future growth?

Most Popular Narrative Narrative: 8.9% Undervalued

With Bloom Energy last closing at $102.50 against a most popular narrative fair value of $112.50, the story hinges on aggressive growth and profitability assumptions.

Ongoing product cost reductions and digital twin enabled operational improvements, fueled by AI driven analytics from a large installed base, are lowering cost per watt and raising manufacturing efficiency, poised to drive continued operating margin and net margin expansion.

Curious how much faster revenues must grow, how far margins need to expand, and which future earnings multiple underpins that valuation? The answers might surprise you.

Result: Fair Value of $112.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rapid advances in zero emissions rivals and any stumble in Bloom’s manufacturing expansion could quickly undermine these upbeat growth and margin assumptions.

Find out about the key risks to this Bloom Energy narrative.

Another Lens on Value

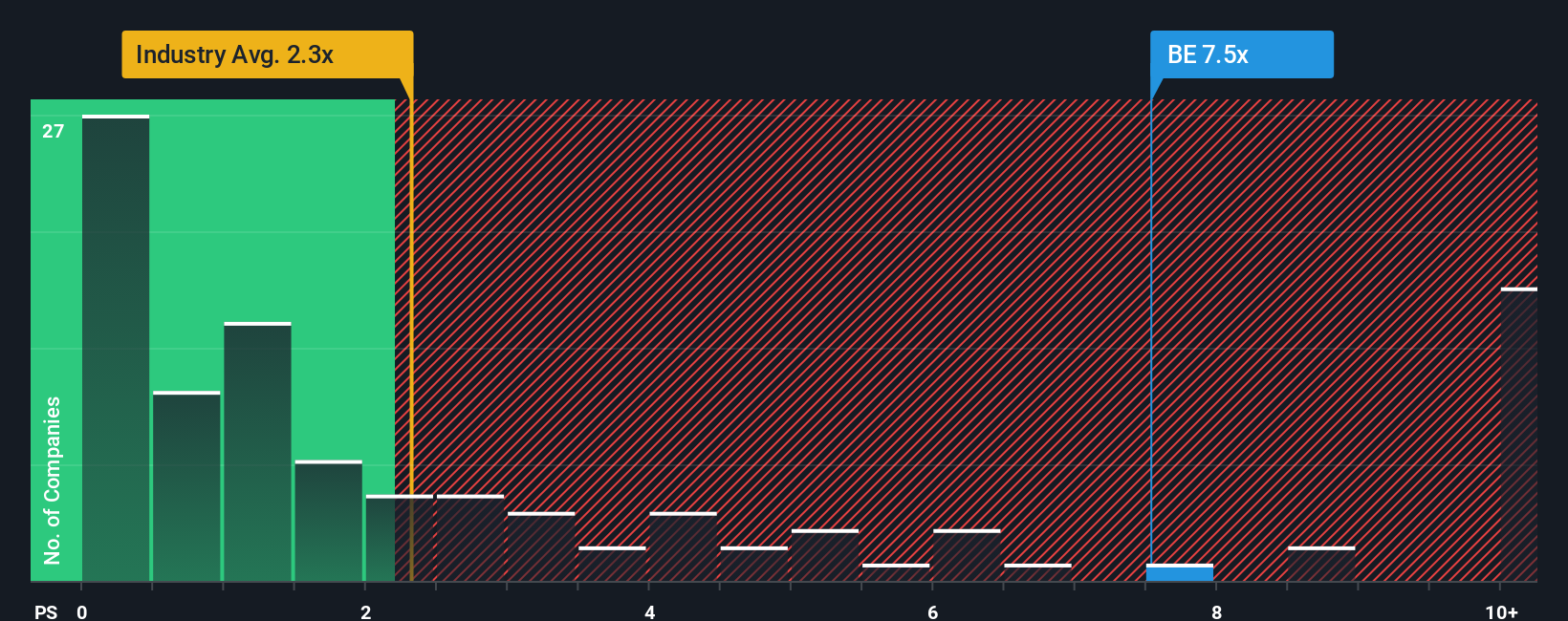

While the narrative and analyst targets suggest Bloom Energy is around 8.9 percent undervalued, the market is paying a steep 13.3 times sales, versus 2.8 times for peers and a fair ratio of 8.6 times. That gap signals real valuation risk if growth expectations slip, or upside if they are met.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bloom Energy Narrative

If you see the story differently, or want to stress test the assumptions yourself, you can build a personalized Bloom Energy narrative in minutes, Do it your way.

A great starting point for your Bloom Energy research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with Bloom Energy. Put Simply Wall Street’s powerful Screener to work now so you do not miss the next wave of standout opportunities.

- Capture potential mispricings by targeting quality businesses trading at attractive valuations with these 917 undervalued stocks based on cash flows tailored to long term, fundamentals focused investors.

- Ride cutting edge innovation by zeroing in on high potential names shaping the future of intelligent software and automation through these 25 AI penny stocks.

- Strengthen your income strategy by pinpointing reliable payers offering meaningful yields using these 14 dividend stocks with yields > 3% as your starting universe.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bloom Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BE

Bloom Energy

Designs, manufactures, sells, and installs solid-oxide fuel cell systems for on-site power generation in the United States and internationally.

Exceptional growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

40 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative