Advertisement

- United States

- /

- Banks

- /

- NYSE:MTB

Is There Now an Opportunity in M&T Bank Following Regulatory Risk Headlines?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if now is the right time to consider M&T Bank’s stock for your portfolio? Let’s dive into what is driving its value and whether it is truly a bargain right now.

- M&T Bank’s share price has seen a modest bump of 0.9% over the past week and is up 4.9% for the last 30 days. However, it is still down 11.1% from a year ago, showing both changing risk perceptions and room for future growth.

- Recently, headlines have focused on regulatory shifts impacting regional banks, with M&T Bank highlighting its robust risk management and capital position in response. This has helped reassure investors, even as broader market sentiment remains cautious for financials.

- On our scoring system, M&T Bank comes in with a strong 5 out of 6 valuation checks, suggesting it is undervalued on most major metrics. Yet, as we will explore later, there may be an even more insightful way to judge its real worth.

Find out why M&T Bank's -11.1% return over the last year is lagging behind its peers.

Approach 1: M&T Bank Excess Returns Analysis

The Excess Returns model is a valuation approach that examines how much profit a company can generate on its invested capital above the cost of capital. The higher the excess return, the more value is being created for shareholders. For M&T Bank, this means looking at how its return on equity compares to the cost of equity and what that difference means for potential investors.

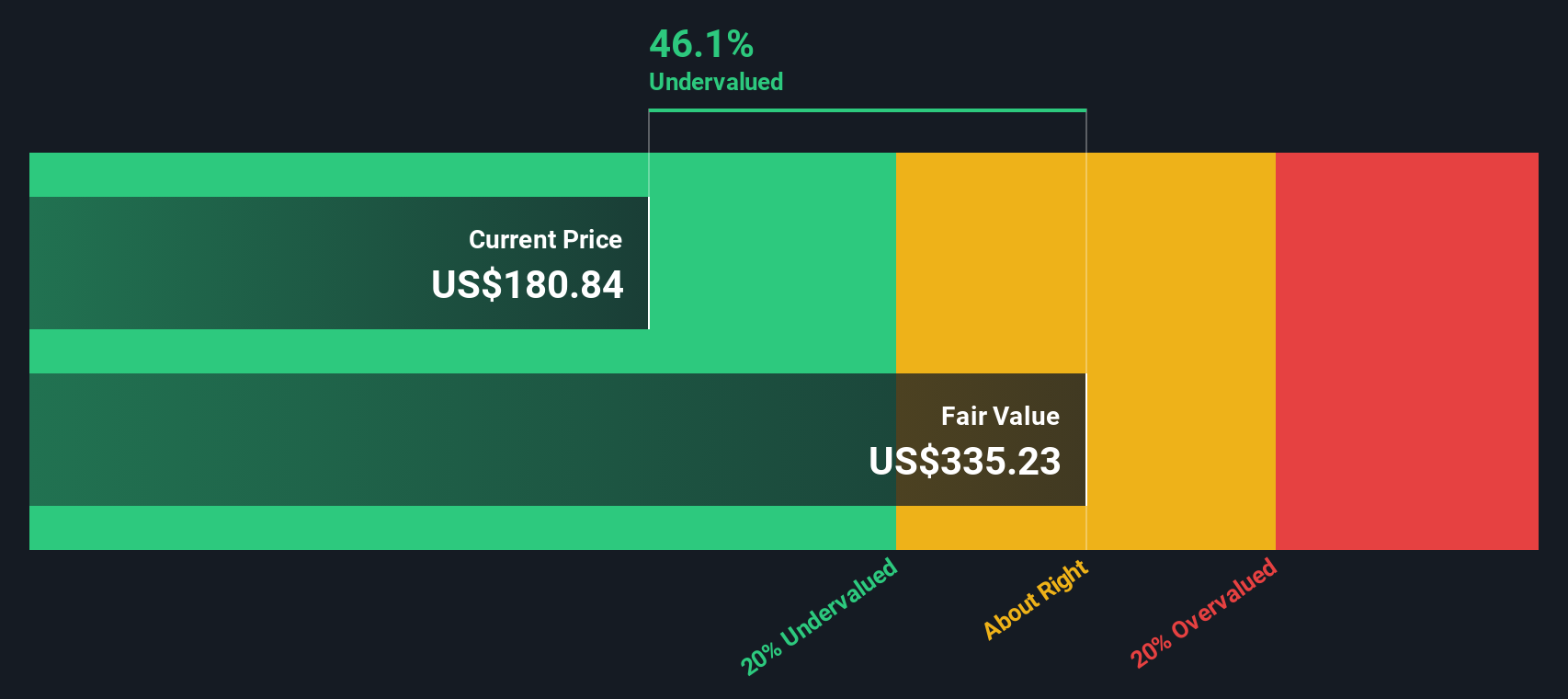

M&T Bank currently reports a Book Value of $170.44 per share and a Stable EPS of $19.12 per share. These figures are driven by weighted future analyst estimates of return on equity. The average Return on Equity stands at a solid 10.36%. The cost of equity, which is the return required by investors, is $13.12 per share. This puts M&T’s excess return, or the profit generated above this cost, at $6.00 per share. Over time, the stable Book Value is projected to grow to $184.51 per share, reflecting cautious but steady progress in building the company’s equity base.

Given these metrics, the Excess Returns model estimates that M&T Bank shares are trading at a substantial 44.1% discount to their intrinsic value. This margin signals a company that is not just generating returns but doing so at a price that may offer significant upside for investors willing to look past recent market volatility.

Result: UNDERVALUED

Our Excess Returns analysis suggests M&T Bank is undervalued by 44.1%. Track this in your watchlist or portfolio, or discover 933 more undervalued stocks based on cash flows.

Approach 2: M&T Bank Price vs Earnings

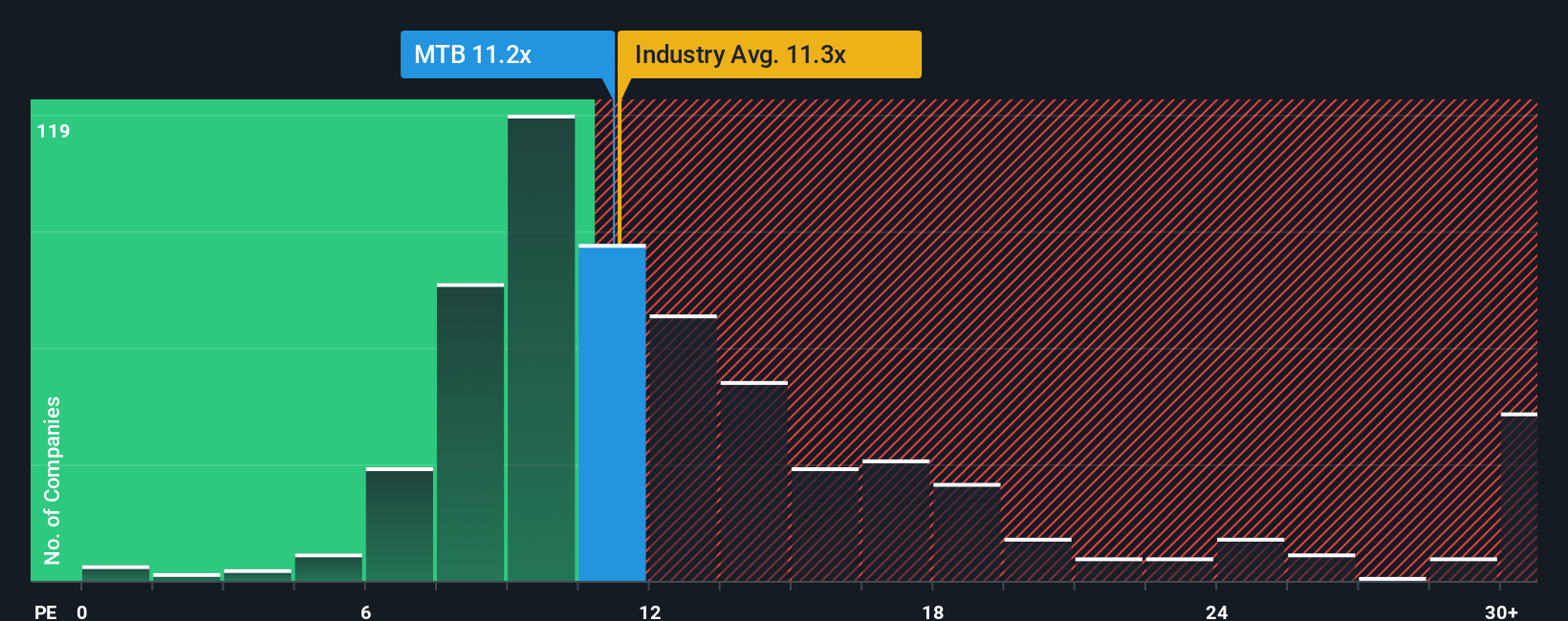

The Price-to-Earnings (PE) ratio is one of the most common ways to value profitable companies, because it directly relates a company's stock price to its per-share earnings. For established banks like M&T Bank, a lower PE ratio can point to undervaluation, while a higher PE ratio usually means investors expect above-average growth or reduced risk.

In practice, what counts as a “normal” PE ratio can shift depending on the company's growth prospects and perceived risk. Companies with faster earnings growth or lower risk often trade at higher multiples, since investors are willing to pay more for each dollar of consistent earnings.

M&T Bank’s current PE ratio is 11.1x. This compares slightly below both the listed industry average PE of 11.4x and the peer group average of 12.4x. While comparing a company’s valuation to its sector is a useful starting point, it does not consider each company’s unique strengths or weaknesses.

This is where Simply Wall St's Fair Ratio comes in. The Fair Ratio for M&T Bank is calculated by factoring in much more than just peer multiples or sector norms. It considers earnings growth, profit margin, risk levels, industry factors and the company's market cap. This makes it a more holistic benchmark for what the company’s multiple should be, given its specific fundamentals.

M&T Bank’s Fair Ratio stands at 11.8x, very close to its actual PE of 11.1x. The small gap between these two numbers suggests that shares are currently trading at about their fair value based on the company’s earning power and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your M&T Bank Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is simply your story or perspective on a company, tying together your expectations for its financial future (like revenue, earnings, and profit margins) with the fair value you believe is justified by your assumptions.

Instead of relying only on broad metrics or peer comparisons, Narratives let you connect M&T Bank’s business story to a specific financial forecast and instantly see how your outlook translates into a fair value. This approach helps you see whether to buy or sell by directly comparing your calculated Fair Value to today’s market price.

Narratives also update automatically when new information arrives, such as news, regulatory changes or earnings updates. This ensures your investment thesis stays current. Available to millions of users on the Simply Wall St platform’s Community page, Narratives are designed to be accessible for everyone, making it easy to build and compare different viewpoints.

For example, with M&T Bank, one investor’s Narrative may be optimistic, expecting a price target of $240 based on strong loan growth and capital returns. Another might be more cautious, valuing shares at just $175 due to concerns about deposit declines and expense pressures. Narratives empower you to see the full range of opinions and take action with greater confidence.

Do you think there's more to the story for M&T Bank? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MTB

M&T Bank

Operates as a bank holding company for Manufacturers and Traders Trust Company and Wilmington Trust, National Association that provides retail and commercial banking products and services in the United States.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative