Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:TRMK

A Fresh Look at Trustmark (TRMK) Valuation After Solid Loan Growth and Revenue Beat

Simply Wall St

Reviewed by Kshitija Bhandaru

Trustmark (TRMK) delivered a quarterly update that checked important boxes for investors, with revenues meeting expectations and net interest income coming in ahead. The company’s management emphasized broad-based loan growth and strong credit quality as key drivers.

See our latest analysis for Trustmark.

Trustmark’s strong operational performance this quarter helped fuel renewed optimism among investors, with its share price up 15% year-to-date and the one-year total shareholder return sitting at an impressive 28.4%. Sustained momentum over both the three and five year periods highlights steady long-term value creation, suggesting that market sentiment is gradually warming as fundamentals strengthen.

If these moves have you curious about what else could be gaining traction, now’s the perfect time to discover fast growing stocks with high insider ownership

With shares already climbing and the company trading about 10% below analyst price targets, investors may wonder if there is an undervalued opportunity here or if Trustmark’s future growth has already been factored in.

Most Popular Narrative: 8.7% Undervalued

With Trustmark’s current share price still below what the most-followed narrative considers fair value, the numbers suggest room for further gains compared to the present market mood.

The ongoing generational wealth transfer and increasing affluence among younger cohorts is opening up opportunities for fee-based wealth management and financial planning services, likely driving increases in noninterest income and diversified earnings streams. Accelerated investments in digital banking and technology infrastructure are expected to enhance operational efficiency, reduce overhead, and expand customer reach. This supports better net margins and improved scalability over the long term.

Curious what’s fueling this confidence? The market is betting on a rare mix of expansion into top-growth regions and a bold digital transformation plan. There’s also a surprising twist in expected profitability. Uncover exactly how these shifting dynamics could reshape the company’s future numbers.

Result: Fair Value of $43.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, unexpected regional economic downturns or delays in digital innovation could challenge Trustmark’s growth and put pressure on future earnings potential.

Find out about the key risks to this Trustmark narrative.

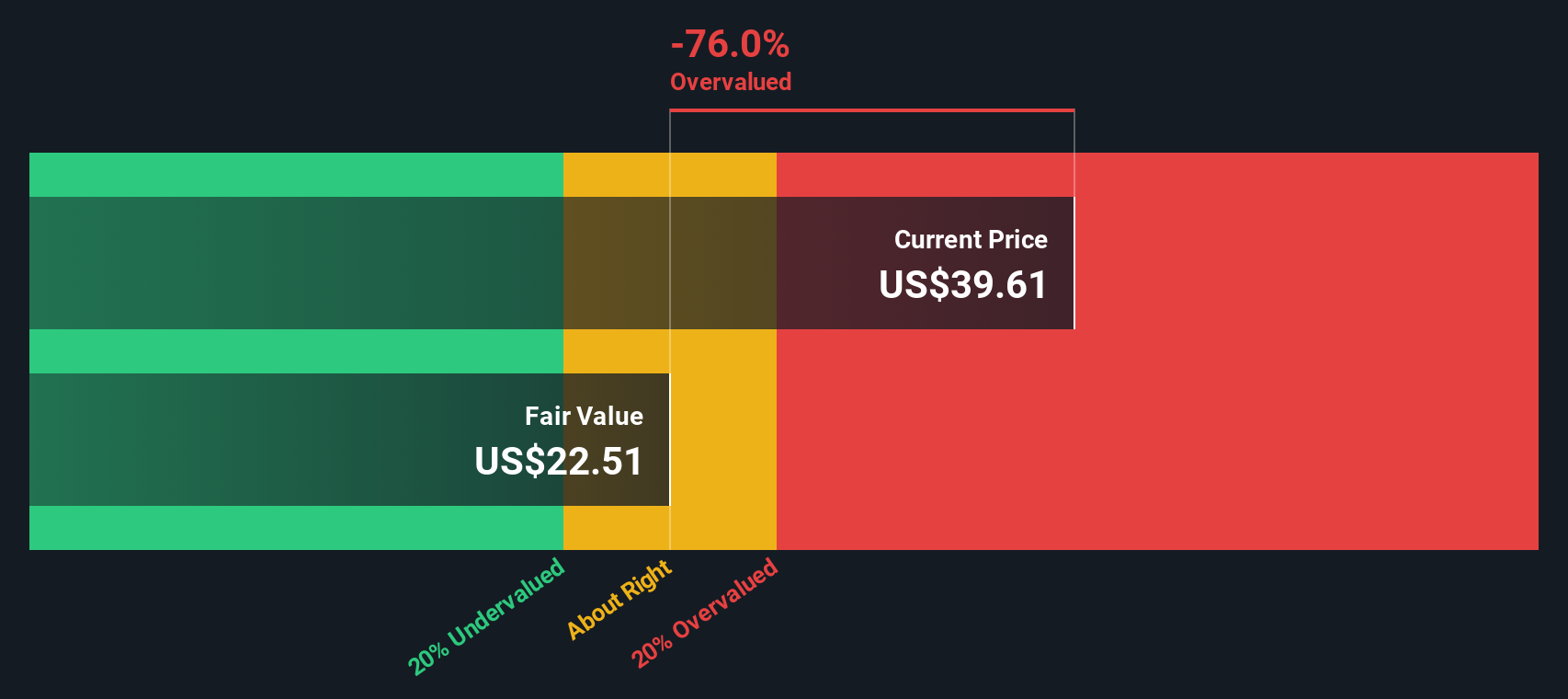

Another View: Numbers Show a Different Story

While analysts see Trustmark as slightly undervalued based on future earnings estimates, our SWS DCF model tells a very different story. When we run the numbers, the shares appear to be trading above what the underlying cash flows suggest is fair value. Which perspective should matter more for investors?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Trustmark for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Trustmark Narrative

If you see the numbers from a different angle or want to dig deeper into the data, you can quickly shape your own view in just minutes. Do it your way

A great starting point for your Trustmark research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Staying ahead in the market means knowing where to look next. Equip yourself with an edge by acting now, not later, and uncover smart stocks other investors are missing.

- Unlock growth stories by exploring potential in high-innovation sectors through these 25 AI penny stocks.

- Build up your income stream with opportunities in these 19 dividend stocks with yields > 3%, where solid yields meet sustainability.

- Position yourself early by staying ahead of the curve with these 78 cryptocurrency and blockchain stocks, tapping into the latest trends in digital assets and blockchain.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trustmark might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TRMK

Trustmark

Operates as the bank holding company for Trustmark National Bank that provides banking and other financial solutions to individuals and corporate institutions in the United States.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor