Advertisement

- United States

- /

- Machinery

- /

- NasdaqGM:EML

Most Shareholders Will Probably Find That The Compensation For The Eastern Company's (NASDAQ:EML) CEO Is Reasonable

The performance at The Eastern Company (NASDAQ:EML) has been rather lacklustre of late and shareholders may be wondering what CEO Gus Vlak is planning to do about this. At the next AGM coming up on 28 April 2021, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We think CEO compensation looks appropriate given the data we have put together.

Check out our latest analysis for Eastern

How Does Total Compensation For Gus Vlak Compare With Other Companies In The Industry?

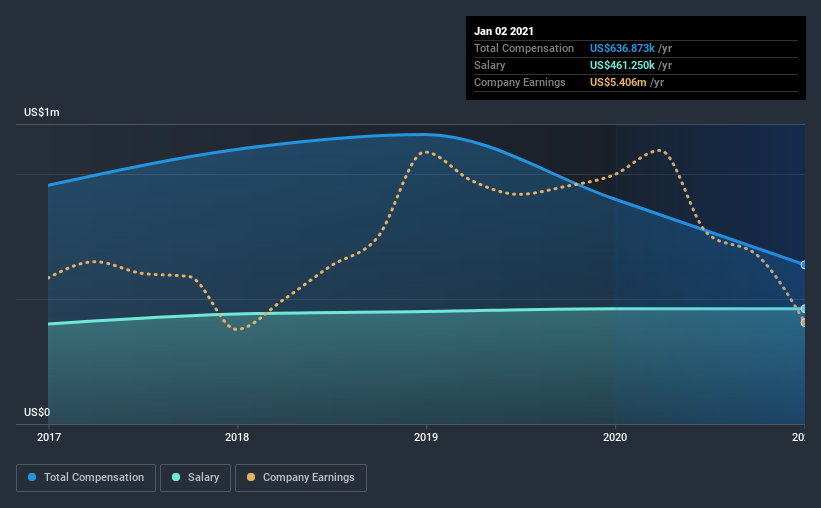

At the time of writing, our data shows that The Eastern Company has a market capitalization of US$158m, and reported total annual CEO compensation of US$637k for the year to January 2021. We note that's a decrease of 29% compared to last year. In particular, the salary of US$461.3k, makes up a huge portion of the total compensation being paid to the CEO.

On examining similar-sized companies in the industry with market capitalizations between US$100m and US$400m, we discovered that the median CEO total compensation of that group was US$950k. That is to say, Gus Vlak is paid under the industry median. What's more, Gus Vlak holds US$480k worth of shares in the company in their own name.

| Component | 2021 | 2019 | Proportion (2021) |

| Salary | US$461k | US$461k | 72% |

| Other | US$176k | US$441k | 28% |

| Total Compensation | US$637k | US$902k | 100% |

On an industry level, roughly 19% of total compensation represents salary and 81% is other remuneration. According to our research, Eastern has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

The Eastern Company's Growth

The Eastern Company's earnings per share (EPS) grew 2.4% per year over the last three years. In the last year, its revenue is down 4.6%.

We would prefer it if there was revenue growth, but the modest EPS growth gives us some relief. It's hard to reach a conclusion about business performance right now. This may be one to watch. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has The Eastern Company Been A Good Investment?

Since shareholders would have lost about 8.2% over three years, some The Eastern Company investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

The lack lustre share price performance may have something to do with the flat earnings growth. Shareholders will get the chance to question the board on key concerns and revisit their investment thesis with regards to the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 3 warning signs for Eastern that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading Eastern or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eastern might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:EML

Eastern

Designs, manufactures, and sells engineered solutions to industrial markets in the United States and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|50.2% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|3.4% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|1.4% undervalued

ZW

Community Contributor