Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:ONB

A Look at Old National Bancorp’s (ONB) Valuation Following Sector Credit Quality Concerns

Simply Wall St

Reviewed by Kshitija Bhandaru

Regional bank stocks are feeling the heat after two lenders reported substantial loan losses and collateral issues, which has raised fresh questions about industrywide credit quality. Old National Bancorp (ONB) is among the banks seeing shares pressured by these developments.

See our latest analysis for Old National Bancorp.

Old National Bancorp’s share price came under pressure alongside other regional banks after several industry peers reported loan charge-offs and collateral issues, reviving credit quality concerns. Despite this renewed caution and a 6.69% drop in share price over the past month, Old National’s one-year total shareholder return stands at an impressive 12.2%. Its five-year figure exceeds 67%, reflecting solid long-term momentum even in a choppy market.

If you’re keeping an eye on sector shifts, now’s a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading nearly 28% below analyst targets and robust recent growth, the key question is whether Old National is an undervalued opportunity or if the market has already taken the company’s future potential into account.

Most Popular Narrative: 21.9% Undervalued

Compared to Old National Bancorp’s last close of $20.65, the most followed narrative sees fair value much higher, suggesting big upside potential. With a significant gap between current price and narrative target, the focus is firmly on what could drive future gains.

Strategic investment in digital banking infrastructure, highlighted by recent technology hires and ongoing upgrades, is enabling ONB to scale services efficiently, enhance client experience, and capitalize on the sector-wide shift toward digital and data-driven banking. This should drive greater noninterest income, improve net margins, and increase client retention over time.

Want to know what underpins this outsized valuation? The narrative’s secret sauce hints at unusually high earnings growth and margin expansion that rivals the sector’s standouts. Curious about the bold assumptions and the financial leap analysts project for ONB? Uncover the full story and see which numbers power this bullish case.

Result: Fair Value of $26.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising commercial real estate exposure and limited geographic reach could challenge Old National’s growth trajectory if market conditions shift unexpectedly.

Find out about the key risks to this Old National Bancorp narrative.

Another View: Market Ratios Tell a Different Story

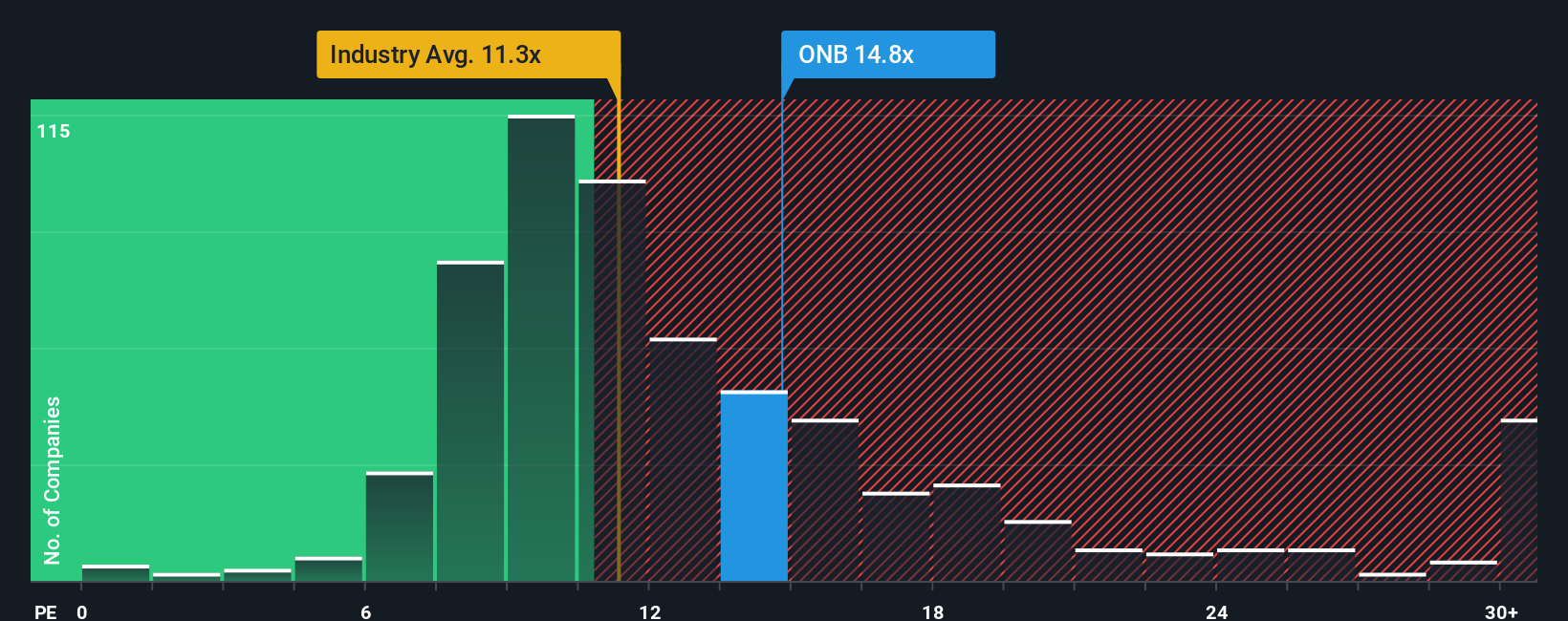

While the narrative-driven valuation points to Old National Bancorp being undervalued, market price-to-earnings ratios suggest caution. ONB trades at 14.7x earnings, higher than both the US Banks industry average of 11.2x and the peer average of 12.9x, but still below its fair ratio of 18.4x. This premium could signal that much optimism is already priced in, raising the risk if future growth falls short. Is the market too optimistic, or is there further room for re-rating?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Old National Bancorp Narrative

If you see a different story in the numbers or want to dive deeper, you can build your own narrative from scratch in just a few minutes. Do it your way

A great starting point for your Old National Bancorp research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Scores of high-potential stocks are waiting for you, but you could easily miss out unless you check out the latest opportunities with the Simply Wall Street Screener today.

- Boost your search for strong, consistent income by checking out these 17 dividend stocks with yields > 3%, which offers yields above 3% and has a proven payout history.

- Spot companies at the forefront of medical innovation with these 33 healthcare AI stocks, where advanced technology meets healthcare breakthroughs for tomorrow’s leaders.

- Get your chance to find undervalued stocks positioned for future growth by exploring these 873 undervalued stocks based on cash flows, which uses rigorous cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ONB

Old National Bancorp

Operates as the bank holding company for Old National Bank that provides consumer and commercial banking services in the United States.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|10.4% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|12.4% undervalued

AN

Based on Analyst Price Targets