Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:INDB

Will Rising Revenue and Enterprise Acquisition Boost Independent Bank's (INDB) Growth Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

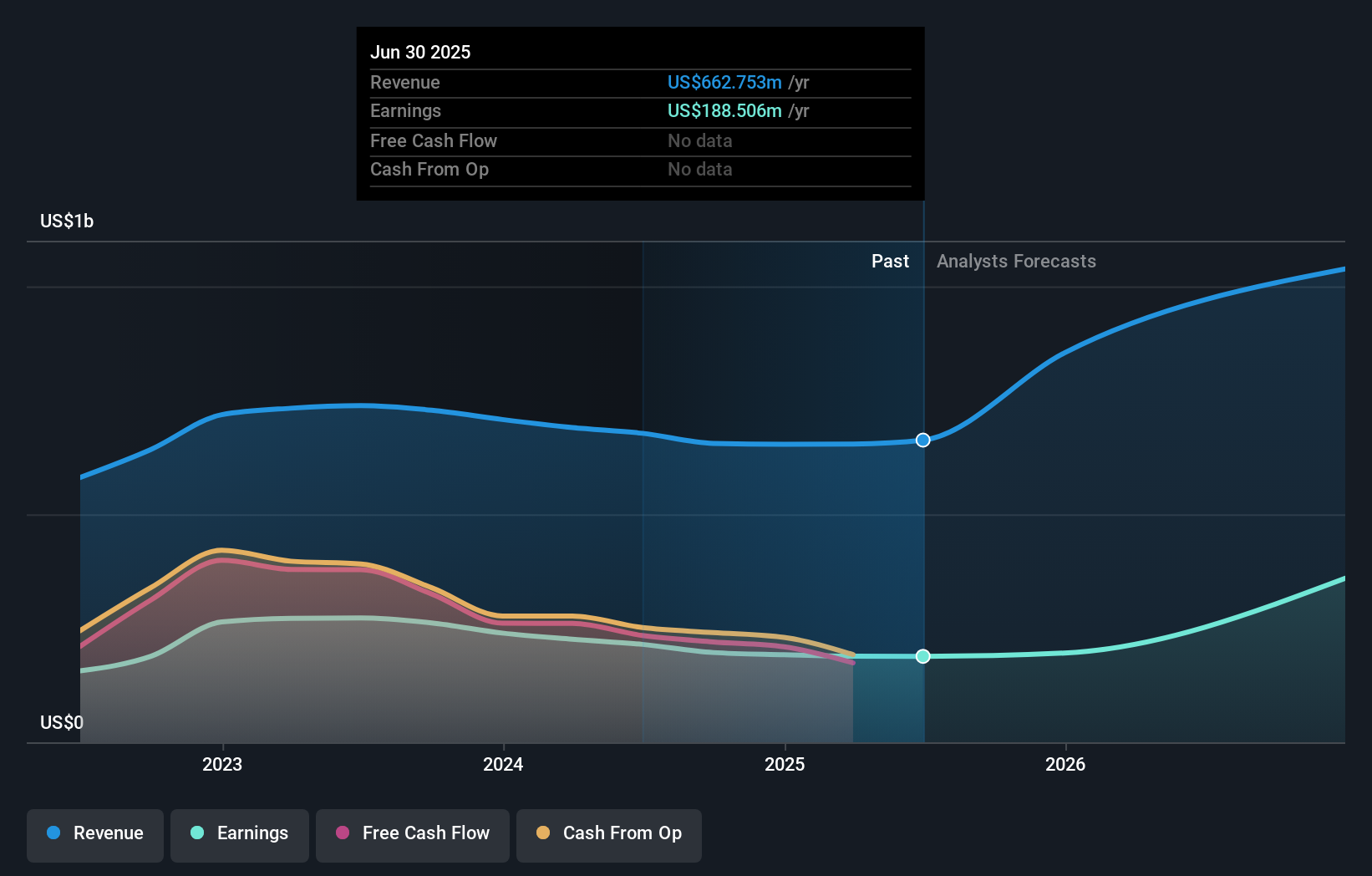

- Independent Bank Corp. recently reported its third-quarter 2025 results, highlighting a rise in net interest income to US$203.34 million while net income decreased to US$34.26 million compared to the year-ago period, and also completed a US$23.4 million share buyback.

- An interesting takeaway is that the strong quarterly revenue growth was largely attributed to successful integration of the Enterprise acquisition, improved net interest margins, and management’s positive outlook on scalable growth and cost savings.

- We’ll explore how the bank’s strong revenue growth and Enterprise acquisition integration update could reshape its investment narrative going forward.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Independent Bank Investment Narrative Recap

To be a shareholder in Independent Bank today, you need confidence in management's ability to deliver scalable growth and cost efficiencies by successfully integrating the Enterprise acquisition, while addressing credit quality concerns and exposure to commercial real estate loans. The recent Q3 2025 results affirm that revenue and net interest income are trending positively, but with net income down, the immediate catalyst remains progress on integration synergies; the main risk is ongoing credit costs tied to commercial real estate, which this quarter's updates do not materially reduce.

The recently completed US$23.4 million share buyback is especially relevant, signaling the company's ongoing commitment to shareholder returns amid operational challenges. This aligns with management’s focus on unlocking value as integration efforts continue to play out over the coming quarters, especially as credit risk remains a key variable for near-term performance.

By contrast, investors should be aware that integration risk, especially as the Enterprise combination temporarily increases exposure to commercial real estate lending, remains a key consideration for...

Read the full narrative on Independent Bank (it's free!)

Independent Bank's projections indicate revenues of $1.6 billion and earnings of $604.7 million by 2028. This outlook is based on a 32.9% annual revenue growth rate and represents an increase in earnings of $416.2 million from the current $188.5 million level.

Uncover how Independent Bank's forecasts yield a $82.75 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Independent Bank range from US$82.75 to US$90.15, based on 2 individual analyses. While these perspectives highlight possible upside, credit quality concerns linked to rising commercial real estate exposure could impact earnings, so you are encouraged to consider several viewpoints before acting.

Explore 2 other fair value estimates on Independent Bank - why the stock might be worth just $82.75!

Build Your Own Independent Bank Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Independent Bank research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Independent Bank research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Independent Bank's overall financial health at a glance.

No Opportunity In Independent Bank?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INDB

Independent Bank

Operates as the bank holding company for Rockland Trust Company that provides commercial banking products and services to individuals and small-to-medium sized businesses in the United States.

Flawless balance sheet with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor