Advertisement

- United States

- /

- Banks

- /

- NYSE:WBS

Should Webster Financial’s (WBS) Digital Strategy and Loan Growth Signal a Stronger Long-Term Investment Outlook?

Simply Wall St

Reviewed by Sasha Jovanovic

- Webster Financial Corporation reported strong third quarter 2025 results, with net interest income of US$631.67 million and net income of US$261.22 million, both up from the same period last year.

- An interesting insight is that the company’s investment in digital capabilities and new business lines, including the Marathon credit partnership, contributed to broad-based loan and deposit growth and ongoing asset quality improvements.

- We'll explore how this broad-based loan and deposit growth impacts Webster Financial's long-term investment outlook and business strategy.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Webster Financial Investment Narrative Recap

To be a shareholder in Webster Financial, you need to believe in the company’s ability to sustain loan and deposit growth, capitalize on digital investments, and manage credit risk, despite ongoing pressures such as margin compression and exposure to commercial real estate. The recent strong third-quarter results reinforce confidence in the main catalyst of broad-based loan and deposit growth, but do not materially change the biggest near-term risk of credit losses tied to potential commercial real estate market volatility.

Among recent company announcements, the update on share repurchases stands out: Webster bought back 2,200,000 shares for US$131.2 million in Q3, bringing total repurchases to over 14% of outstanding shares since 2017. While these buybacks may indicate board confidence in future earnings and can support per-share metrics, they do not buffer against risks from rising credit charges and ongoing deposit competition, both key factors that can influence short-term performance.

However, investors should not overlook the potential downside if commercial real estate credit quality deteriorates further, especially as ...

Read the full narrative on Webster Financial (it's free!)

Webster Financial's narrative projects $3.4 billion revenue and $1.2 billion earnings by 2028. This requires 10.8% yearly revenue growth and a $369 million earnings increase from $830.6 million today.

Uncover how Webster Financial's forecasts yield a $71.59 fair value, a 28% upside to its current price.

Exploring Other Perspectives

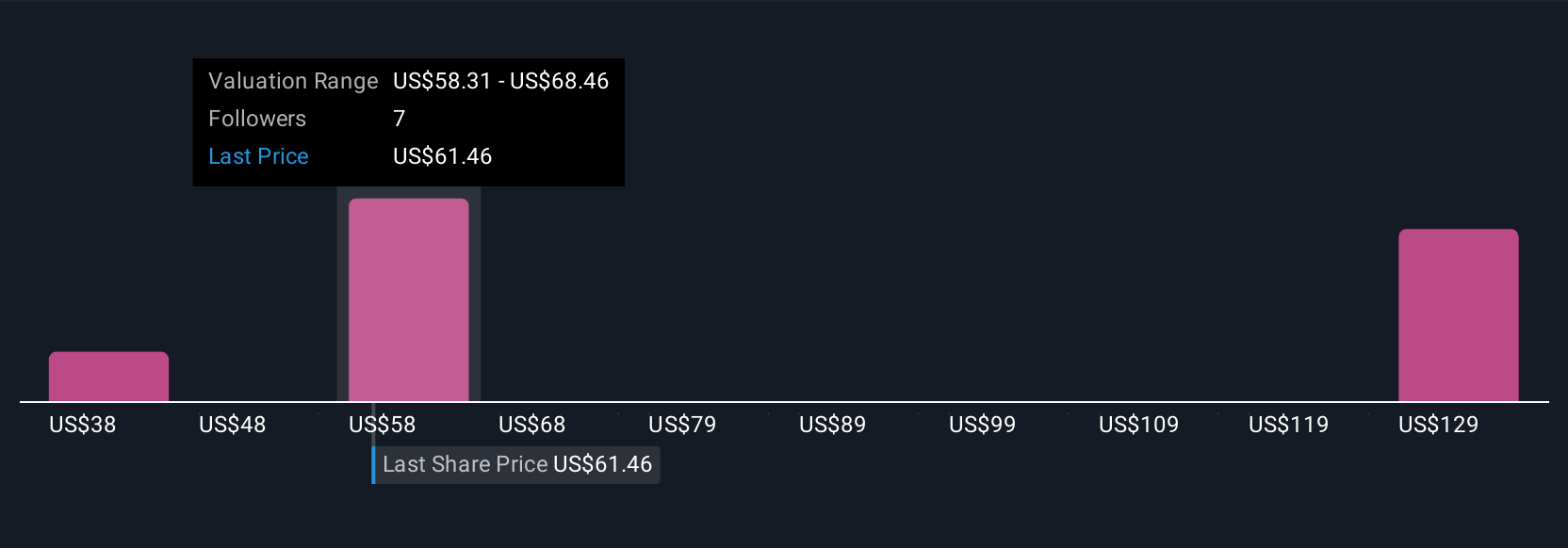

Three community estimates for Webster Financial’s fair value range from US$38 to over US$130 per share, reflecting highly varied expectations. While most analysts point to deposit and loan growth as key strengths, these numbers show that investors hold sharply different views about future performance, be sure to compare all sides before forming your opinion.

Explore 3 other fair value estimates on Webster Financial - why the stock might be worth 32% less than the current price!

Build Your Own Webster Financial Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Webster Financial research is our analysis highlighting 6 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Webster Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Webster Financial's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Webster Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WBS

Webster Financial

Operates as the bank holding company for Webster Bank, National Association that provides various financial products and services to businesses, individuals, and families in the United States.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor