Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:UBSI

United Bankshares' (NASDAQ:UBSI) Upcoming Dividend Will Be Larger Than Last Year's

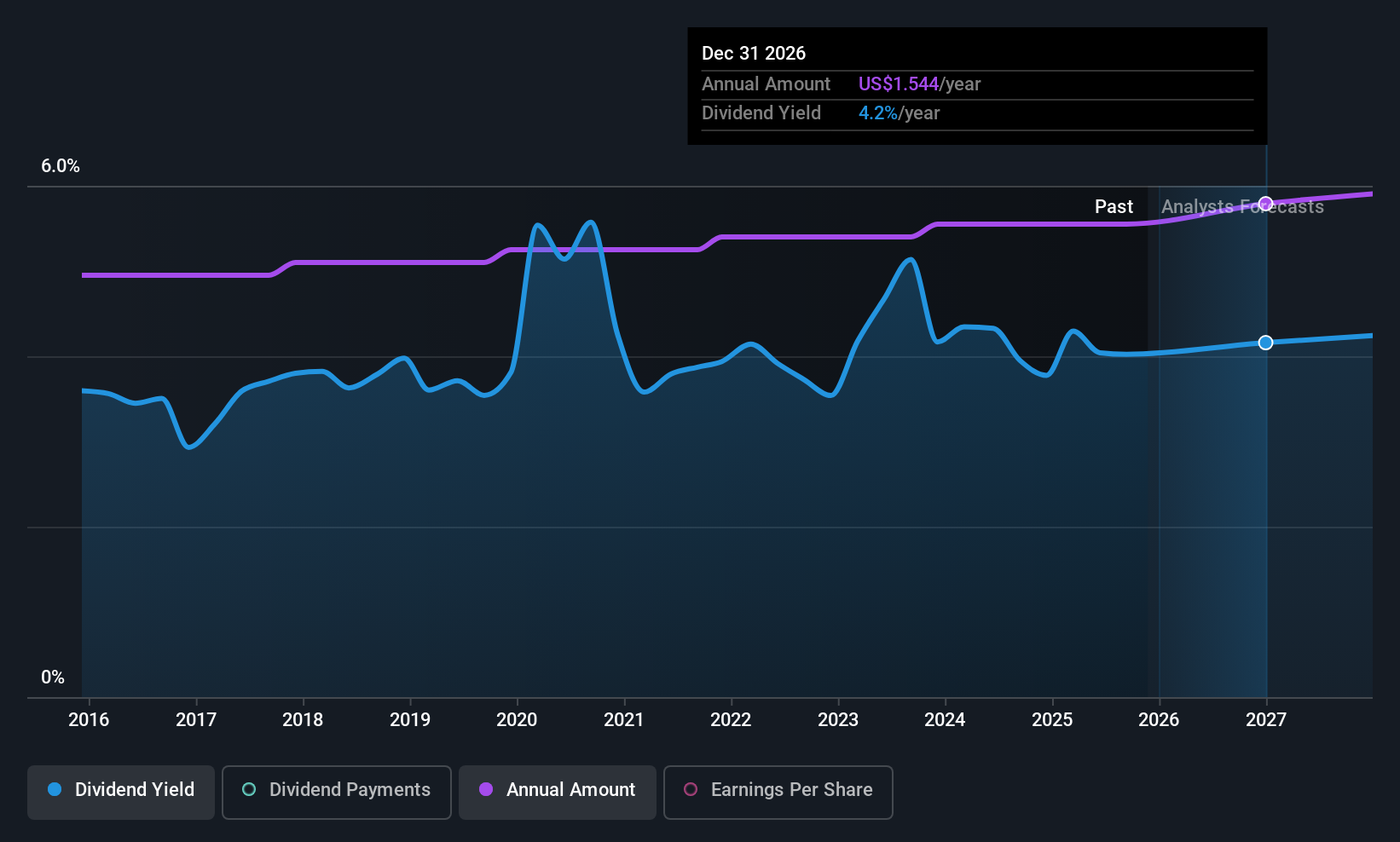

United Bankshares, Inc. (NASDAQ:UBSI) will increase its dividend on the 2nd of January to $0.38, which is 2.7% higher than last year's payment from the same period of $0.37. This will take the dividend yield to an attractive 4.0%, providing a nice boost to shareholder returns.

United Bankshares' Earnings Will Easily Cover The Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable.

United Bankshares has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Based on United Bankshares' last earnings report, the payout ratio is at a decent 48%, meaning that the company is able to pay out its dividend with a bit of room to spare.

The next 3 years are set to see EPS grow by 22.0%. Analysts estimate the future payout ratio will be 44% over the same time period, which is in the range that makes us comfortable with the sustainability of the dividend.

Check out our latest analysis for United Bankshares

United Bankshares Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the annual payment back then was $1.28, compared to the most recent full-year payment of $1.48. This implies that the company grew its distributions at a yearly rate of about 1.5% over that duration. Although we can't deny that the dividend has been remarkably stable in the past, the growth has been pretty muted.

United Bankshares Could Grow Its Dividend

Investors could be attracted to the stock based on the quality of its payment history. United Bankshares has seen EPS rising for the last five years, at 5.9% per annum. Earnings are on the uptrend, and it is only paying a small portion of those earnings to shareholders.

United Bankshares Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All of these factors considered, we think this has solid potential as a dividend stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 5 United Bankshares analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is United Bankshares not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:UBSI

United Bankshares

Through its subsidiaries, provides commercial and retail banking products and services in the United States.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

135 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

86 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

923 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative