Advertisement

- Sweden

- /

- Life Sciences

- /

- OM:ALIF B

Exploring Undervalued Small Caps With Insider Actions In July 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets show signs of recovery, with small-cap stocks like the Russell 2000 Index recently outperforming their larger counterparts, investors may find potential opportunities in undervalued small caps. In this context, understanding insider actions can provide valuable insights into promising stocks that might be overlooked by the broader market.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Semen Indonesia (Persero) | 13.2x | 0.7x | 20.85% | ★★★★★☆ |

| East West Banking | 3.4x | 0.7x | 49.83% | ★★★★★☆ |

| Healius | NA | 0.6x | 41.53% | ★★★★★☆ |

| Strike Energy | 301.9x | 73.9x | 48.54% | ★★★★☆☆ |

| China Leon Inspection Holding | 10.1x | 0.7x | 25.18% | ★★★★☆☆ |

| RAM Essential Services Property Fund | NA | 5.9x | 37.41% | ★★★★☆☆ |

| Dicker Data | 22.3x | 0.8x | -0.95% | ★★★☆☆☆ |

| Ever Sunshine Services Group | 6.1x | 0.4x | 14.60% | ★★★☆☆☆ |

| Tai Sin Electric | 15.4x | 0.5x | 3.32% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

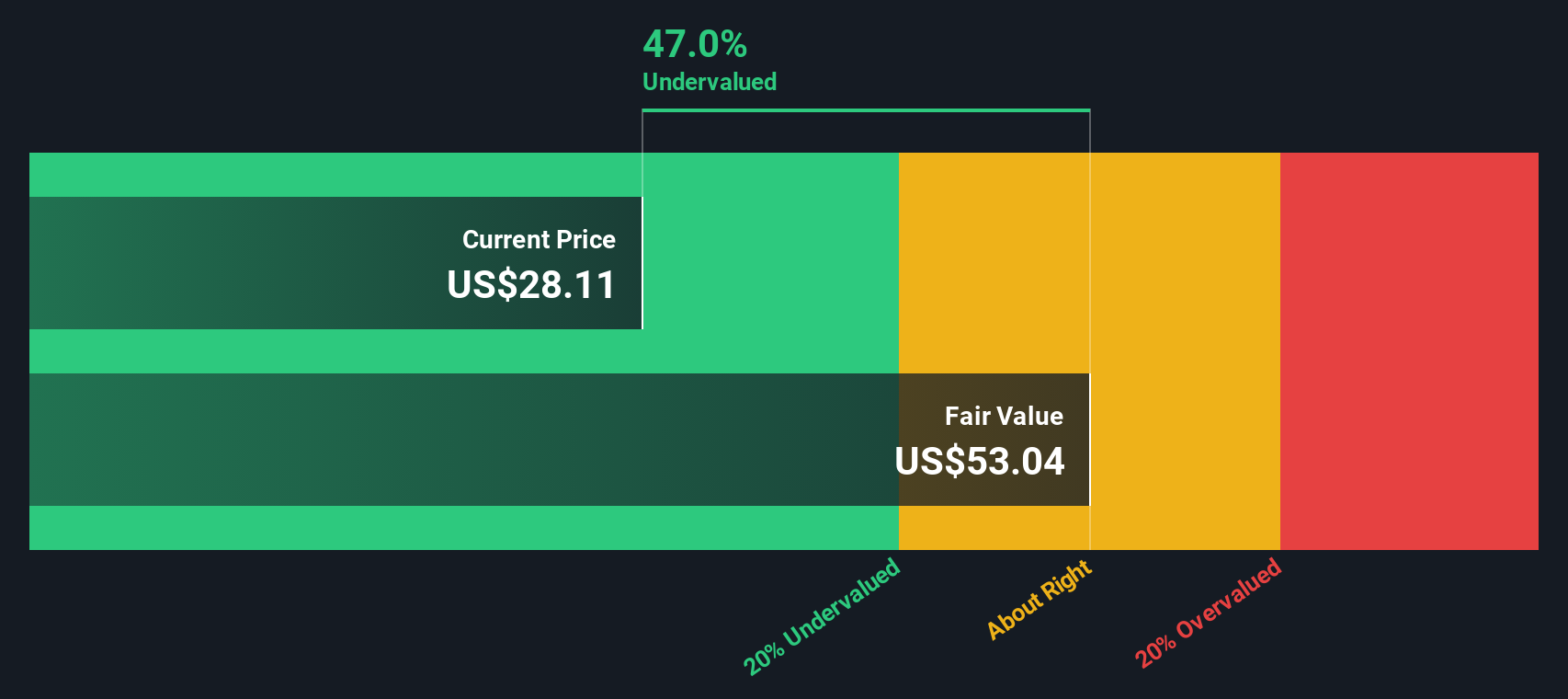

Byline Bancorp (NYSE:BY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Byline Bancorp is a bank holding company primarily engaged in offering banking products and services with a market capitalization of approximately $0.87 billion.

Operations: Banking operations have consistently reported a gross profit margin of 100%, with recent net income margins improving to approximately 0.31%. The business model demonstrates significant reliance on general and administrative expenses, which recently amounted to $184.24 million, alongside sales and marketing expenses of $3.80 million.

PE: 10.8x

Byline Bancorp recently showed robust financial performance, with a notable increase in net interest income to US$85.54 million and net income rising to US$30.44 million in the first quarter of 2024, compared to the previous year. This growth is underscored by insider confidence, as evidenced by recent share purchases. Additionally, Byline has secured an extended credit facility up to US$15 million until May 2025, enhancing its financial flexibility amid forecasts of a slight earnings decline over the next three years.

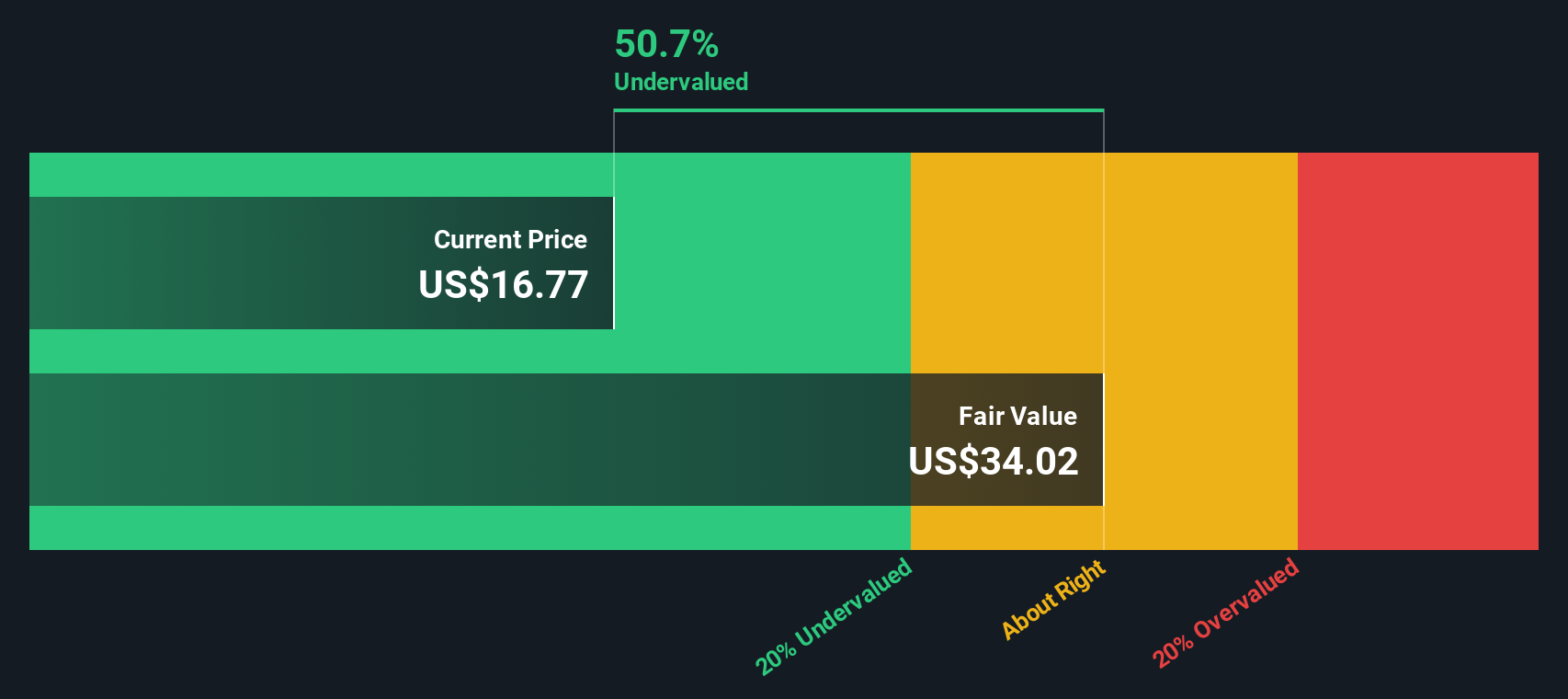

Provident Financial Services (NYSE:PFS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Provident Financial Services is a financial institution offering traditional banking and other financial services, with a market capitalization of approximately $1.07 billion.

Operations: This entity generates a consistent gross profit margin of 100%, with its latest reported quarterly revenue at $441.20 million. Its net income margin has seen fluctuations, most recently recorded at 27.19%.

PE: 11.1x

Provident Financial Services, recently bolstering its leadership and expanding board diversity, reflects strategic agility amid a dynamic market. With earnings poised to grow significantly at 54.74% annually, their recent $225 million fixed-income offering underscores a fortified financial posture. Insider confidence shone through as they recently purchased shares, signaling robust faith in the company's trajectory. This move, coupled with a substantial shelf registration of $40.78 million for employee stock ownership, suggests a commitment to long-term value creation and stability within this sector.

- Delve into the full analysis valuation report here for a deeper understanding of Provident Financial Services.

Gain insights into Provident Financial Services' past trends and performance with our Past report.

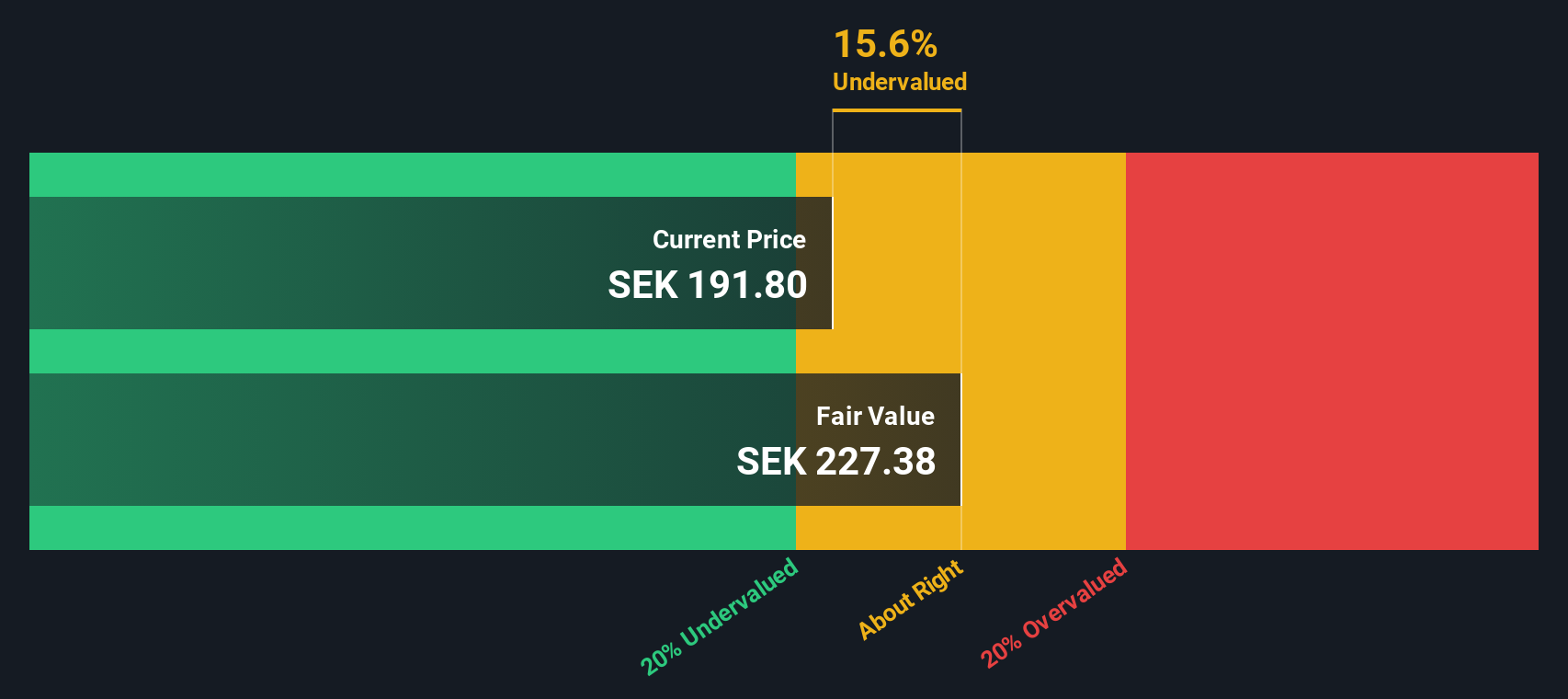

AddLife (OM:ALIF B)

Simply Wall St Value Rating: ★★★★★☆

Overview: AddLife is a company that operates in the life sciences sector, focusing on laboratory and medical technology products, with a market cap of approximately SEK 14.15 billion.

Operations: Labtech and Medtech are the primary revenue contributors, generating SEK 3.68 billion and SEK 6.32 billion respectively. The company's gross profit margin has shown a slight increase over recent periods, reaching approximately 37% by mid-2024, reflecting its ability to manage costs relative to sales effectively.

PE: 157.7x

Recently, AddLife demonstrated a notable financial performance with its second-quarter sales reaching SEK 2,554 million, up from SEK 2,365 million the previous year. This growth is mirrored in their net income for the same period which doubled to SEK 72 million. Despite these gains, the company's profit margins have dipped compared to last year and interest payments are straining earnings. However, insider confidence is evident as insiders have recently purchased shares, signaling belief in the company’s potential despite current financial pressures. This aligns with a forecasted earnings growth of over 53% per year, painting a promising picture for future value realization.

- Click here and access our complete valuation analysis report to understand the dynamics of AddLife.

Assess AddLife's past performance with our detailed historical performance reports.

Next Steps

- Navigate through the entire inventory of 226 Undervalued Small Caps With Insider Buying here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ALIF B

AddLife

Provides equipment, consumables, and reagents primarily to healthcare sector, research, colleges, and universities, as well as the food and pharmaceutical industries.

Reasonable growth potential with proven track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor