- United States

- /

- Banks

- /

- NYSE:BAC

Bank of America (NYSE:BAC) Reports Higher Q1 Earnings and Net Interest Income

Reviewed by Simply Wall St

Bank of America (NYSE:BAC) recently reported impressive first-quarter earnings, with net income rising to $7.4 billion and EPS increasing to $0.90. This robust financial performance likely played a role in the company's 3% price increase last week, aligning with strong market trends that saw bank stocks lift the indexes. Despite ongoing trade tensions with China affecting some sectors, the financial sector showed resilience, with banks like Citigroup also reporting positive results. The broader market gained momentum, led by tech and bank stocks, possibly reinforcing confidence in BAC's positive earnings surprise and enhancing its share value.

The recent robust earnings report from Bank of America, with net income reaching US$7.4 billion and EPS at US$0.90, not only contributed to a 3% rise in the share price last week but also aligns with the company's narrative surrounding organic loan and deposit growth, as well as digital strategy advancements. Over the past five years, shareholders have experienced a total return of 84.54%, reflecting a significant performance considering the broader market conditions. However, over the past year, Bank of America has lagged behind the US Banks industry, which experienced a return of 11.7%, indicating recent challenges despite long-term gains.

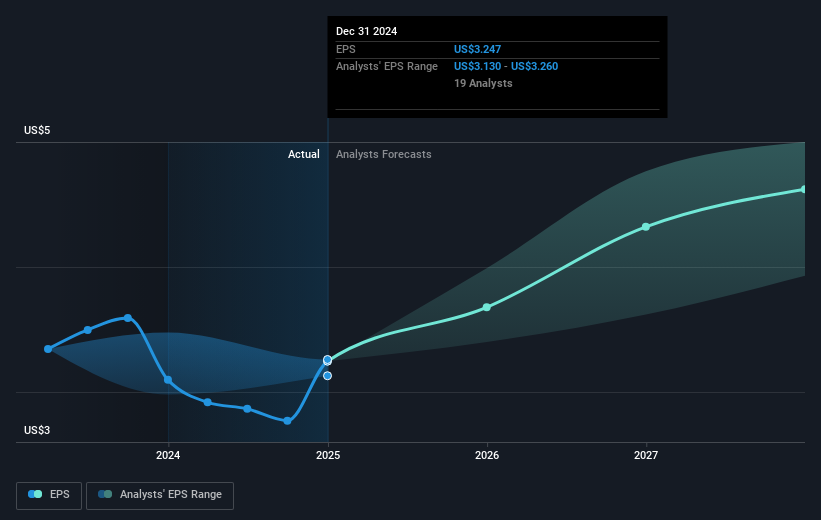

The positive earnings announcement is anticipated to impact future revenue and earnings forecasts favorably, reinforcing expectations for record net interest income and revenue growth as previously stated. With earnings expected to grow to US$31.7 billion by 2028, analysts have set a consensus price target of US$50.02, suggesting approximately 30% upside from the current share price of US$35.03. Despite the current price trailing behind the target, the emphasis on digital capabilities and client solutions, alongside measured strategies in wealth management and investment banking, fortifies the analysts' positive outlook, providing context for future growth potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of America might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BAC

Bank of America

Through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives