Advertisement

- United States

- /

- Banks

- /

- NYSE:WAL

Western Alliance Bancorporation (WAL) Is Up 9.4% After Q3 Earnings Beat and Share Buyback—What's Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- Western Alliance Bancorporation recently reported third quarter earnings that exceeded analyst expectations, with strong deposit growth and solid net interest income, despite elevated net loan charge-offs of US$31.1 million compared to US$26.6 million a year earlier.

- An interesting aspect of the news is that the company simultaneously completed a buyback of 300,833 shares for US$25 million, even while managing litigation related to a credit facility fraud where proactive disclosure and legal action were emphasized.

- We’ll assess how the combination of resilient quarterly earnings and ongoing credit and legal challenges impacts Western Alliance’s investment narrative going forward.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Western Alliance Bancorporation Investment Narrative Recap

To be a shareholder in Western Alliance Bancorporation, you need to believe in the company's ability to drive consistent loan and deposit growth across its core Sun Belt markets, while carefully managing credit risk from its commercial real estate exposure. The recent uptick in net loan charge-offs is an important watch point, but does not appear to meaningfully weaken the short-term catalyst of robust deposit inflows following strong third-quarter results; however, ongoing legal and credit challenges remain a key risk to monitor.

The recently completed US$25 million buyback of 300,833 shares stands out, especially alongside the company's proactive disclosure regarding credit issues from a fraud event. While management’s focus on delivering shareholder value is clear, monitoring the interplay between capital actions and managing elevated credit costs will be important for assessing the sustainability of future growth.

By contrast, investors should stay informed about the potential impact of unresolved legal and credit matters on Western Alliance’s earnings profile...

Read the full narrative on Western Alliance Bancorporation (it's free!)

Western Alliance Bancorporation's outlook calls for $4.4 billion in revenue and $1.4 billion in earnings by 2028. This is based on an 11.9% annual revenue growth rate and a $566.6 million increase in earnings from the current $833.4 million.

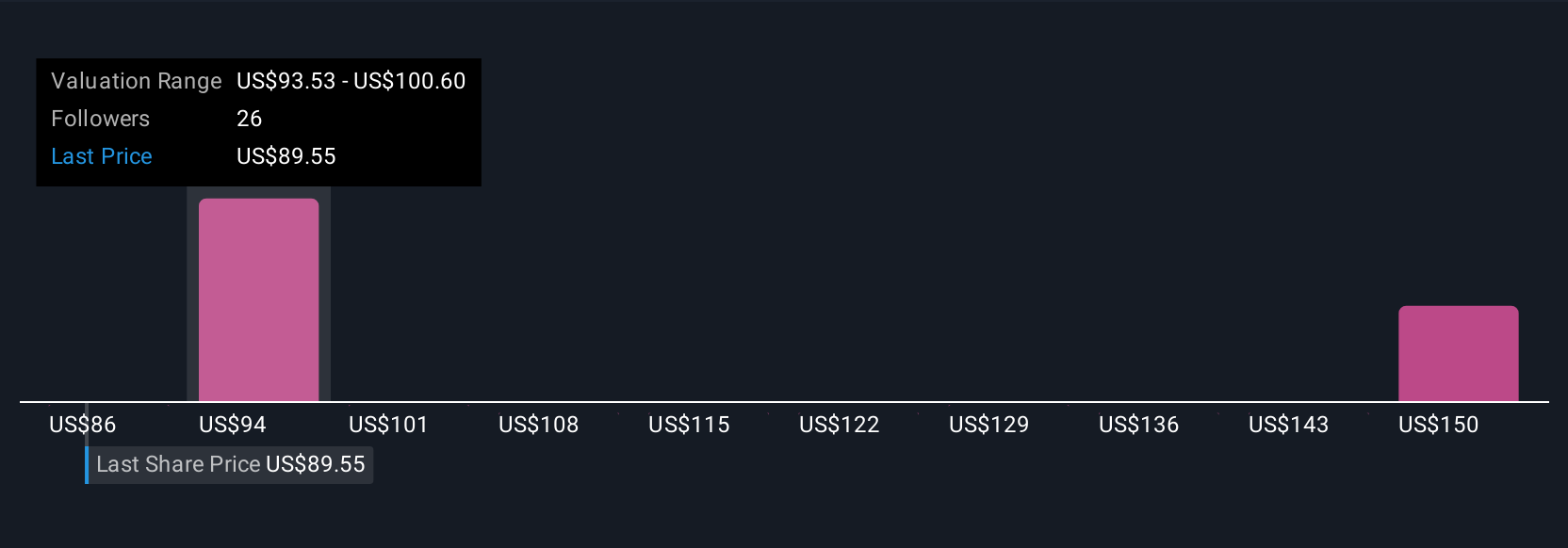

Uncover how Western Alliance Bancorporation's forecasts yield a $102.06 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community estimate Western Alliance Bancorporation’s fair value between US$96.06 and US$166.60 per share. While many are attracted by the current earnings momentum, the recent rise in charge-offs highlights the challenge of balancing growth with consistent credit quality.

Explore 6 other fair value estimates on Western Alliance Bancorporation - why the stock might be worth just $96.06!

Build Your Own Western Alliance Bancorporation Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Western Alliance Bancorporation research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Western Alliance Bancorporation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Western Alliance Bancorporation's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Alliance Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WAL

Western Alliance Bancorporation

Operates as the bank holding company for Western Alliance Bank that provides various banking products and related services primarily in Arizona, California, and Nevada.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor